On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

In today’s weekly, we suggest a framework for sifting through the various forces buffeting the 2023 outlook and pose five big questions that we think need to be answered to judge how the economy and central bank policy will evolve in 2023.

This is our final Australian Markets for the year. We will resume publication the week of 16 January 2023. We wish all of our readers a happy holiday season.

1. Goods prices are expected to be disinflationary, but by themselves may not be enough to see policymakers confident inflation will be sustainably back to target.

2. Labour market pressures are expected to ease and wages slow. Border reopening and maturing of the pandemic employment rebound suggest some of the exceptional tightness in demand indicators can slow faster than the unemployment rates rise.

3. NAB forecasts a mild recession in the US in 2023, slower growth in Australia (but no recession), and inflation moving back towards target. Goods and housing are turning, but consumers remain reasonably well positioned, while pent-up demand for services remain. Should central banks reduce restrictive settings somewhat in late 2023/early 2024 a ‘softish’ landing is possible.

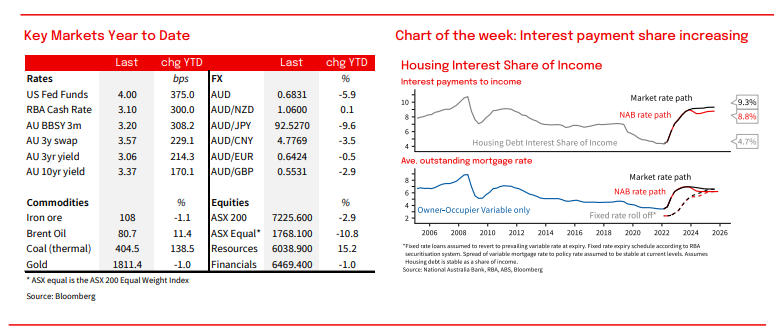

4. With much of the direct cash flow impact of RBA tightening in mortgage payments still to come, we expect slowing to be more evident in Australia in H1 2023. RBA rate increases flow through to repayments with a lag. For many the first 150bp of tightening was simply ‘normalisation’.

5. China’s transition away from COVID-zero is unlikely to be smooth, but markets so far are looking past near-term disruption to a 2023 recovery.

NAB Markets Research Disclaimer

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.