AMW: Fed Pressure Index and recession signals from the US ISMs

A key issue for markets is whether the US economy is headed for a recession in 2023, and when can we expect a meaningful moderation in inflation that would then enable the Fed to start to pivot

Analysis: Fed Pressure Index and recession signals from the ISMs

A key issue for markets is whether the US economy is headed for a recession in 2023, and when can we expect a meaningful moderation in inflation that would then enable the Fed to start to pivot, pause and then cut rates sometime in H2 2023 as the market is currently pricing. In next week’s Weekly we will explore these themes in more detail.

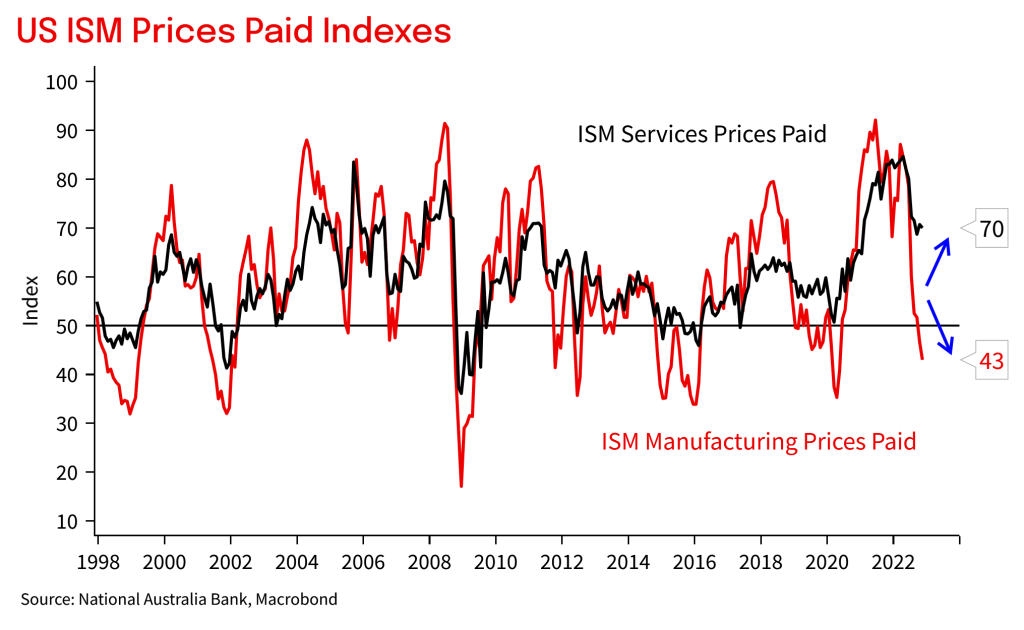

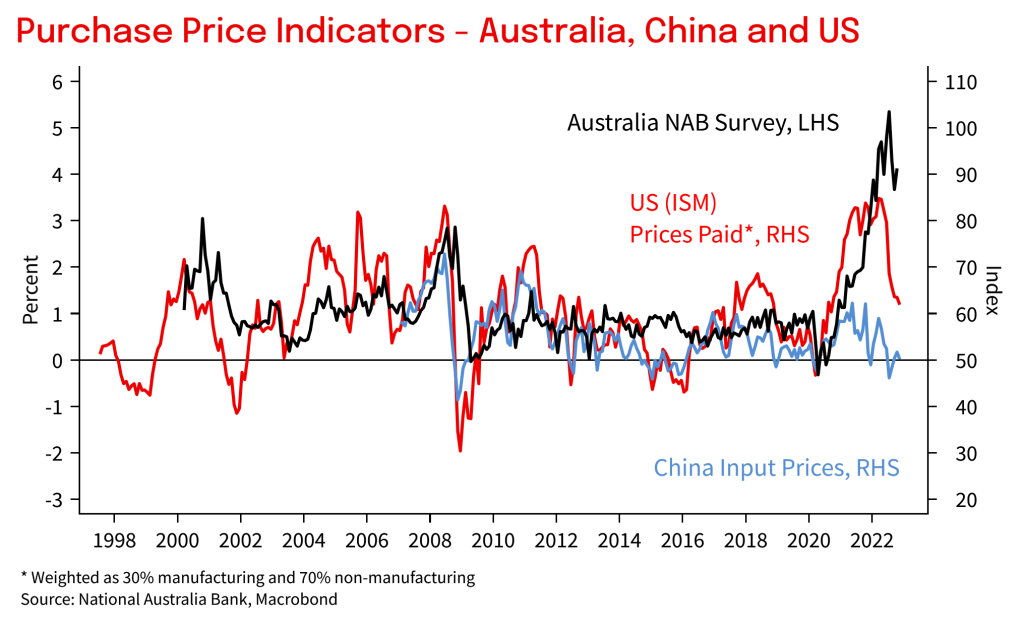

In this Weekly we update some indicators of inflation pressures and recession indicators out of the US ISMs that came out in the past week. In summary we note price pressures