We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

The US to reinstate tough economic sanctions against Iran, with the threat of secondary sanctions against those who continue to support the regime. Plus last night’s Budget, Theresa May’s split cabinet and the risk of another election in Italy.

https://soundcloud.com/user-291029717/trump-pulls-a-hard-exit-from-the-iran-deal

Seeing ‘Pope Rhianna’ on the Met Gala red carpet last night reminded me that with Tapas Strickland now at NAB in London, there are still a few (albeit very few) unused song titles in her back catalogue available to title our Market Today missive.

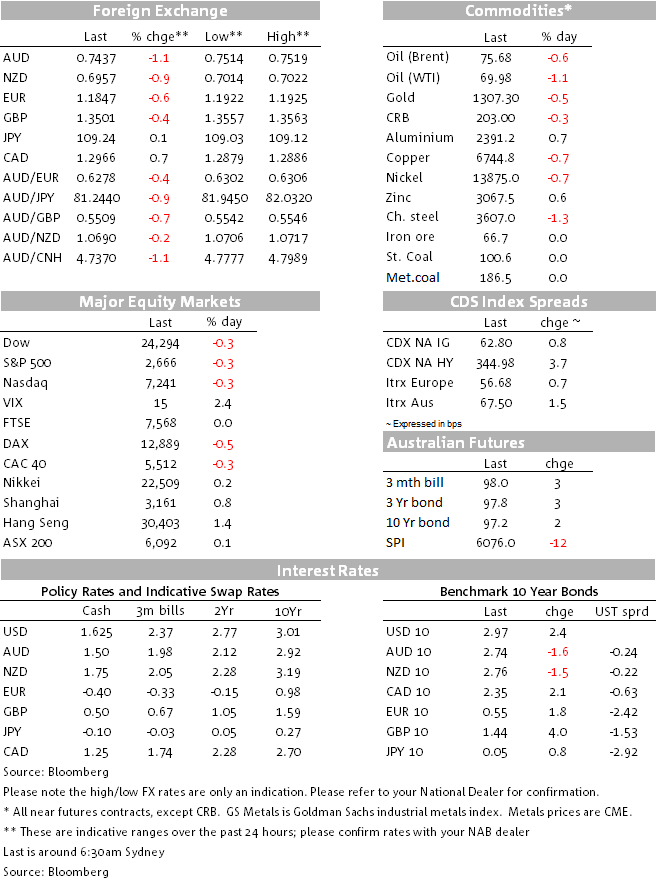

Though markets were on tenterhooks yesterday awaiting President Trump’s decision on whether the US would pull out of the 2015 Iran nuclear agreement, the decision to do so when it came – an immediate ‘hard’ exit and known a few hours before the formal 2pm Washington time announcement – drew only limited market response, consistent with the notion it was mostly ‘in the price’ already. That may be so, but its early days in terms of how the decision will play out in terms of heightened geopolitical stress in the Middle East, even if any physical reduction in Iranian crude oil exports is limited.

All of the other five signatories to the 2015 agreement (UK, France, China, Russian and Germany) appear to remain committed to the deal. The UK, Germany and France have said so while Russia says the US pull out “won’t end its existence immediately” and that it will continue to develop bilateral ties with Iran as well as being open to French proposal for an enhanced nuclear deal. China is expected to ignore any reimposed sanctions and indeed is a potential buyer of more Iranian oil after Saudi Arabia has of late been lifting the premium it charges China on top of the Brent crude benchmark price.

Overall, this further example of US isolationism is something that can continue to erode foreign investor enthusiasm for owning US assets over time, if not right here and now.

The ‘no, yes’ volatility in expectations as to what Trump would do on Tuesday saw the Brent crude benchmark trade as low as $73.10 and as high as $76.18 (the latter just below Monday’s new cycle high of $76.34). It’s ended the NY session at $75.63. WTI crude currently sits just below $70 at $69.71, about $1 back from Monday’s highs. The S&P 500 lost about 0.5% on news of the pull-out but has since recouped all of the loss, keeping the VIX below 15. US Treasury yields were higher into then lower out of the formal announcement, to currently be 2bps up on the day at 2.97%.

In currencies the US dollar has continued to advance, with some support seemingly drawn from Fed chair Jay Powell’s remarks in Zurich. His comments reinforced the Fed’s message that more rate rises are coming (no surprise there). Powell said the market was ‘reasonably well aligned’ with the Fed’s tightening plans while noting that “overall U.S. domestic financial conditions have gotten looser” despite the Fed’s six rate hikes (something we have been stressing for a while now and which plays in favour of more not fewer rates hikes down the track that currently discounted). Powell came across as very relaxed about the ability of other countries to weather higher US rates, in particular Emerging Market economies (though central bankers always say that, don’t they?).

On EM specifically, the Argentine Peso has recovered somewhat after making new lows earlier in the day, after President Macro announced the country had sought a (reportedly $30b) flexible credit line from the IMF. The credit line is seen as a precautionary tool to reassure markets and hopefully to ‘short circuit’ the rapid depreciation in the peso.

Also assisting the USD was the breach of seemingly key levels on some currencies (e.g. 1.19 on EUR/USD and later 1.1875). GBP/USD has so far rejected an earlier push below $1.35. Further USD short covering probably had just as important a role to play as Powell’s comments, which haven’t really told us much we didn’t already know.

Both AUD and NZD have made new 2018 lows in the past few hours, at 0.7434 and 0.6954 respectively, amid fresh USD strength and with commodity prices mostly below Monday’s highs.

AUD did nothing on last night’s Budget (par for the course). As expected, the centrepiece of this year’s Budget is increased infrastructure spending (currently put at A$24.5bn over 10 years), reductions in both personal and company tax and the Baby Boomer package (aimed to allow pension aged residents to fund their retirement in their own homes). Also we have the government committing to a tax to GDP ratio of 23.9% (likely to be triggered by around 2021/22). The latter is largely political but probably means that without significant spending restraint (unlikely in our view) future surpluses will be marginal. Hence there is little to no room for the Budget to adapt to any economic downturn while retaining the projected surplus – and indeed little macro policy flexibility. This, combined with doubts as to whether the projected surpluses will in reality be realised, has been reflected in S&P refusing to lift its negative outlook on Australia’s AAA rating.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.