AMW: Central banks are gear shifting, rather than pivoting

By downshifting the pace of hikes, central banks are acknowledging that decisions are becoming more finely balanced as they tread a fine line of returning inflation to target, while avoiding significantly overtightening policy and slowing the economy more than needed.

Analysis: Central banks are gear shifting rather than pivoting

Markets have been pre-occupied over whether the US Fed will downshift the pace of hikes in December from its 75bps a meeting. Talk of a downshift follows the RBA’s surprise decision to downshift to 25bps in October, and the BoCs decision to downshift to 50bps last week, all coming after central bankers met at the IMF last month. Last week’s FOMC meeting also raised the possibility of downshifting.

By downshifting the pace of hikes, central banks are acknowledging that decisions are becoming more finely balanced as they tread a fine line of returning inflation to target, while avoiding significantly overtightening policy and slowing the economy more than needed. The logic of front-loading the hiking cycle enabled central banks to move away from accommodative setting quickly, but with the level of rates higher, central banks can buy time to assess how the economy is responding to higher rates/tighter financial conditions, and the cut to real incomes from too high inflation.

Downshifting buys time to see whether there are any reversals of pandemic trends that have driven inflation and could reduce the task for policy in getting demand and supply back into balance. Supply chains are easing, and freight rates have fallen back to almost pre-pandemic levels on some international routes. Against that backdrop goods consumption has remained elevated, and there has been pent-up demand for services, which has allowed firms to pass on higher input costs, and in some cases lift margins.

But there are risks. Inflation pressures could become more entrenched if inflation psychology/expectations shift, necessitating a higher level of rates than otherwise and a larger slowing in activity. On the other hand, the risk of not downshifting is that central banks overtighten policy given policy acts with long and variable lags which then leads to a severe recession. There are “no easy outs to restoring price stability”.

Each central bank will view the above risks slightly differently, with those weights determined by economy-specific factors, as well as potentially different mandates. For the RBA achieving a soft landing appears to have a higher priority than for the US Fed, which leaves the RBA exposed should inflation prove more durable.

The most recent SoMP noted uncertainties make “…the Board’s objective of returning inflation to target while keeping the domestic economy on an even keel a narrow one”. If the RBA is wrong on this balancing act it will need to adjust course. Part of the reason for caution is the potential sensitivity of households to rate rises. The bank reporting season highlighted that rate rises seen in Jul-Aug are still flowing through to higher repayments; those in Sep-Nov will flow through in 2023.

In the US Chair Powell noted that there is a greater risk from not tightening enough than from overtightening. That is, risks are asymmetric in that you can always cut if you overtighten. For achieving their twin goals of price stability and full employment requires “forceful steps to moderate demand so that it comes into better alignment with supply…Reducing inflation is likely to require a sustained period of below-trend growth and some softening of labor market conditions”.

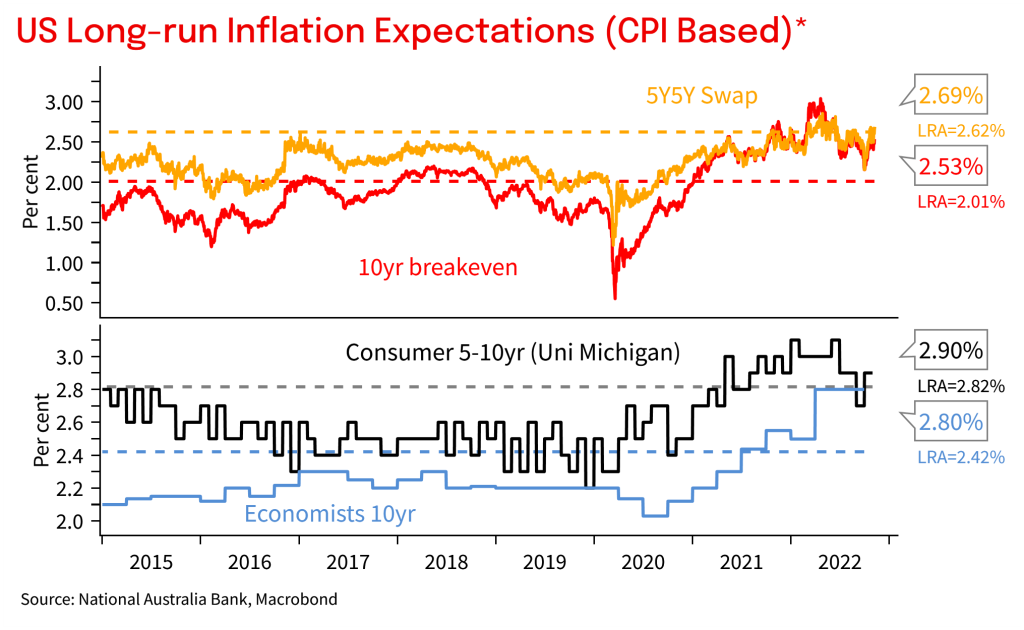

Chart 1: Inflation expectations are a little above long-run average levels, meaning central banks need to remain hawkish

Chart 2: Signs suggest rates are in restrictive territory with lending standards tightening noticeably in the US

Chart 3: Good reasons to think Australian consumers will be more sensitive to interest rate increases when rates pass through occurs. The bank reporting season notes cash rate increases in July and August are still flowing through to variable rate mortgages via higher minimum repayments, with increases in September, October and November likely to be felt in early 2023