in the Manufacturing ISM have eased considerably over the past year, but price pressures in the Services ISM remain elevated. The divergence between the manufacturing side and the services side in terms of prices is one of the largest in the history of the two surveys (see chart 1 below).

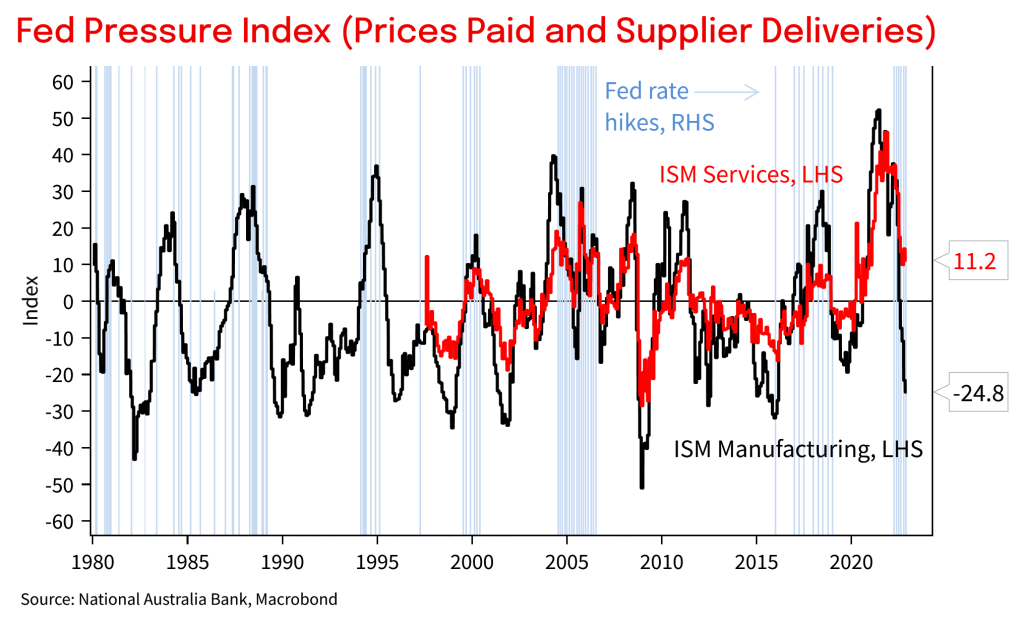

In prior Weeklies we have also highlighted our ‘Fed Pressure Index’ which takes the Prices Paid and the Supplier Deliveries indexes from the manufacturing survey, and which have historically provided a good read on both inflation pressures, as well as the Fed hike cycle. Updating this index on the manufacturing side suggests inflation pressures have eased considerably and is more consistent historically with cutting rates rather than hiking. However, on the other side the services version of the ‘Fed Pressure Index’ is still too high and thus should see the Fed continuing to hike rates.

