AMW: Household sector starts to respond to higher rates

In this Weekly we shine a spotlight on the household sector and what trends are starting to show as households react to higher interest rates and above-target inflation.

Analysis: Household sector starts to respond to higher interest rates

In this Weekly we shine a spotlight on the household sector and what trends are starting to show as households react to higher interest rates and above-target inflation.

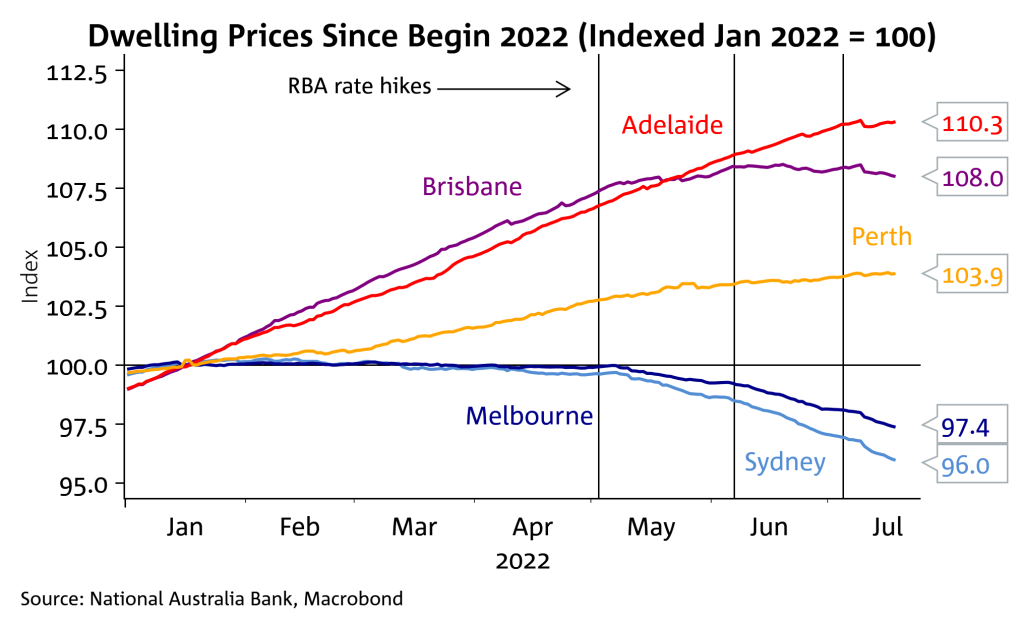

It is still very early to assess the impact fully, but from the limited data to date the most pronounced effect has been on the housing market with Sydney dwelling prices down some 4% since the beginning of the year and Melbourne prices down 2.6%.

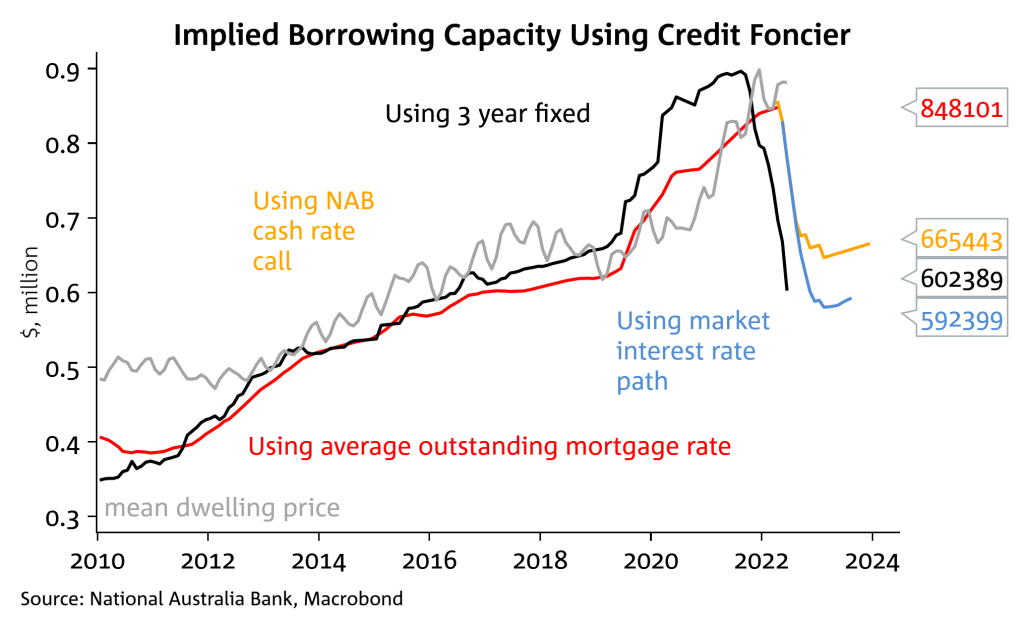

NAB recently revised its house price forecasts, seeing an 18% decline over the next two years, mainly attributable to less borrowing power from higher rates. Updating our models with NAB’s cash rate assumption sees borrowing capacity fall by 22%.

RBA modelling suggests if house prices were to fall 20%, the share of loans in negative equity would only rise to 2.5%. A milder house price decline of 10% would see just 0.4% of loans in negative equity.

A larger fall in theoretical borrowing capacity occurs when assuming fixed rates or market pricing for the cash rate which gives a 32% fall in borrowing power. Regardless of which cash rate assumption is used, house prices will likely continue to correct, though not necessarily as significantly as borrowing capacity.

