AMW: RBA pricing seems too aggressive over the next 2 years

The RBA clearly signalled it is contemplating lifting rates over coming months, removing language about being “patient” and pivoting the RBA to once again being forward looking.

Analysis: RBA pricing seems too aggressive over the next 2 years

Today the RBA clearly signalled it is contemplating lifting rates over coming months, removing language about being “patient” and pivoting the RBA to once again being forward looking. NAB now sees the RBA hiking in June and we will revise the interest rate track for the remainder of the year in next week’s monthly update. In this Weekly we update our analysis of the market path for rates and implications for households.

We conclude households are well placed to handle the first phase of tightening that we expect this year and next (taking the cash rate to around 1.5-1.75%), but that a further move higher to 3% or above over that timeframe as markets price is too aggressive and would place undue pressure on the household sector.

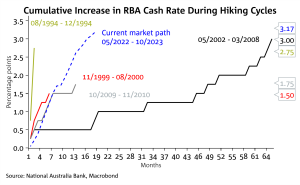

Looking at prior cycles, a lift in the RBA cash rate to 3.25% over the next 2 years would be both higher and importantly much steeper than all cycles in the post 1993 inflation targeting era (1994 was 275bps over 5 meetings; 1999 was 150bps over 9 meetings; 2002 was 300bps over 65 meetings; 2009 was 175bps over 13 meetings).

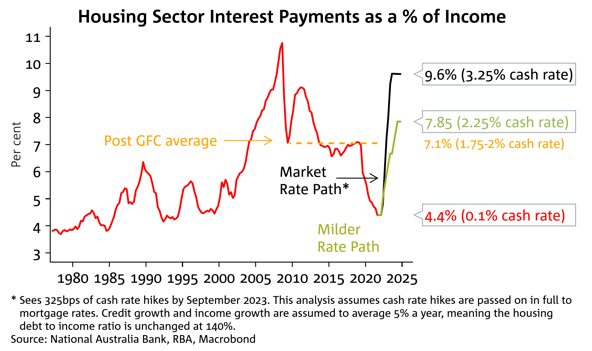

Flowing through the implied 315bps of rate hikes to mortgage rates and assuming full pass through, would see the housing interest payment share increasing to 9.6% of household sector income, its highest since September 2008. Note this does not include principal repayments and assumes household sector income grows by 5% a year, with housing credit also growing by a similar 5% a year to keep debt/income constant.

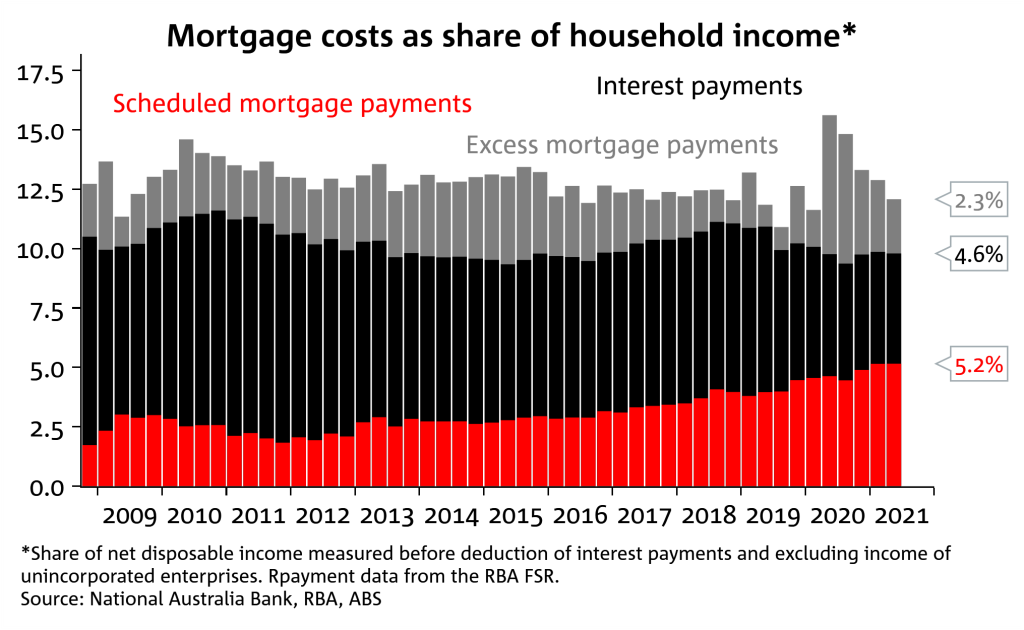

Including estimates of principal repayments would see interest and scheduled principal repayments hitting a record high as a share of income. The RBA calculated in its October FSR that scheduled principal repayments amounted to around 5.2% of household sector income, which was 3-percentage points above the levels in early 2009. Adding on interest payments would then have a combined scheduled repayment at around 15% of household income, above the 13% seen in 2008.

While it is clear the household sector will be able to service a higher mortgage rate (especially given APRA’s minimum serviceability buffers), a rise in interest payments relative to income will have to be financed by a reduction in the savings rate, erosion of the stock of savings, and/or lower consumption than otherwise. The magnitude of the increase implied by higher rates looks too aggressive to us.

As an alternative exercise, we modelled NAB’s RBA call for rates to rise to 2¼% by the end of 2024. This results in a more gradual rise in interest payments as a share of income which would still see interest payments at their highest rates since 2012 as a share of income. Should the spread of cash to mortgage rates widen, interest payments would rise a little further than assumed here.

What does this mean for neutral and the terminal cash rate? It is unclear given household cash flows are just one transmission mechanism for monetary policy and the economic backdrop also matters. Models used by the RBA suggests neutral is around 3.0-3.5%, but we also think there are good reasons to discount these models. The RBA is unlikely to be dogmatic and will be looking at how the data responds to the hikes.

Chart 1: Interest repayments could surge to the highest since 2008 under the market rate hike profile

Chart 2: Including principal repayments would have mortgage repayments as a share of household income at record highs. Note in the post 2012 period, higher debt saw higher scheduled mortgage payments offsetting the decline in interest payments stemming from lower rates

Chart 3: The 315bps of tightening priced by the market would be the highest and steepest tightening cycle in the inflation targeting era

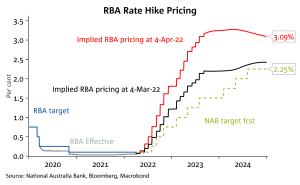

Chart 4: Market rate profile has lifted significantly from a month ago

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.