The above analysis underscores US Fed Chair Powell’s recent analysis of the inflation figures where he split inflation into goods inflation, housing services, and core services other than housing. Powell’s analysis noted that goods inflation should ease, housing services inflation should start to ease over the next year based on new rental lease data, but importantly there have been few signs of any easing in ‘core services other than housing’ which is also the largest of the PCE categories. Wages growth is a key driver of services inflation and markets will remain very sensitive to wage indicators.

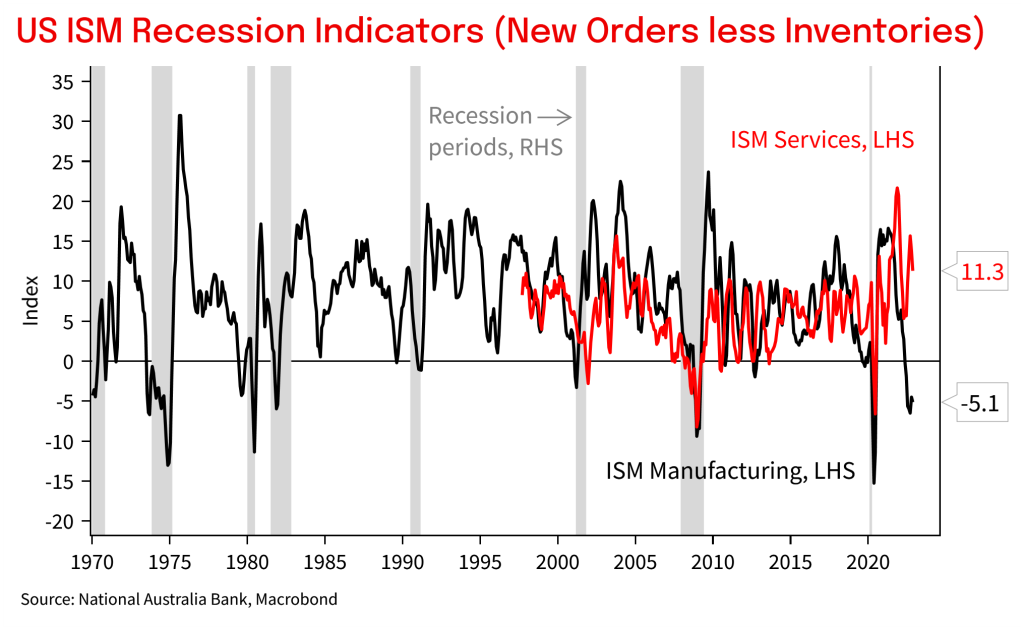

Components of the ISMs have also been used as a leading indicator of recessions, particularly the gap between new orders and inventories. Again, on the manufacturing side, recession risk appears high. But on the services side, recession risk seems much lower. The key difficulty in interpreting the usual leading signal from the more interest rate sensitive manufacturing side is separating any broad cyclical slowing from a ‘natural correction’ from very elevated goods demand during the pandemic.

What does this mean for Australia? Input prices on the manufacturing side are starting to ease and Australian businesses should start to be seeing this as well. In our NAB Business Survey the input price series has tended to lag the US ISMs in this cycle, likely due to the delta lockdowns that Australia had back in 2021 which delayed the inflation pressures being seen on the services side of the economy. In your scribe’s conversations with clients, many are now seeing lower freight rates, and starting to see lower prices on imported intermediate inputs such as steel and wood.

