We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Australian GDP, Lowe speaks as does Fed’s Brainard. ADP and Bank of Canada tonight.

Even though the US dollar and equities slid today, there’s optimism that President Trump will see sense and reverse his plans to kick start a trade war, or at least be more specific about which countries he targets. Phil Dobbie discusses the shifting scene with NAB’s Gavin Friend in London.

https://soundcloud.com/user-291029717/two-wars-could-be-off-the-agenda

Having been holding back for US President Trump’s net market moving tweet to make titular use of the Smith’s 1986 hit single it is another president, Kim Jon-un, who has instead gifted the opportunity after South Korea said North Korea is willing to talk about getting rid of its nuclear weapons but only if its own safety can be guaranteed.

The leaders of North and South Korea have agreed to meet at a summit next month, Seoul’s envoy says. It will be the first such meeting for more than a decade and the first since Kim Jong-un took power in North Korea. Mr Kim is said to be open to US talks and would pause weapons testing during such time. In previous programmes to halt its nuclear ambitions, the North has failed to keep its promises, but ‘risk’ market have nevertheless responded in positive fashion to the news.

President Trump’s tweeted response was that “For the first time in many years, a serious effort is being made by all parties concerned. The World is watching and waiting! May be false hope, but the U.S. is ready to go hard in either direction!”

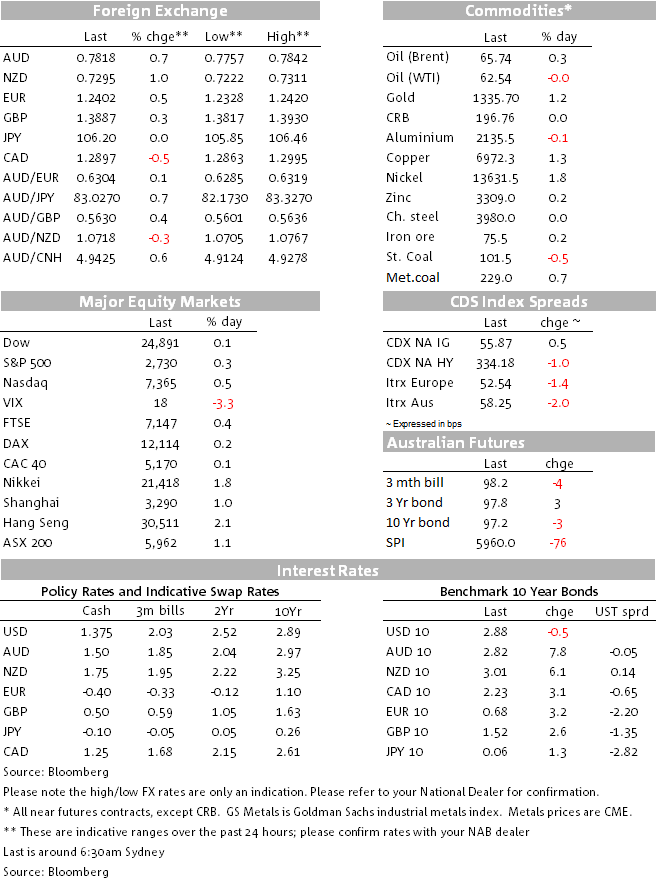

Immediate market response to the news, which hit the wires around 10pm AEDT last night, was more evident in currencies than stocks or bonds, the risk-sensitive AUD, NZD and SEK showing the largest gains with AUD/USD jumping from around 0.7765 to 0.7842 within two hours. This after some choppy but overall limited AUD price action following yesterday’s release of soft retail sales data (+0.1%) but GDP partial data suggesting some upside risk to today’s Q4 GDP data relatively to consensus and an uneventful post-RBA meeting statement.

While the pre-eminent safe haven currency, JPY, did fall-back, the CHF did not and indeed since this time yesterday, both JPY and CHF are marginally stronger. US bond yields aren’t much changed while US stocks are heading into the close slightly firmer.

JPY also weakened a tad after BoJ Governor Kuroda attempted to row back on his monetary policy comments made last week about the possibility of withdrawing monetary stimulus beginning in FY2019. In his daily appearance before lawmakers yesterday he said fewer stimuli before reaching the CPI target is “unthinkable” and that “I said that we would be discussing how to move forward with exit. I never said we would be exiting immediately in fiscal 2019″.

UK Brexit minister David Davis added his voice to UK Prime Minister Theresa May earlier in the week, saying there are good chances of getting a transition agreement in March. That said Bloomberg reports that the EU is planning to keep the final wording on the transitional Brexit agreement on the future trade relationship fairly vague. This would leave the UK in the vulnerable position of having to negotiate substantial chunks of a trade deal after losing much of its leverage.

For now though, getting a transition deal over the line by the March 22 EU Summit should suffice to see GBP/USD back above $1.40 (and in which case AUD/GBP probably goes below 0.55, which would be its best level since the day of the UK referendum). Sterling is slightly firmer overnight but this is largely in the context of a weaker US dollar post the Korea news (DXY -0.6%). The pound is softer against most other currencies.

The NZD is stronger on the Korea news but was unresponsive to the dairy trade auction results, where the 0.6% fall in the GDT index was close to expectations. If anything, the decline was not quite as big as the indicators intimated (the slight positive surprise driven by a 5.5% jump in skim milk powder prices). The GDT Price Index is up 12.2% year-to-date and 9.8% on a year ago.

As for the state of play on trade tariffs, Trump continues to get significant pushback from fellow Republicans. The WSJ reports that top Republicans overseeing trade policy have begun circulating a letter to Trump, warning that tariffs are a bad idea and Congressional Republican leaders aren’t ruling out potential legislative action aimed at blocking such tariffs. Trump’s economic advisor Gary Cohn has been summoning executives from US companies that depend on the metals to meet this week with Trump to try to blunt or halt the tariffs (Bloomberg also reports Trump indicating he thinks Cohn will resign if tariffs go ahead). Meanwhile the EU is reportedly preparing punitive tariffs on iconic US brands produced in key Republican constituencies.

Heading towards Friday’s important US employment report and the March 20-21 FOMC meeting, Dallas Fed President Robert Kaplan has been on CNBC saying “My base case” for the year “hasn’t changed – it’s three for this year, I think we should get started sooner rather than later.”

Australia Q4 GDP where NAB hasn’t changed its original 0.7% forecast following the release of the various GDP partials, neither has the market where the consensus forecast remains at 0.5%. Before this RBA Governor Lowe will be speaking in Sydney at 08:35 AEDT at an AFR conference, on “The Changing Nature of Investment”.

Also in our time zone known Fed dove Lael Brainard will be speaking in New York (11:00AEDT) and Kaplan again, 90 minutes later, at an energy conference. Tonight we get both Atlanta Fed president Bostic and soon-to-retire NY Fed President Bill Dudley.

On the data front, US ADP employment will be released. The Bank of Canada is expected to keep rates on hold (market implied probably of a rise is 13.5%) with NAFTA negotiations freshly overhanging the economic outlook.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

We hear from NAB’s new Chief Economist, as she unpacks the latest economic data with Deb Knight, Host of Money News – 2GB. Watch now.

Video

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.