Confidence and Conditions Lift

Insight

NAB’s global debt syndicate teams share their insights on Asia, the US, Europe and the UK debt markets for the year ahead.

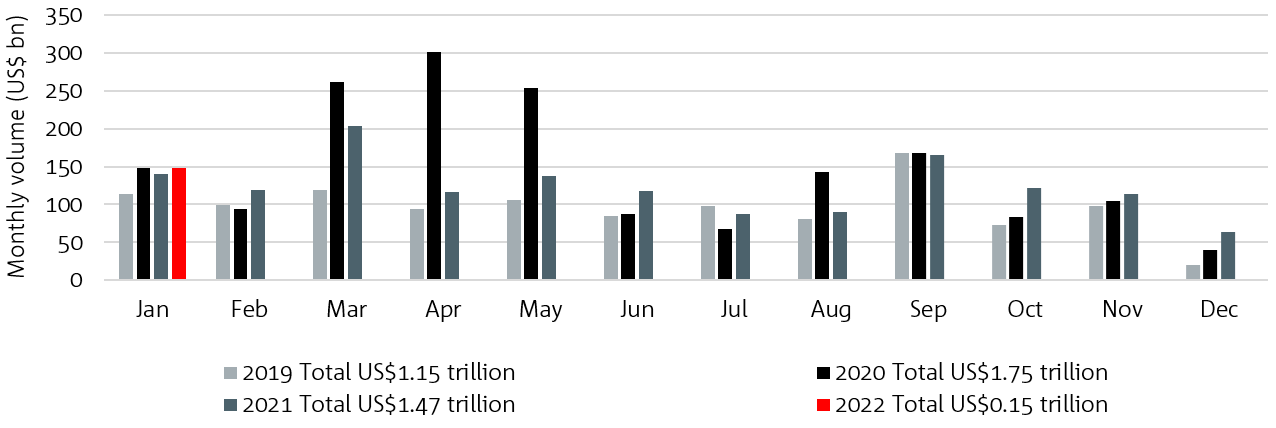

Ongoing market volatility driven by inflation concerns, the Omicron outbreak and central bank meetings saw an earlier than usual close to 2021 on the primary front. The combined effect of the macro influences led to large swings in the rates and swaps markets, while also pushing secondaries wider, resulting in a reduction of new issuance. The supply that did hit screens was more defensive in nature (covered bonds, high grade issuers) and came with higher new issue concessions than previous months to balance the reduction in demand as investors held onto their cash into year end.

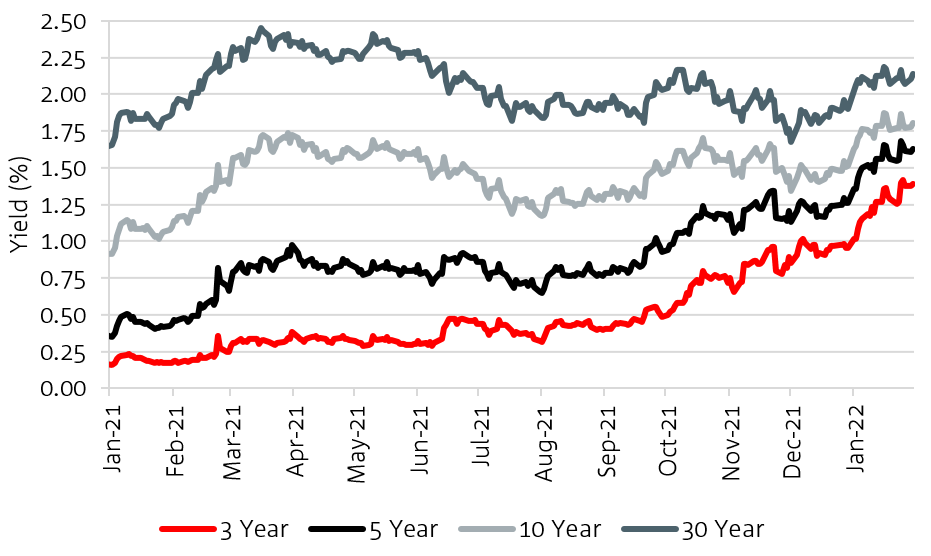

As we open for 2022, many of the macro concerns persist, however some clarity has emerged surrounding direction from central banks: the BoE raised rates in December; the Fed announced a doubling of its tapering to finish stimulus by March while also signalling at least three rate hikes for 2022; and the ECB continued to reiterate plans for a PEPP runoff by the end of March – which is set to be replaced by a regular asset-purchase plan1.

