NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Our outlook for the Australian dollar looks at the global forces that shape the currency’s fate.

The course of the Australian dollar (AUD) in 2019 inevitably revolves first and foremost around the fate of the United States dollar (USD). Where the US dollar goes, the Australian dollar (almost) invariably follows, in the opposite direction of course. This is not to say we don’t care, from a currency perspective, how well the Australian economy fares and what that might mean for RBA policy. It’s simply that the AUD’s fate will be shaped more by the global forces operating on it from a combination of volatility in the USD, in commodity prices and the extent to which the financial world is generally a happy or unhappy place.

The significance of the latter can never be overlooked, bearing in mind Australia’s inglorious status as one the world’s biggest net international debtors. Externally owned debt is currently close to A$1 trillion, which as a share of GDP is surpassed only by New Zealand and Spain. This means that when the world’s financial markets start to fret for whatever reason and focus on the return of, rather than the return on, capital, money flies home and the AUD tends to suffer.

For much of 2018, this negative correlation was more evident in relation to stresses in various Emerging Markets (EM), which suffered capital flight as US interest rates continued to rise, reversing some of the inflow evident during the post-GFC period of ultra-low Fed policy rates and Quantitative Easing as a result of the ‘reach for yield’ by US investors in particular.

Alongside, we have witnessed various idiosyncratic sources of pressure on some big EM currencies this year (e.g. Turkey, Brazil and South Africa) and of course China, the latter as the US government imposed, and subsequently ratcheted up, trade tariffs on imports from China. Throughout these developments, the AUD has proved to be the pre-eminent ‘EM risk proxy’, a product of Australia’s strong trade links with EM – China in particular – and the superior liquidity on offer in what is the fifth most actively traded currency in the world.

We would happily be proved wrong, but our working assumption as we head toward 2019 is that President Trump will carry through on his threat to increase the tariff rate on US$200 billion worth of Chinese imports from 10% to 25% from 1 January 2019 and, from February, levy tariffs on the full gamut of Chinese imports (meaning on a further US$267 billion worth of goods). This is because of the depth and complexity of the US’s grievances with China. This includes rules, whether tacit or explicit, governing licensing, joint ventures between US and Chinese firms and intellectual property transfers. The ‘Made in China 2025’ policy has in this respect, further inflamed US senses.

US policy is increasingly focused on persuading US firms to shift manufacturing operation out of China back to the United States, as part of President Trump’s ambitions to ‘Make America Great Again’. Running alongside are cyber-security, geopolitical and related defence concerns. To our minds, this adds up to the Sino-US trade stoush extending well into 2019 and with that the likelihood of the re-emergence of pressures on EM, to include capital outflows from China that if not fully resisted by the PBoC, will mean USD/CNY being allowed to trade above the psychologically significant 7.00 level. This is turn would represent a fresh weight on the AUD given the aforementioned strong AUD links to Emerging Market.

Against this, we should note that global commodity demand currently looks reasonably robust. To the extent China will do whatever it takes to protect its overall growth rate in the face of slower export demand, this is positive for iron ore and coking coal demand (and prices), bearing in mind most Chinese steel production is consumed domestically.

As for where the USD goes next year, one potential source of upward pressure has just receded following the US mid-term elections. Here, the victory for the Democrats in the House of Representatives makes it less likely that we will see even more expansionary fiscal policy courtesy of additional tax cuts. There could be bipartisan agreement for an infrastructure package but only if this isn’t tied to funding for ‘the wall’.

The risk of further loosening of fiscal policy adding to the build of inflationary pressures and requiring a more aggressive tightening stance from the Federal Reserve – supporting the USD in the process – has receded, though it remains possible the Fed will end up raising rates in 2019 by more than the market currently discounts. Yet as the Fed gets close to the point where policy is considered ‘neutral’ we look for the USD to come under downward pressure, especially if the prospect of higher rates in other parts of the world come closer into view.

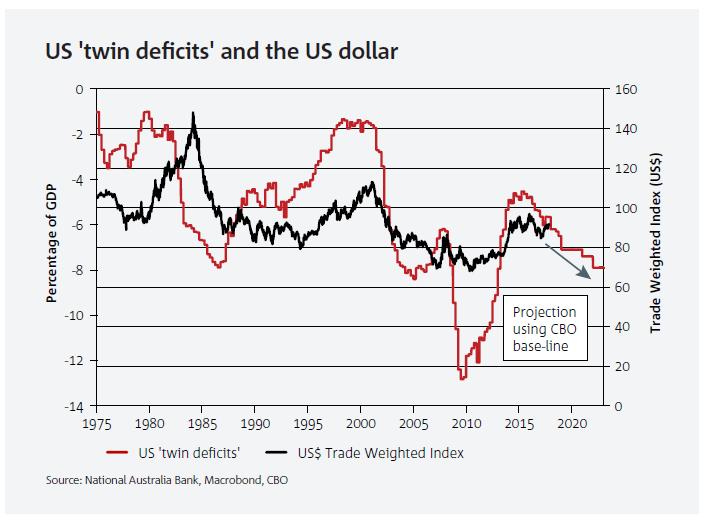

Furthermore, even without further easing in US fiscal policy, budget deficits are slated to get bigger in 2019 and beyond, at the same time that the US trade deficits continues to widen (the impact of US tariffs notwithstanding). The so called ‘twin deficits’ will be widening in coming years, which historically is a recipe for a weaker, not stronger USD. Think of foreign investors demanding either a higher interest rates or cheaper purchase price (weaker USD) to be persuaded to buy ever increasing amounts of US debt.

If the USD starts to move lower as 2019 progresses as NAB’s FX Strategists expect, the flip-side is likely to be an AUD/USD moving back up to, or through 75 cents before the year is out.

This article was first published in 2019 Outlook Creating Opportunities. Read more articles from the magazine.

Speak to a specialist

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.