CPI Preview: Q3 CPI seen +1.6% q/q on trimmed mean and 1.3% on headline

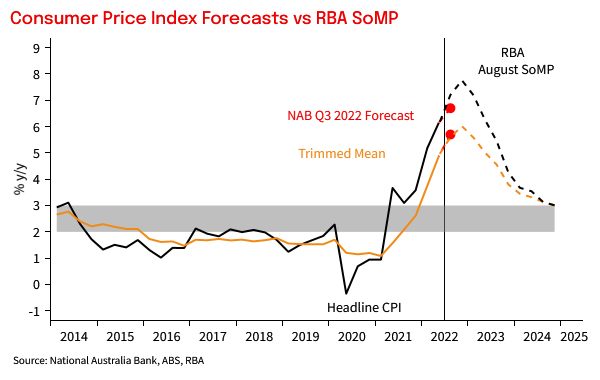

Q3 CPI is on Wednesday 26 October and we forecast Headline of 1.3% q/q and 6.7% y/y. For the more closely watched core trimmed mean measure, we look for an increase of 1.6% q/q and 5.7% y/y. It is a complicated set of risks around those forecasts with uncertainty on whether new dwelling construction costs are sufficiently high to be again trimmed out, and thereby skew the core inflation basket higher. We think they will be, but if they aren’t then trimmed mean could be as much as a ¼ point lower.

The RBA is already braced for a further acceleration in inflationary pressure. The August SoMP profile implied a 1.6% q/q and 5.6% y/y for trimmed mean. Of more importance will be what the detail says about inflation outlook. An upside surprise would pressure the RBA’s contention that the inflation backdrop in Australia is fundamentally more benign than seen in the US. So too would a sharper acceleration in services inflation which would then suggest inflation psychology has shifted. For the November RBA meeting we expect a 25bp hike, but a shift back to 50bp cannot be fully discounted if the CPI surprises sufficiently high and broad.

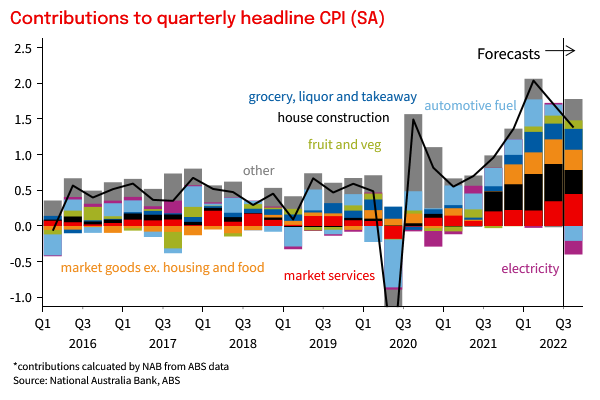

We expect headline inflation to print 1.3% q/q, which would be the first time since the initial COVID shock of Q2 2020 that headline prints noticeably below core. The key items subtracting from inflation in the month are a 5.5%q/q decline in fuel prices (-0.2ppt contribution), and an estimated 8% q/q decline from electricity prices (-0.2ppt contribution) due to the anticipated effect of rebates on measured prices despite large underlying increases in prices in the quarter. Each of these categories will contribute positively to inflation in Q4 as the effect of rebates unwinds and the end of the fuel excise cut adds to petrol prices. We pencil in a 2.0% q/q headline print for Q4, taking y/y to 7½%.

Driving our Q3 forecast is high and broad-based inflation. Goods price inflation is seen remaining elevated as upstream cost pressures continue to flow into consumer prices amid still buoyant consumer demand, even as evidence mounts that material disinflation across goods is likely to occur in 2023. Food and grocery inflation is expected to remain high, while market services inflation is forecast to accelerate further in Q3. Helping boost market services inflation on top of the underlying inflation pressure is the unwind of restaurant voucher schemes in Sydney and Melbourne, and the partial unwind of domestic holiday vouchers, that had weighed on prices in recent quarters.

We expect the breadth of price increase to support underlying inflation in the quarter as price pressures across consumer goods, food and markets services overlap amid the strong demand backdrop. That’s despite some moderation in the right-skew of the prices distribution that had supported the trimmed mean in recent quarters. As a result, our forecast for weighted median, which is less sensitive to price increases in the top quartile, is also for a 1.6% q/q, after lagging trimmed mean in recent quarters. The outsized impact of new dwelling on the distribution of price increases may mean the quarterly peak in trimmed mean inflation may occur in Q3, with indicators such as the average value of a residential building approval starting to stabilize after having increased substantially over the past year.

For more detail on our forecast and a detailed discussion of the drivers, see attached report

Chart 1: RBA braced for high inflation in Q3

Chart 2: We expect broad based contributions to CPI in Q3