On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Markets will be looking for any clues from the RBA Board Minutes as to whether the RBA might step down from its 50bps rises back to 25bps.

This week

It’s a relatively quiet week on the Australian data front this week, with really only the RBA Board Minutes tomorrow and a speech by Deputy Governor Bullock on Wednesday, which will review the RBA’s bond purchase program and presumably conclude that active QT is still not under consideration. Markets will be looking for any clues from the Minutes as to whether the RBA might step down from its 50bps rises back to 25bps (NAB changed its call on Friday to suggesting that enough moderation in demand had yet to be seen in the presence of what the Governor described as shifting inflation psychology in his semi-annual Parliamentary testimony).

There’s a lot more action offshore, with the Fed and BoJ meetings looming large early on Thursday morning and during Thursday respectively. The BoE also meets. NAB expects the Fed to produce another 75bps increase in rates and thinks any change in the BoJ’s YCC policy would be significant for interest rate markets and especially the USD/JPY, which has weakened significantly in recent months. Australian markets are closed on Thursday for a National Day of Mourning for Queen Elizabeth II.

Analysis

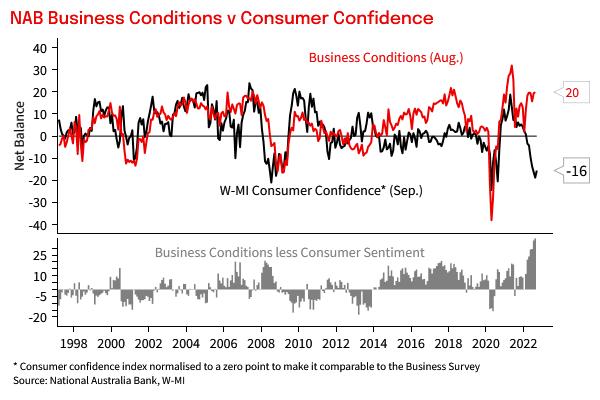

Our delve into the entrails of the NAB Business Survey and the Westpac Melbourne Institute Survey of Consumer Confidence helps explain the current record divergence between consumer confidence and businesses’ reports of very elevated business conditions in the NAB Business Survey, namely:

Lags in the impact of recent interest rate rises are also likely an important part of the story, with banks taking around three months, minimum, to implement higher repayments for consumers with mortgages after rate changes occur. This places a large part of the recent rapid mortgage rate changes beyond the monthly timeframe response of the NAB Business Survey, though the sentiments are captured in the forward-looking responses of some of the questions in the consumer sentiment survey. The elevated survey response on profitability also suggests that businesses are currently able to pass on higher input costs relatively well.

It’s likely that the current divergence resolves when the much higher interest rates put in place by the RBA over the past five months – and in prospect over the next couple of months as well – eventually show up in significantly increased mortgage repayments by consumers. That can be expected to be impacting the Australian economy more significantly from the December quarter of this year and into the first half of 2023.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.