Firmer consumer and steady outlook

Insight

ACCU discount to global prices is out-of-step with looming step-change in demand. View the full report.

ACCU discount to global prices is out-of-step with looming step-change in demand

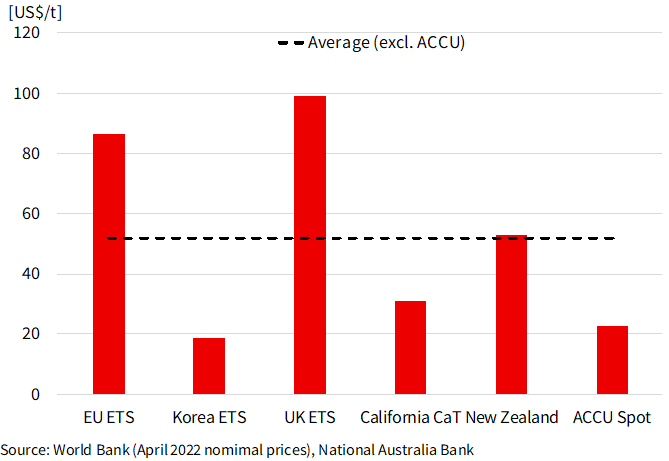

The conclusion of the Chubb review provided an endorsement of the ACCU market, with only minor impacts to our ACCU market outlook balance. ACCU prices remain undervalued in our view and the growing demand for carbon offsets from Australian corporates is set to drive prices higher by 2025 if not earlier. ACCU prices are currently trading at US$22.70/tonne and 60% below global comparable carbon price benchmarks. Recent abatement cost-curve analysis published by the CSIRO highlights ~US$68/tonne or a 100% rise in ACCU prices is implied in order to signal investment in Australian Carbon Capture projects. A steep rise in demand for ACCUs by 2025 is expected to be driven by:

Rising adoption of Net Zero commitments by Australian corporates by 2025. Since 2019 the proportion of S&P ASX-listed Top 50 companies to implement a Net-Zero Strategy has risen from ~30% to 90% and importantly the number of these firms intending to use carbon offsets to support their strategy has grown from ~15% in 2019 to ~65% in 2022 which we expect to underpin a progressive uptick in carbon offset demand.

Australia’s Federal Government has proposed Climate Risk reporting requirements to be implemented by 2025 to align with international standards which is likely to drive increasing participation in carbon offset markets in Australia. On 12 December 2022 the Australian Federal government released a consultation paper which highlighted a gap in the current guidance on Climate Risk disclosures, with potential for increased mandatory reporting on climate risks in Australia from 2025, in line with global recommendations from the Financial Stability Board (FSB). In our view increased reporting and disclosure on climate risks will drive increased engagement from large Australian corporates on Sustainability and Net Zero emission targets which is likely to deliver increased demand for carbon offsets as companies actively manage near term targets and mitigate risks in connection with greenwashing.

CSIRO analysis highlights a step-change in abatement costs ahead. In the CSIRO’s ‘stocktake and analysis of sequestration technologies’ report for the Climate Change Authority the cost of abatement is highlighted to more than double from current cost drivers towards US$68/tonne or A$100/tonne required to underpin investment in Carbon Capture & Storage projects once abatement of more than ~160-170 Mt is required, while we estimate 110-120 Mt of abatement has been delivered already by the current ACCU market.

Australia’s Safeguard Mechanism set to accelerate decarbonisation of the largest emitters adding to ACCU demand to 2030. The current proposal from the Government on our numbers represents ~140 Mt CO2e cumulative increase in emission reductions versus BAU from 2023 to 2030 (ex the Electricity Sector) and is likely to boost demand for ACCUs in our view from FY24. Importantly the new baseline by 2030 will require ~40Mt abatement reductions per annum. In this context, new contracted ACCU supply is estimated at 80 million units by 2030, is only equivalent to 2 years of abatement demand if managed with carbon offsets.

Australia’s LGC prices also signal upside to ACCUs amidst delays in expected renewable energy market penetration. Large-scale Generation Certificates (LGCs) are linked to Australia’s Renewable Energy Target (RET), which was simplistically designed to deliver 33,000 GWh of renewable energy (ca. ~20% of National Electricity Market demand) by 2020. The current LGC spot price is A$55.95/certificate and forward prices remain above A$50/certificate in 2024. We expect LGC prices to fall well below A$20/certificate once the RET is achieved, and current prices indicate delays/shortfalls in LGC production from new renewable energy projects. In our view, delivery on these LGC eligible projects is likely critical to some Australian corporates meeting renewable energy and carbon-emission reduction targets and ACCUs will form a viable strategy to address near term shortfalls in expected renewable energy and net zero emission targets.

Australian’s Renewable Energy pipeline faces ongoing delays according to the Australian Energy Regulator. The Australian Energy Regulator in the 2022 State of the Market report, and AEMO’s 2022 statement of opportunities report highlights delays to renewable generation projects through Covid. We also note Snowy Hydro’s expansion, the Snowy 2.0 pumped hydro project, a key deliverable to support increased renewable electricity generation, was flagged in the Federal Government’s October 2022-23 Budget Strategy and Outlook, Paper No.1 requiring additional equity investment and projects risks including potential construction delays, and cost pressures were highlighted. Continued delays to the addition of firm renewable energy is expected to continue to drive upside risk to –ACCU demand in the medium term.

Chubb Review provides endorsement of the ACCU market. The Chubb Review concluded the ACCU scheme arrangements are essentially sound, which in our view is a positive endorsement for the market. Key changes from the review to our ACCU market outlook are twofold. 1. Panel Recommendation 9, to exclude avoided deforestation from future ACCU projects has a minor market tightening impact, however this is likely to be offset by 2. Panel Recommendation 16 which is proposed to remove obligations under the Climate Active organisation to use a minimum of 20% ACCUs to achieve target emission offsets is likely to see some Australian corporates opting for lower cost offset units such as CERs, VCUs, ESCs and other global carbon offset programs.

ACCUs and carbon offset markets remain an under-appreciated tool by many Australian corporates to meeting carbon emission targets. As highlighted by the 2022 NAB Renewable Energy Survey, link here, most of S&P’s ASX-listed Top 50 companies have now adopted net-zero emissions targets, however less than ~5% of these companies so far have plans to use carbon offsets, highlighting the potential shift in demand from these companies as 2025 and 2030 emission targets approach.

Chart 1: Key Carbon Market Prices

For further FX, Interest rate and Commodities information visit Financial markets, loans, foreign exchange, commodities – NAB. Read our NAB Markets Research Disclaimer.

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.