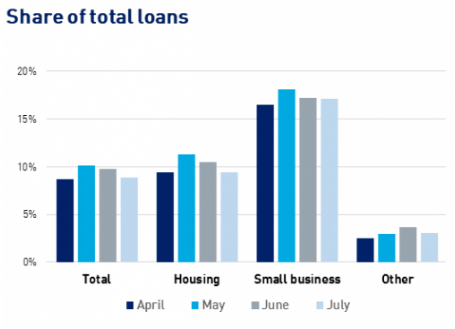

APRA recently released details on the major banks’ home loan deferral scheme. At its peak use in May 11% of all home loans were being deferred. That figure has now fallen back to 9% with some of those customers also restarting repayments. That is an encouraging sign and aligns with the recovery seen in payrolls data with around 50% of the jobs lost in the initial phase of the pandemic having been regained.

Overall, house prices have been surprisingly resilient with only mild declines seen so far and prices have actually risen in Brisbane, Perth and Adelaide over the past month. Part of the reason is likely due to the loan deferral scheme preventing forced sales (the first phase of the scheme ends on September 30 with an extension to March 31 2021 on a case by case basis), while interest rate cuts and government support packages and access to super have increased household cash flows.

NAB is still pencilling in house price declines of 10-15% over the coming 12-18 months with Australia’s recovery from the pandemic expected to be protracted. GDP is not expected to return to pre-pandemic levels until mid-2023, while unemployment is expected to peak at 10% (currently 7.5%). Notwithstanding, home loan deferrals and extensive fiscal support may continue to see resiliency continue for house prices until later in 2020, when these supports begin to be rolled back.

RBA easing speculation grows, 7 of 11 economists expect an expanded QE program

The RBA Minutes are set to be watched closely tomorrow after an AFR article today suggested the RBA is contemplating further easing, including an expanded QE program and possibly lowering the cash rate to 10bps from its current 25bps.

Speculation has been mounting since the September Board Meeting which saw the TFF expanded and an easing bias inserted into the concluding para (“continues to consider how further monetary measures could support the recovery”). A recent Bloomberg survey suggests 7 out of 11 economists are expecting an expanded QE program.

Week ahead

Australia: The RBA Minutes are on Tuesday and will be closely watched to see whether the RBA is indeed contemplating further policy easing (see above). Key employment data on Thursday should show Victoria’s lockdown weighing. Weekly payrolls suggest a -40k outcome (also the consensus) and unemployment rate is expected to rise to 7.8%.

International: Across the ditch NZ has Q2 GDP figures on Thursday and the pre-election fiscal update is on Wednesday. CH: most focus on the key activity indicators on Tuesday where retail continues to lag the industrial recovery. EZ/UK: BoE meets Thursday and while policy is unchanged, could lay some groundwork for further easing. UK-EU trade negotiators also re-convene amid a the current Brexit vacuum. US: The FOMC meets with Powell likely to be pushed on what exactly average inflation targeting means.

Please see attached for further details.

Charts of the week

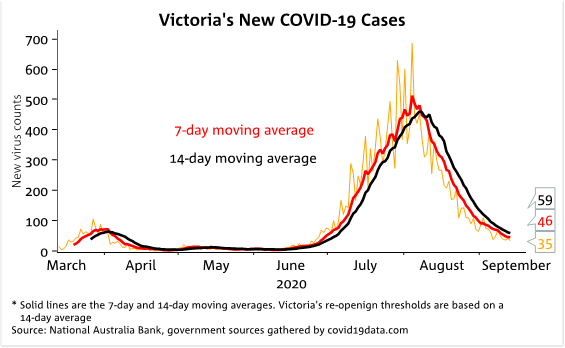

Victorian virus numbers continue to fall.

Housing loan deferrals have fallen

Source: APRA

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.