This indication of “faster-than-expected” reduction of support via bond buying schemes and a signalling of rate hikes sooner and higher than expected has fuelled volatility as well as expectations not only of higher rates, but of a widening of credit spreads.

Uncertainty over the further impact of COVID-19 and any future new strains on the global economy will also continue to contribute to this volatility, likely resulting in a more window-driven market for borrowers. It will see investors back in the driving seat after what was a very “borrower friendly” 2021.

Global debt issuance volumes are expected to remain strong, despite rising issuance costs, as evidenced in the first month of the year as liquidity remains abundant and choppy stock markets nudge some investors towards more safe haven assets.

In addition to speculation on the trajectory of rates and the ongoing impact of the pandemic (including ongoing supply chain disruptions and inflation concerns), the increased focus on ESG investment opportunities rounds out the three key themes we expect to see impacting global debt markets in 2022.

The unpredictability of the spread and prevalence of COVID-19 has been one of the hallmarks of this global pandemic crisis. Governments have adopted highly nimble approaches to manage the balance between protecting their populations and their economies.

The impact on global supply chains has seen severe disruptions putting upward pressure on price inflation across key industries, a significant area of concern for central banks.

While the vaccine rollout has made huge headway in offsetting the virus, it has not been a silver bullet. The potential for future variants will continue to induce volatility in the market, however timing and severity will remain unknown, although it is unlikely governments globally will incur the same restrictions and lockdowns while the health system is not overburdened and will look to adopt “live with COVID” strategies.

ESG supply has become normalised in the global primary market as supply surpassed US$1 trillion equivalent globally for the first time ever, Bloomberg data shows2. ESG supply has become a regular feature in the primary markets, with increased rigour around the frameworks and greater scrutiny of the validation and verification evident.

Those that do not issue specifically in green format will continue to come under increased scrutiny with regards to the ESG impact of their underlying operations and certain sectors will continue to be challenged if they don’t meet the expectations of stakeholders and the community.

