Last week was a big one in terms of RBA communications, with the February Board Meeting, a speech from the Governor and the February Statement on Monetary Policy. From these communications, we know:

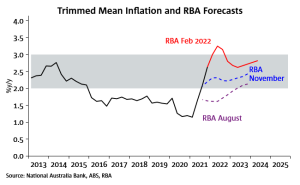

The RBA badly misread the effects of COVID on the economy and in particular on inflation and unemployment, which has resulted in the Bank making the second major change to their forecasts for inflation and unemployment in three months (the table below shows the difference in forecasts from the start of last year);

The RBA describes progress towards the Bank’s goals as having been material and separately that “if realised, the staff forecasts imply that the Bank’s policy goals would be achieved sooner than previously envisaged”. The implication of these statements is that an interest rate rise is closer than the previous guidance

Governor noted in the Q&A to his speech, that there were scenarios where an interest rate rise later in 2022 was plausible. This is in stark contrast to guidance as recently as November that the condition for a rate hike was not likely to be met until 2024, with 2023 only deemed “plausible” and 2022 termed implausible.

The RBA Board is encouraged that it is within sight of the full employment part of its policy mandate. The Board though continues to judge as too early to conclude that inflation is sustainably in the target range. Wages are thought to be key in sustaining inflation at target. The RBA SoMP noted that WA and SA were not seeing a notable increase in wages growth despite a tightening in the labour market. Unemployment has fallen to 3.4% in WA and 3.9% in SA compared to 4.2% nationally.

Importantly though, the RBA has started to broaden its focus for what constitutes sustainable inflation which suggests that while the Board will remain patient as it monitors how the various factors affecting inflation play out and waits for wages to strengthen, it is perhaps not quite as comfortable about inflation as previously.

In assessing inflation’s sustainability, Governor Lowe noted: “We do not have a specific definition as to what ‘sustainably in the target range’ means. The actual rate of inflation is relevant as are the trajectory and the outlook. So too is the breadth of price increases and the factors driving them”. It’s worth reiterating that the RBA’s ultimate policy objective is inflation, not wages.

Further high inflation prints that surprise the RBA could see the Bank shift its stance again. As Governor Lowe noted: “Countries with higher rates of inflation have less scope here [in taking time to obtain greater clarity]”, by inference this signals some upper tolerance to inflation being outside of the target band.