Online retail sales growth slowed in May following a fairly strong April

Insight

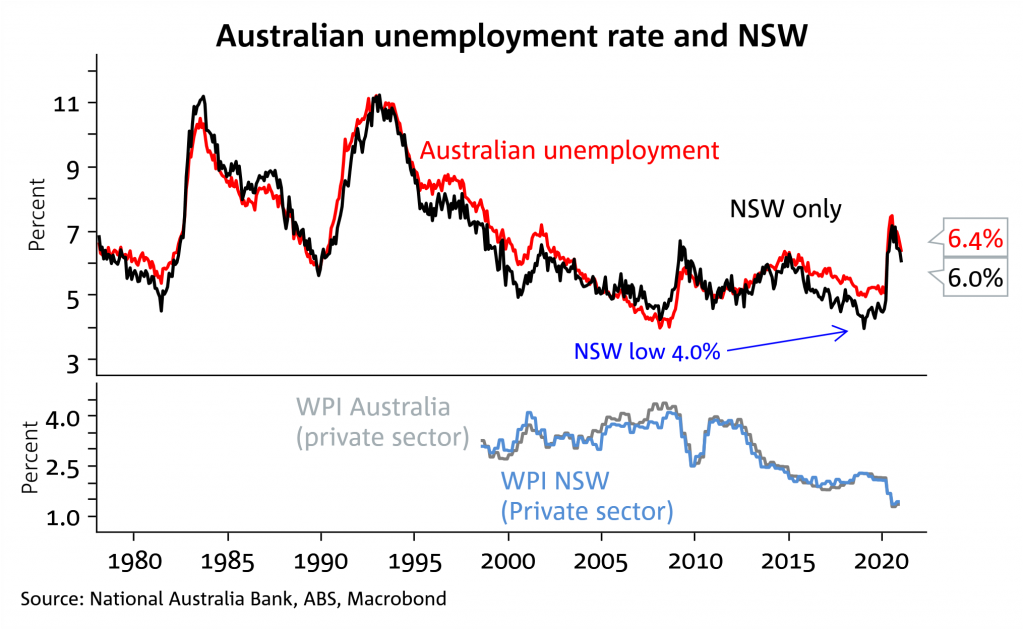

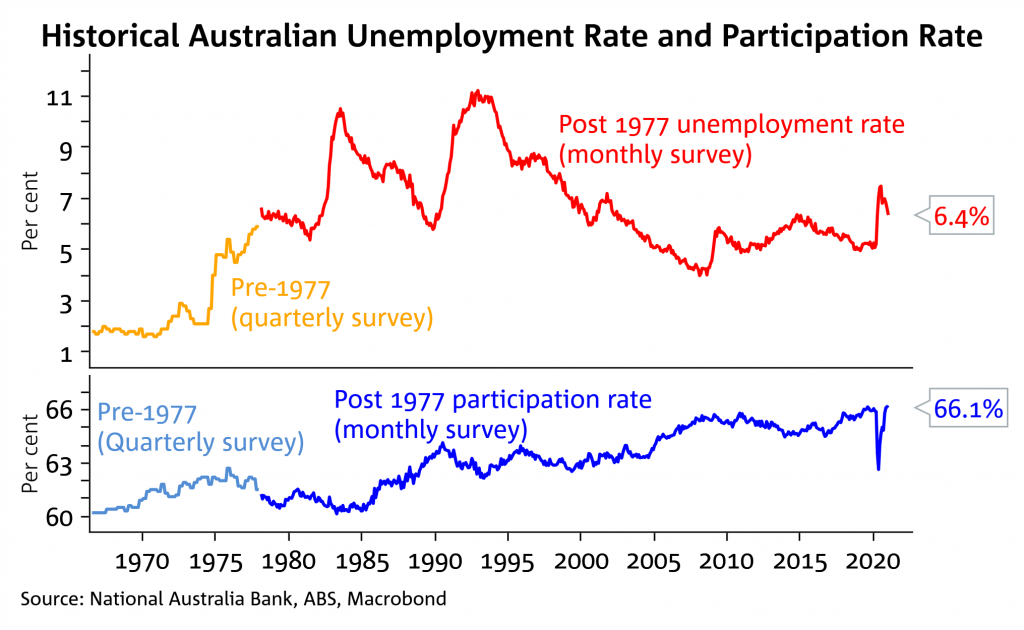

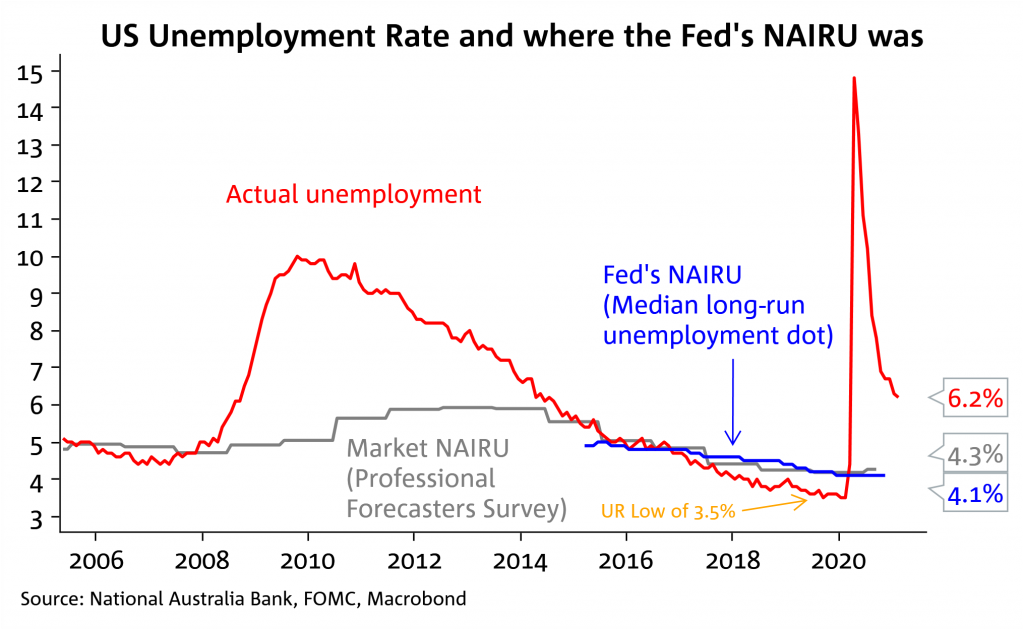

Central banks are pursuing ‘maximum possible sustainable employment’, an understated evolution in inflation targeting.

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.