Total spending grew 0.9% in June.

The key policy challenge will be to gradually return inflation to the 2%/2-3% target ranges sought in the US and Australia respectively, while avoiding taking interest rates too high producing a recession and a sustained rise in unemployment

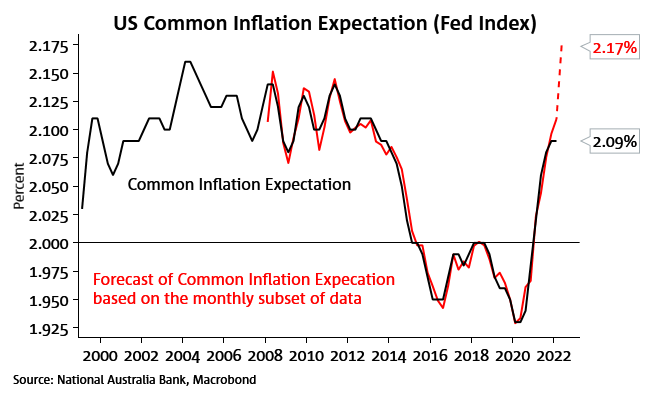

Chart 1: Inflation expectations continue to lift

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.