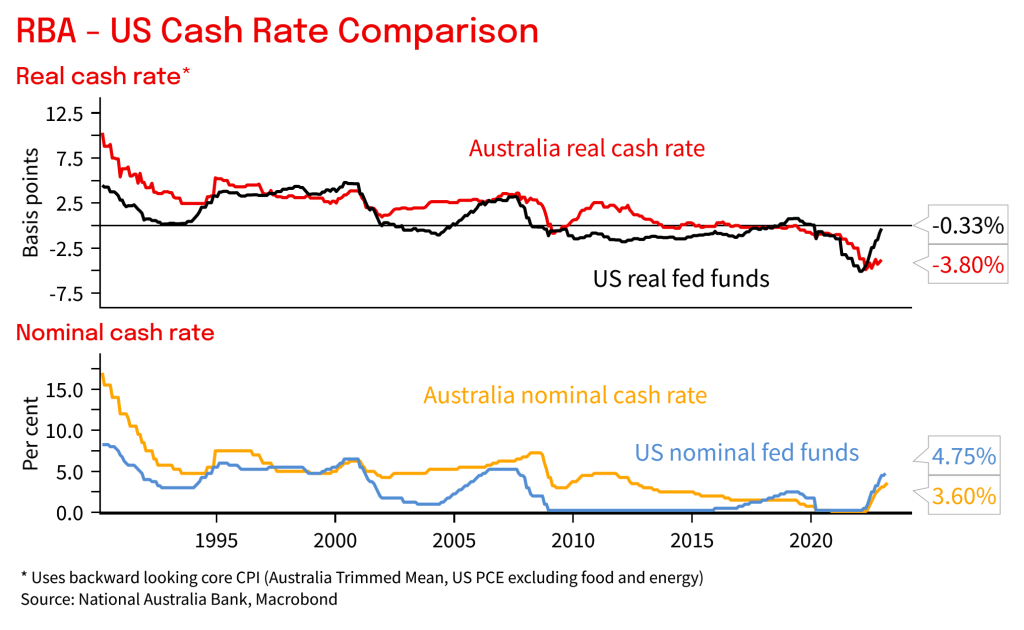

Is Australia different? is a key question for the outlook for rates given the US Fed looks like it will get its fed funds rate to >5.50% (markets price 5.64%). If the RBA lifts rates to 4.10% as is our central forecast, then that would mean a differential of at least 140bps. Such a large divergence has occurred once in the inflation targeting era. In real terms, it would be the largest on record using backward looking core CPI.

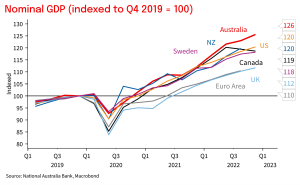

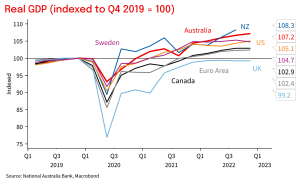

In this Weekly we delve into last week’s GDP figures to show how Australia compares on both nominal and real activity relative to other comparable countries. In short Australia has outperformed with both nominal and real GDP higher than other countries relative to pre-pandemic. That prompts the natural question of whether the RBA cash rate will need to get higher and closer to other comparable countries. Overall, we still expect cash rates to peak lower in Australia than offshore.

The RBA certainly holds out Australia is different to offshore with Governor Lowe today noting wages growth is consistent with the inflation target, and the potential interest rate sensitivity of households given the prevalence of variable/short-term fixed rate mortgages. Even though we broadly agree with these differences, it is still unclear how far Australian interest rates will peak below rates offshore. Meanwhile while Lowe has floated the idea of pausing, US Fed Chair Powell is more hawkish.

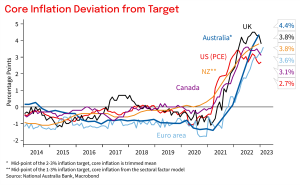

On wages, in Australia the latest WPI and broader measures of compensation were strong relative to pre-pandemic, but not red hot. The labour market nevertheless remains tight given the unemployment rate is around the lowest it has been in 50 years at 3.7%, and the increase in job vacancies is similar to that seen in the US and NZ. In client meetings, wage pressures remain front and centre, but as some of the pandemic influences on the labour market recede, we think the labour market can continue to cool, especially given a recovery in migration.

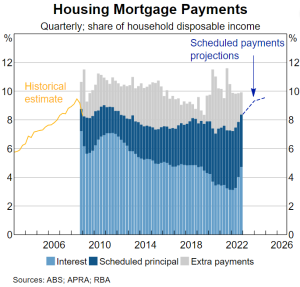

The interest rate sensitivity of households appears to be playing out in the housing market where house prices have fallen by 8.9% since their peak, and in credit growth, but to date there has been little impact on household consumption with trends similar to the strength seen offshore. One reason could be the financial buffers accumulated during the pandemic, delays in interest rate pass through to mortgaged households, or just the level of rates is not restrictive enough.

Chart 1: Australia’s cash rate well behind the US, how far below will it peak?

Chart 2: Australian nominal GDP well out in front

Chart 3: Australian real GDP also well out in front

Chart 4: Australian core inflation is high

Chart 5: Australian mortgage repayments set to rise, but still unclear the wider impact. Although interest repayments have risen, total repayments have been steady over the past few quarters as households reduced excess principal repayments in aggregate