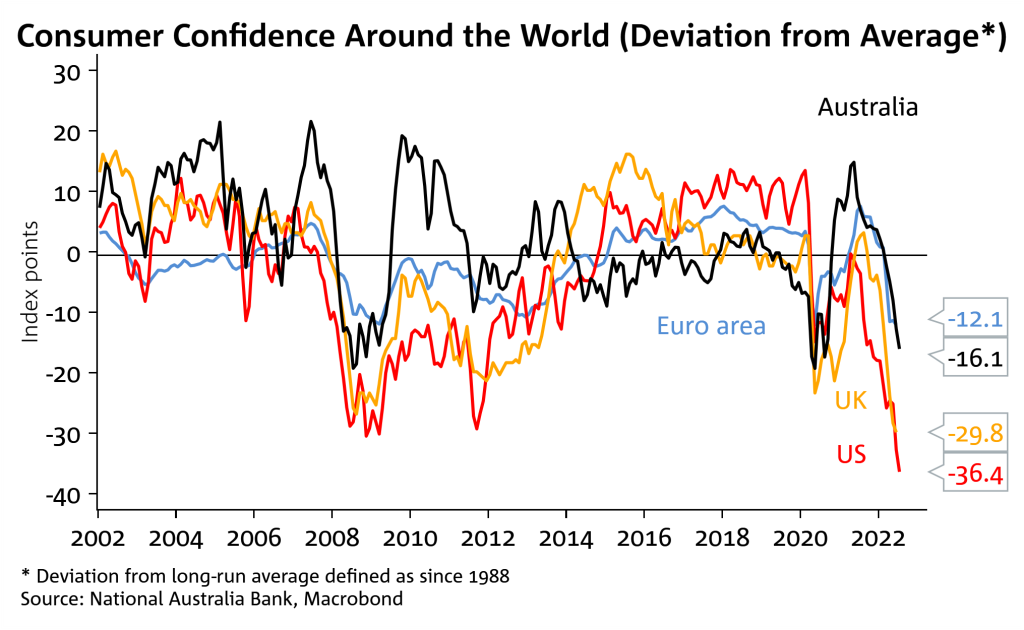

Consumer confidence has also shown a sizeable hit, but the details show much of the decline is due to too high inflation. Since July concerns around interest rates have also risen with those surveyed post RBA having confidence levels 7.4% below those surveyed prior.

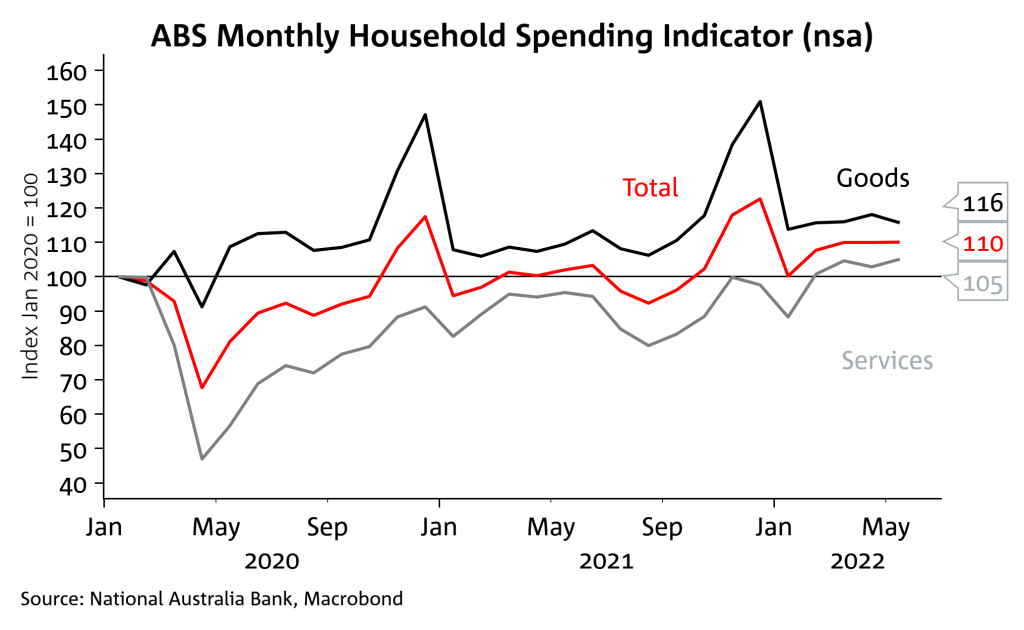

Consumer spending overall has been resilient according to retail sales data for May, though a wider measure of spending based on bank transactions data suggests spending may be starting to slow with little to no growth in April and May.

Overall, it seems households so far are proving resilient to the combination of both rising and higher inflation, likely supported by strong labour markets. That should keep the RBA for now hiking relatively aggressively.

The RBA Minutes just out and a speech by Deputy Governor Bullock suggest the RBA will keep hiking relatively aggressively:

The RBA Board had assessed the cash rate at the July meeting as being “well below the lower range of estimates for the nominal neutral rate”. Neutral has been held out by the Governor to be around 2.5%, while models give a rate closer to 3%.

Bullock revealed modelling rate rises on individual borrowers which assumed “mortgage rates rise by around 300 basis points, which is broadly informed by recent market pricing”.

Bullock reinforced the importance of monitoring trends in the household sector: “the Board will be closely observing…how households respond to the combination of rising interest rates and prices”. Bullock also noted that it was necessary to get rates up to some concept of neutral, which is a fair bit higher than where we are.

Chart 1: House price falls gather pace

Chart 2: Implied borrowing capacity has fallen with higher rates

Chart 3: Consumer confidence is at recessionary levels

Chart 4: Consumer spending indicators based on bank transactions data might be slowing, but the data is non-seasonally adjusted

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.