Chart 1: Large price divergence between manufacturing and services

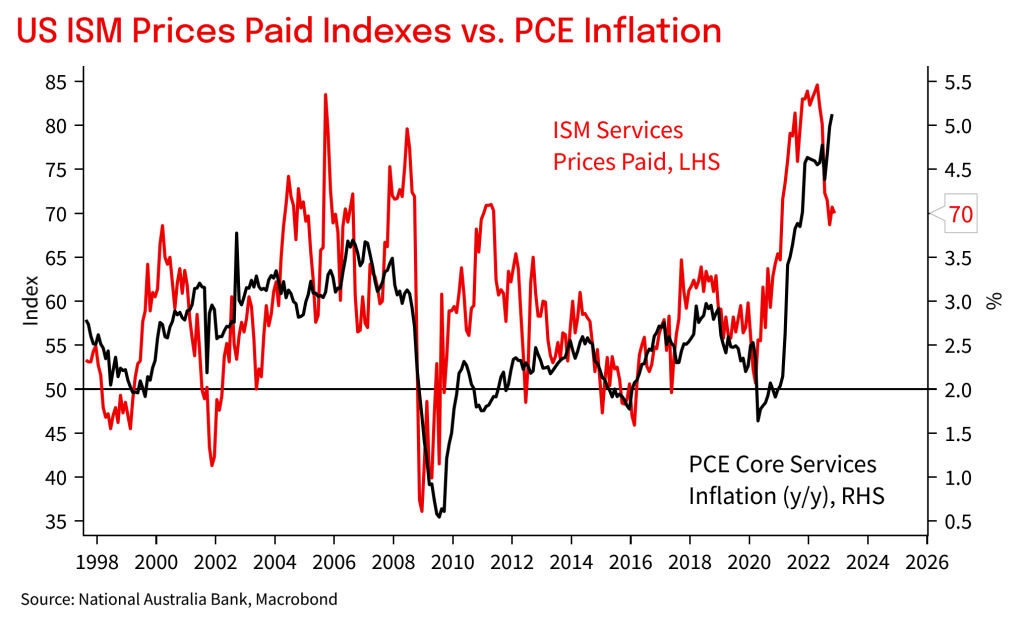

Chart 2: ISM Services Prices Paid suggests near-term PCE core services inflation will remain high

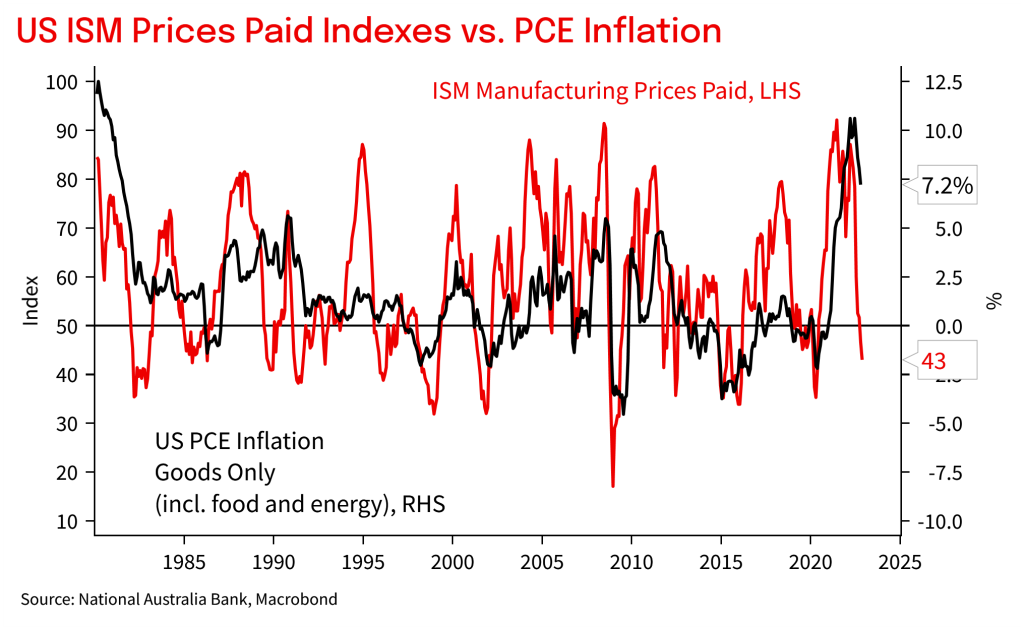

Chart 3: ISM Manufacturing Prices Paid suggests near-term PCE goods inflation should ease considerably

Chart 4: Our Fed pressure index on the manufacturing side is more consistent with the end of the hike cycle, but on the services side is consistent with more rate hikes

Chart 5: Recession risk is elevated on the manufacturing side, but not on the services

Chart 6: Some input cost relief should start to be felt by Australian businesses