US IG historical volumes

Source: Above data from Bloomberg, Informa, NAB

US Treasury yields

Source: Bloomberg data

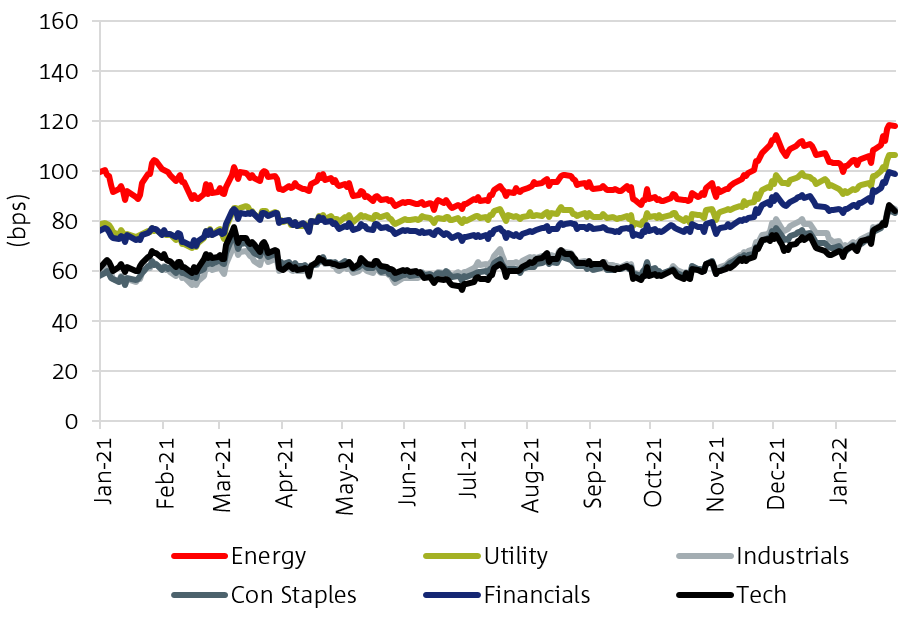

US credit spreads: 10yr ‘A’ band

Source: Bloomberg BVAL Indices

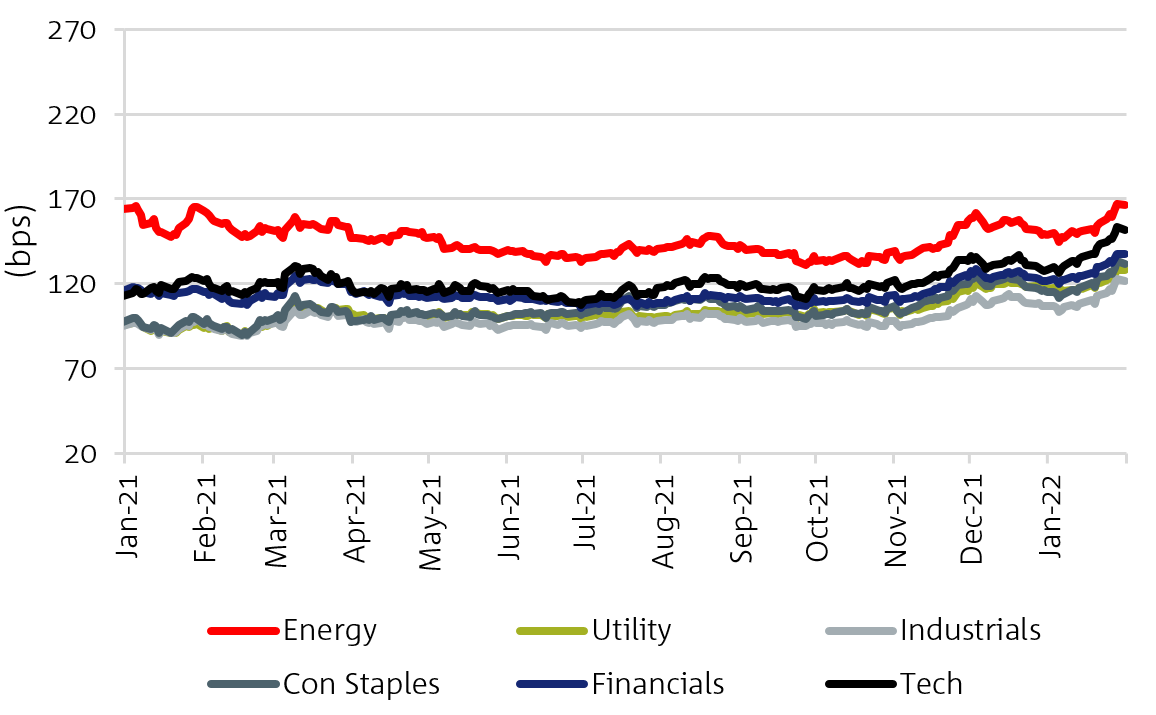

US credit spreads: 10yr ‘BBB’ band

Source: Bloomberg BVAL Indices

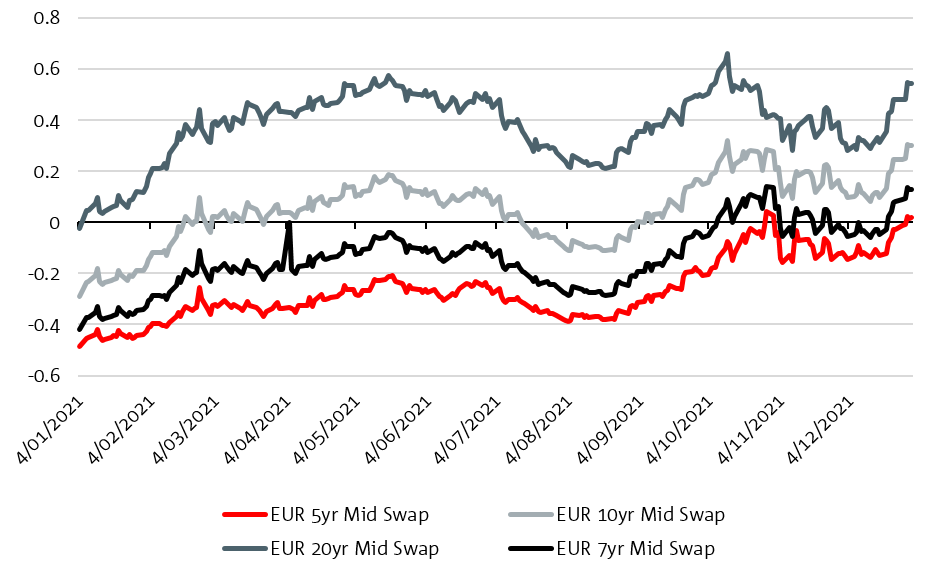

EUR Mid Swaps

Source: Bloomberg data

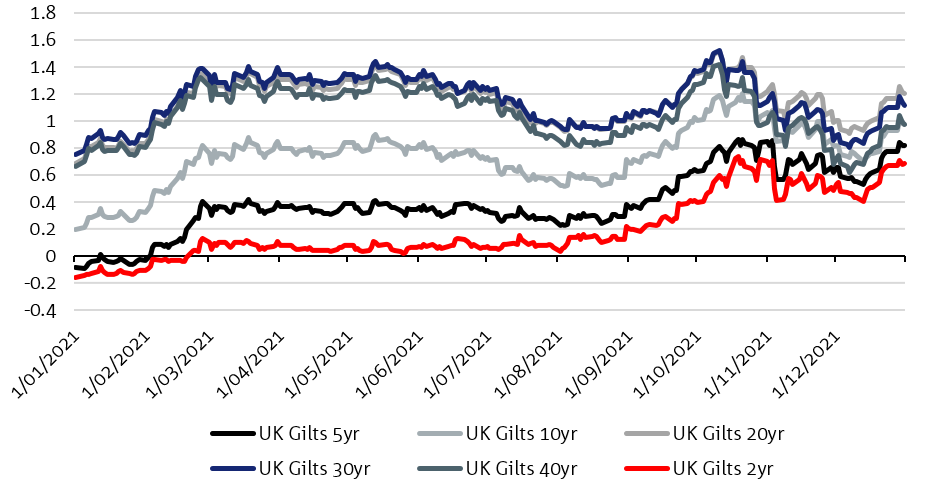

UK Gilts Curve

Source: Bloomberg data

As is the case for G3 currency markets globally, Asian local currency markets will also face into volatility in 2022, as the US dollar and the expected faster pace of US dollar rate hikes impact the attractiveness of those unpegged local currency markets.

While inflation was largely benign in Asia versus the US and Europe in 2021, ongoing higher shipping costs and supply chain disruptions look set to contribute to higher inflation across the region in 2022. This may quicken the pace of rate hikes by regional central banks, however some have already started their rate hike programmes, or simply had previously cut rates to a lesser extent than the US in response to the pandemic. As such we expect local currency bond issuance to remain less attractive for investors than issuance denominated in US dollars.

Adding to volatility across the region, which further impacts the Dim Sum (CNH) and Panda Bond (onshore CNY) markets in addition to the US$ RegS market, are ongoing concerns in the China economy off the back of weakness in the domestic property sector.

