In this Weekly, we dive into last week’s Q3 WPI to explain why the RBA should be more nervous about their strategy and why a near-term pause is unlikely.

The RBA is looking to thread the needle, hoping to return inflation to target while maintaining as much of the improvement in the labour market as possible. A large part of that strategy is based on wages growth remaining consistent with at target inflation. In this Weekly, we dive into last week’s Q3 WPI to explain why the RBA should be more nervous about this strategy and why a near-term pause is unlikely.

The rationale for the RBA’s ‘even keel’ approach is that it is reasonably confident that inflation will fall through 2023 (supply chains easing, some decline in commodity prices, lower global growth from tighter policy in advanced economies). As long as price- and wage-setting behaviour remains consistent with at-target inflation, inflation will return to target. An added uncertainty surrounds the household sector, where “the full effect of the increase in interest rates was yet to be felt in mortgage payments”.

The RBA’s approach of course relies on a wages growth and broader nominal demand backdrop being consistent with inflation at 2-3%. The RBA has previously said WPI growth of 3.5-4% is consistent with at target inflation assuming a 1% productivity assumption. However, last week’s WPI print surprised economists and the RBA and highlighted the risk the longer inflation remains elevated, the greater the likelihood wages become inconsistent with at target inflation.

Q3 WPI rose 1.0% q/q and 3.1% y/y, compared to the RBA’s forecast for a 0.8-0.9% q/q rise. The higher award wage decision this year was a factor, but the details of the release also showed a faster-than-expected acceleration in wages growth among the more flexible parts of the labour market. Private sector wages rose 1.2% q/q and for the 46% of jobs that received a pay increase in Q3, it amounted to 4.3% and had been steadily rising through 2022; last quarter it was 3.8%.

Those parts of the WPI basket that are responsive to labour market conditions are responding and elevated labour cost growth signalled in broader measures is in part reflecting much higher base wage growth. The ABS noted increases for some jobs covered by individual agreements were benchmarked against the award/minimum wage decision but more broadly the category reflects “increases based on end of financial year wage and salary reviewsor interim increases as a retention strategy. ” Note not all the award/minimum wage effect was felt in Q3, meaning the contribution from awards was similar to 2019 with implementation in some industries deferred until Q4. Another strong award/minimum wage increase is also likely in 2023 given elevated inflation.

The RBA has held out that wage and inflation dynamics in Australia are different to other countries, and while that was true over the initial reopening phase, recent data is challenging the assessment that the backdrop is fundamentally more benign. With such risks, we think it is too early for the RBA to consider pausing rate increases, and we expect the RBA to continue in a string of 25bps increases, lifting rates in December, February and March and taking the cash rate to 3.60%. Market pricing of an 80% chance of a 25bp hike at December and February looks too low.

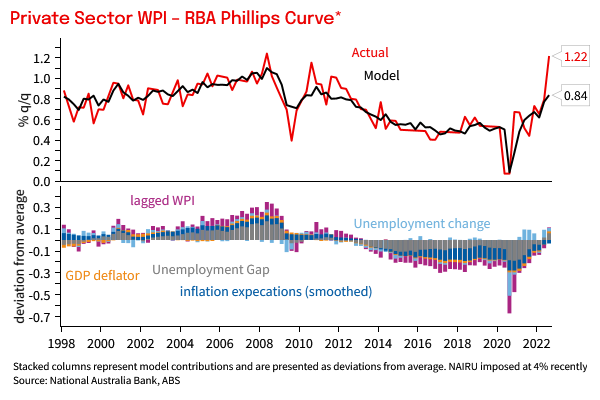

Chart 1: Large unexplained component to the Q3 sharp pick up in wages growth, even after accounting for tighter labour markets