Analysis: Inflation indicators run hot, central banks will tilt to being more hawkish

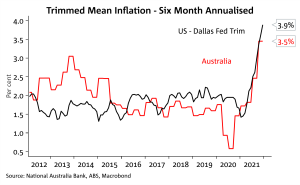

CPI figures last week illustrated Australia is not an island when it comes to global inflation pressures with core trimmed mean inflation running at 2.6% y/y. The six-month annualised rate is running hotter at 3.5% and is not far off the US where the Dallas Fed Trimmed Mean PCE inflation rate is at 3.9% six-month annualised.

In this Weekly we look at Central Bank frameworks and how policy may evolve under the newly adopted average inflation targeting/maximum employment frameworks. This is important given central bank reaction functions prior to the pandemic would imply much tighter policy. E.g. for the US the Cleveland Fed’s Policy Rules imply a Fed Funds Rates already at 2.70% and lifting to 3.3% by end 2022!

Once policymakers see maximum employment as broadly met and are confident rates can sustainably move away from zero without inflation moving below target, policy is likely to become more proactive again in responding to at or above target inflation.

To delve into this, we observe how the US Fed thought policy would evolve under the average inflation target/maximum employment framework when it was first adopted in 2020. We then look at US Fed Chair Powell’s post-FOMC press conference to see whether the initial guidance is likely to eventuate. Finally, we draw parallels with the RBA, as well as looking at the last rate hike cycle in 2009. Our key findings are:

Central banks are likely to revert to previous reaction functions: Former Fed Chair Clarida, an architect of the Fed’s average inflation targeting framework noted in early 2021 that after liftoff from zero, monetary policy reverts to simple flexible inflation targeting and he would use an inertial Taylor Rule to help inform where policy should be. Such a rule has policy around 1.00% at the end of 2021 and 2.50% by end 2022.

Focus tilts to inflation, with less emphasis on maximum employment: Clarida also noted when maximum employment is broadly reached, it will be data on inflation that the Fed reacts to. Chair Powell in his press conference seemingly confirmed this approach, noting “I think there’s quite a bit of room to raise interest rates without threatening the labor market”.

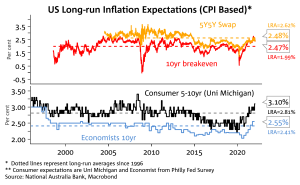

Inflation expectations are potentially important for the pace of lift-off: Inflation expectations are the ultimate arbiter of whether temporary higher inflation is likely to persist for longer. On the measures we look at, US inflation expectations are back to pre-GFC averages.

Policy is asymmetric: The lower bound on policy limits how low rates can go to push inflation higher, but not how restrictive they can become to control inflation on the upside.

RBA could assess policy is “imprudent” very quickly and hike swiftly to materially shift the stance of policy to a less accommodative setting: Looking at the 2009 hiking cycle, the RBA hiked by 25bps at three consecutive meetings after it assessed changes to the outlook meant the policy stance had become “imprudent”.

Chart 1: Australia is not an island as far as inflation is concerned. The the core trimmed mean measure inflation is running at similar rates to the US

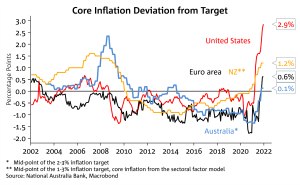

Chart 2: Core inflation is above target across the G10, meaning central banks will pivot hawkish. The question is how hawkish will they need to become.

Chart 3: Inflation expectations are now above average and back to pre-GFC levels, suggesting policy needs to be materially less accommodative