The underlying issues, which have resulted in a liquidity squeeze and overall funding shortage, have not yet been resolved and will continue to impact RMB and US$ RegS market sentiment in 2022, which could have a significant knock-on impact on the overall Chinese economy, accounting for circa 30% of GDP (when including related industries). Political risk also remains a potential headwind for China on a number of fronts, which continues to impact demand, not just for China credit, but also for Dim Sum issuance, which has been declining steadily over the course of the past two years.

Investor demand in the HKD market is expected to remain relatively steady throughout 2022, given the HKD FX and rates peg to the US dollar. There also continues to be a significant amount of funds in the currency to be invested, with a strong preference for HKD denominated product amongst investors.

Furthermore, the Hong Kong Monetary Authority (HKMA) has been focused on the further development of debt capital markets to retain its status as one of the most prominent bond markets in the region. In the fight to maintain competitiveness against Singapore, the HKMA have been focusing on how to promote ESG issuance in the jurisdiction.

Hong Kong was the largest market for bond issuance in ESG format from the Asia region, which looks set to continue in 2022 as the government continues to promote issuance in the format through policy, as well as via grant schemes targeted at ESG issuance11.

The SFC in Hong Kong will also be introducing a new Code of Conduct for Intermediaries in both the ECM and DCM markets, which will be effective in August 2022 and which will aim to improve the transparency and efficiency of execution12, again to ensure they provide the best framework for global borrowers to issue.

However, questions remain around the potential extra-territorial reach of the new regulations which could impact all transactions touching Hong Kong. Discussions remain ongoing on this aspect of the new regulation.

