Family succession on the back-burner? Delay can create unforeseen complications down the track

Article

Growth is key in a low-yield environment. But it’s also vital to protect the wealth you’ve spent years building.

Should you be thinking about greater protection? When it comes to your wealth, absolutely. Consider the current environment. There are any number of events around the globe creating uncertainty for individuals and investors alike – including the upcoming US presidential elections, Brexit and the US-China trade negotiations.

At the same time, global finances are in unchartered territory as we enter a period of very low to zero interest rates.

As NAB Private Customer Executive Jason Murray observes: “I think even the brightest economist may not have a strong view on where the [global] economy will be in a year or two years’ time. There are so many exogenous factors which could influence it.”

Australia remains in reasonably good shape. As NAB Group Economics notes, the housing market is making further progress towards recovery. Meanwhile, unemployment is relatively low and growth is fair, if not surging. “We read a lot in the financial press or general press around the uncertainties, but actually the underlying fundamentals of a strong economy are doing okay,” Murray points out.

However, Australia is also facing a near-zero interest rate environment, and we’re far from immune to a global downturn. “The correlation between how Australia performs relative to the globe is very, very high,” Murray says.

“So if the US and Europe were to go into the recession, it would be very difficult for Australia to escape that.”

Which brings us back to the issue of wealth protection. “I think the notion of protecting your wealth is very applicable to these times, given the high level of uncertainty,” Murray says.

This is brought into sharp relief when you consider Australia’s changing demographic. Many people are on the cusp of retirement; certainly a greater proportion compared to 10 years ago. “It makes it particularly important that high net worth individuals (HNWIs) start to think very clearly about the future,” Murray says. “Protecting [their wealth] is an important element of overall wealth management.”

This isn’t simply a matter of reviewing your insurance policies for your home and your family, although undoubtedly that’s a critical element. Ultimately, it’s about having a clear sense of where you’re at, where you want to be, and how you can best achieve that. It’s only by proactively managing your wealth that you can hope to protect it.

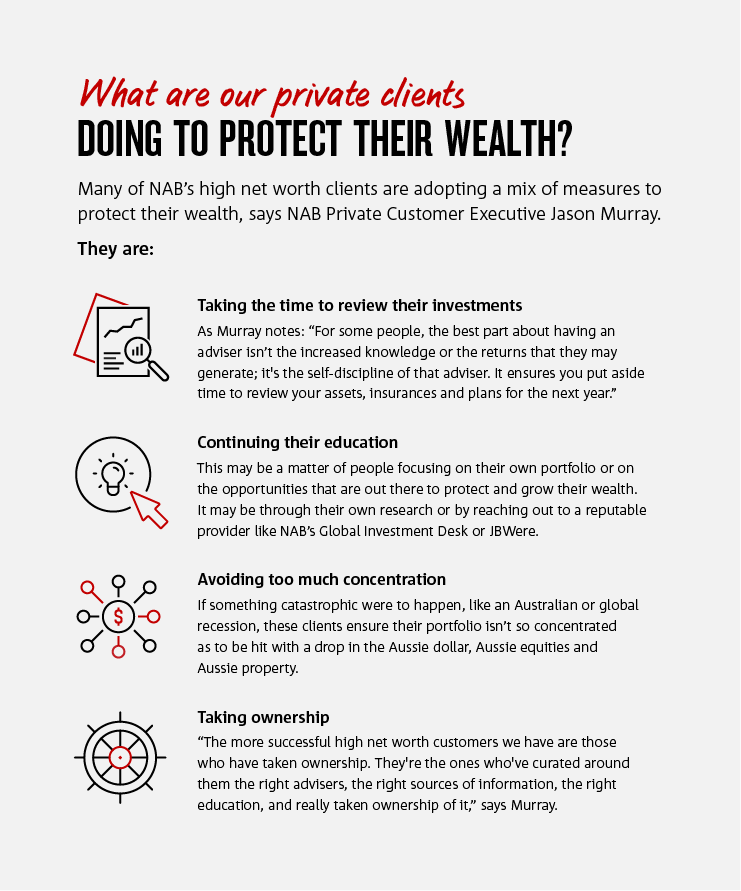

First and foremost, this requires you to draw up a financial plan. “That’s as important for HNWIs, and particularly retirees, as it is for someone in their twenties just starting out,” Murray says.

You should also review your investments – not just once but on an ongoing basis. “You need to have those regular conversations with your financial adviser to ensure you’re up to speed with where your investments are at and what you can do to further them,” Murray says.

However, any such reviews will be relatively meaningless if you don’t have the education and knowhow to support them; to understand what they’re about and whether they’re right for your circumstances in the current environment.

At the end of the day, you need to take ownership of your wealth, Murray says – to understand what you’re investing in and who is investing it. “It’s a matter of ensuring that you are consciously doing the right due diligence and investing in things that you are comfortable with, with reputable and good investment firms, managers and organisations.”

It may be that you’re comfortable with Australian asset classes. However, you also need to consider diversification.

“Australian HNWIs are generally over-concentrated in three asset classes: cash, equities and property; and in one currency: Australian dollars,” Murray says.

The problem with this is it leaves you particularly vulnerable to a downturn. It also means you miss out on opportunities for growth. “For example, if over the past five years you haven’t had exposure to US dollars, you wouldn’t have seen that benefit of the strength of the US dollar or the flourishing US tech sector, for example,” Murray says. “If over the past five years you had nothing in bonds, you wouldn’t have seen the dramatic price appreciation in bonds in a reducing interest rate environment.”

This isn’t to suggest that you should simply take on more risk – although there are those who have found better returns in alternative assets like private equity and unlisted funds.

Fundamentally, diversification is about protecting your portfolio by avoiding concentration in one asset class, geography or currency,” Murray says.

Exposure to enough different asset classes gives you the blended return necessary to beat inflation. “If you leave everything in cash, for example, you may think you’re about as safe as you can possibly be,” Murray says. “But actually you’re not. By generating one per cent, or whatever the current general deposit rates are, you’re not even beating inflation, so your wealth is actually whittling away.”

That might not make a difference in the space of a year, but over a 10-year period it means you’ll inevitably go backwards.

Admittedly, the current financial environment isn’t conducive to reaping stellar returns. As Murray notes: “We’re in a reduced-yield environment across all asset classes, not just interest rates or term deposits.”

Yet protecting your wealth can still be about growing your wealth as well. Upping your expertise and broadening your investment horizons can be a win-win on both fronts.

While this might take considerable self-education and research, you don’t have to go it alone. Arming yourself with the necessary tools can be as simple as reaching out to NAB’s Global Investment Desk – for the more self-direct investor – or approaching JBWere for further insights and advice.

Family succession on the back-burner? Delay can create unforeseen complications down the track

Article

Margin lending can be used to accelerate wealth strategies but picking the right provider to team up with can make a difference to enacting your plan

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.