Family succession on the back-burner? Delay can create unforeseen complications down the track

Article

As investors, growth is something we like to see in the economy. While we have entered a period of decline, we see scenarios emerging later in the year that could create growth and upside for equities.

We have said goodbye to 2022 and there is no doubt it was a challenging year for returns. A rapid rise in inflation, tight labour markets, an aggressive central bank tightening cycle and conflict in Ukraine were just some of the factors that defined the year’s investment environment.

Looking ahead, we think this year will bring its fair share of challenges, but we also believe that there will be some important differences. These include a peak in the interest rate cycle, an eventual cyclical trough in global growth (preceded by recession in the US, UK, and Europe) and a peak in inflation.

In this article we examine how central banks will manage the transition out of a rising inflationary environment and the risks for investors from the different scenarios that may be generated by this transition. We also examine when opportunities are likely to arise in key asset classes as the year unfolds.

The central bank conundrum

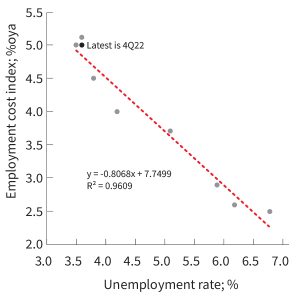

Even wages growth of 3.5% requires a much higher unemployment rate

Source: JBWere and Bloomberg. Past performance is not a reliable indicator of future performance.

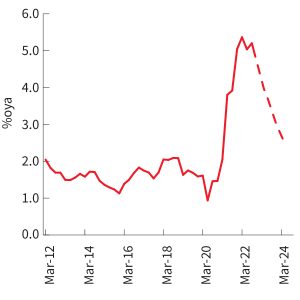

US core inflation (dashed line is consensus forecast)

Source: JBWere and Bloomberg. Past performance is not a reliable indicator of future performance.

Equity markets first half of 2023 – We think investors should consider

For equities to turn more constructive we need

Fixed income looks very attractive

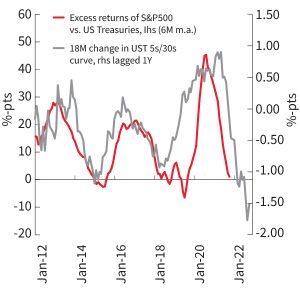

The curve suggests further US Treasuries out-performance

JBWere and Bloomberg. Past performance is not a reliable indicator of future performance.

A final caution

We expect the Fed to pause interest rate hikes about or even before mid-year, but the pain from high rates will continue. Effectively, the Fed needs a protracted period of restrictive monetary policy to ensure that it completes the task on inflation. We don’t think a longer period of high interest rates has been factored into equity markets, and the Australian market has not factored in a recession (even a mild one).

Equity under-performance looks modest, given tightening in financial conditions in the US

JBWere and Bloomberg. Past performance is not an s not a reliable indicator of future performance.

The information contained in this article is gathered from multiple sources believed to be reliable as of the end of December 2022 and is intended to be of a general nature only. It has been prepared without taking into account any person’s objectives, financial situation or needs. JBWere Limited ABN 68 137 978 360 AFSL 341162 (JBWere) is a wholly owned subsidiary of National Australia Bank Limited ABN 12 004 044 937 AFSL and Australian Credit Licence 230686 (NAB). Before acting on this information, NAB and JBWere recommend that you consider whether it is appropriate for your circumstances. NAB and JBWere recommend that you seek independent legal, financial and taxation advice before acting on any information in this article.

Family succession on the back-burner? Delay can create unforeseen complications down the track

Article

Margin lending can be used to accelerate wealth strategies but picking the right provider to team up with can make a difference to enacting your plan

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.