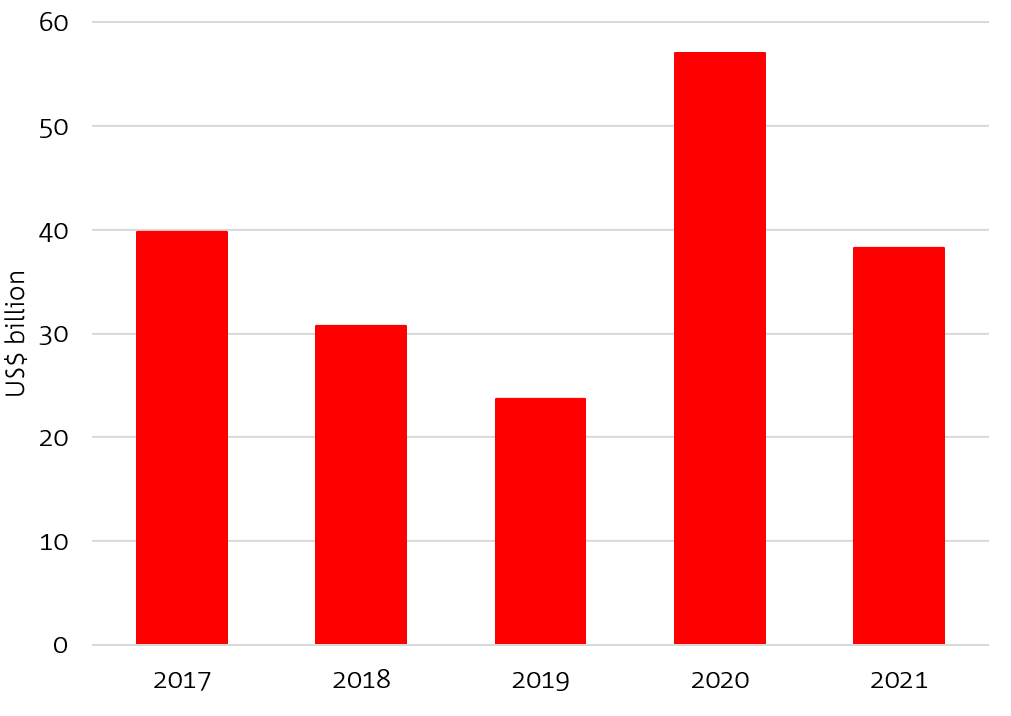

One local market bucking the trend is the Formosa bond market. Strong growth is expected in 2022. After a ~33% reduction in issuance volumes in the format in 2021, January has already seen ~US$6.5 billion of issuance for the month13, which already accounts for 17% of 2021’s total issuance volume.

With potential redemptions of >US$23 billion, investor appetite will continue for US dollar and Australian dollar long-dated callable zero-coupon notes, which make up the vast majority of all issuance in the Formosa market. With long-end rates set to rise in the second half of the year, this market will present borrowers with a good source of cost-effective funding to complement their borrowing programmes in global G3 currency markets.

Historical issuance of US$ Formosa bonds

Source: Graph data from Taipei Exchange as of January 25, 2022

One of the most stable markets in the region throughout the pandemic has been the JPY denominated debt market. While issuance volumes have increased slightly, the share of issuance from offshore borrowers has dropped from ~16% of all issuance in 2019, to ~13% in 202114.

The key driver has really been basis swap moves and the attractiveness of the US dollar market from both a tenor and pricing perspective since H2 2020. The ongoing volatility in the JPY market will continue to make issuance in Samurai/Euroyen formats challenging in 2022, however borrowers who remain flexible and can move quickly will be able to successfully price transactions and achieve good arbitrage value off the back of rate and basis swap moves.

More generally, Japanese investors have been increasingly active, with many being buyers of offshore debt for the first time in 2021. Japanese investors have developed a strong focus for responsible investment, becoming key drivers of demand for ESG format issuance in both bond and loan formats.

With large ticket sizes and less price sensitivity versus other investors, as well a willingness to buy private placements alongside strong appetite for Australian and NZ based borrowers this is a key demographic for borrowers looking to issue in green/sustainability-linked bond and loan formats in 2022.

____________

1 Bloomberg Market Data as of December 15, 2021 and Fed comment from FOMC Statement – Federal Reserve Board – Federal Reserve issues FOMC statement

2 Bloomberg Market Data as of December 23, 2021

3 Bloomberg Market Data as of December 15, 2021/FOMC Statement – Federal Reserve Board – Federal Reserve issues FOMC statement

4 Bloomberg as of December 31, 2021

5 Refinitiv Lipper data as of December 31, 2021

6 Bloomberg as of January 25, 2022

7 Bloomberg News / Market Data as of January 24, 2022

8 ibid

9 ibid

10 ibid

11 For example through the establishment of the Green and Sustainability Bond Grant scheme, as announced on May 4, 2021 – Hong Kong Monetary Authority – HKMA announces guideline on the Green and Sustainable Finance Grant Scheme (GSF Grant Scheme)

12 October 2021 Circular from the HK SFC – Consultation Conclusions on (i) the Proposed Code of Conduct on Bookbuilding and Placing Activities in Equity Capital Market and Debt Capital Market Transactions and (ii) the “Sponsor Coupling” Proposal – Conclusion (sfc.hk)

13 NAB data of executed transactions as of January 25, 2022

14 Bloomberg data as of January 25, 2022

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.