Long-term signal vs. Short-term noise

Insight

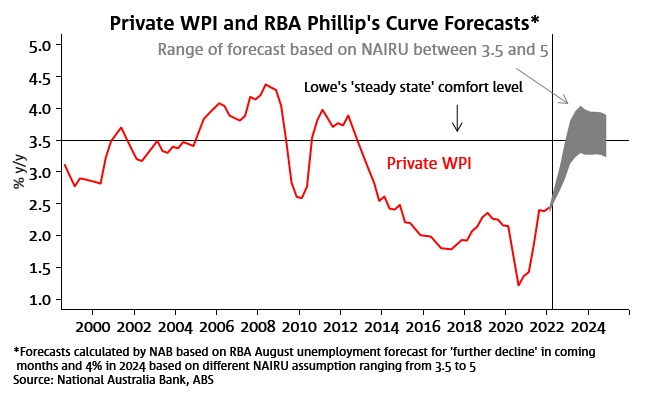

Our analysis in this weekly highlights that the RBA is indeed treading a fine line in trying to chart a credible path to at target inflation.

Chart 1: Wages to accelerate, but how far?

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.