NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

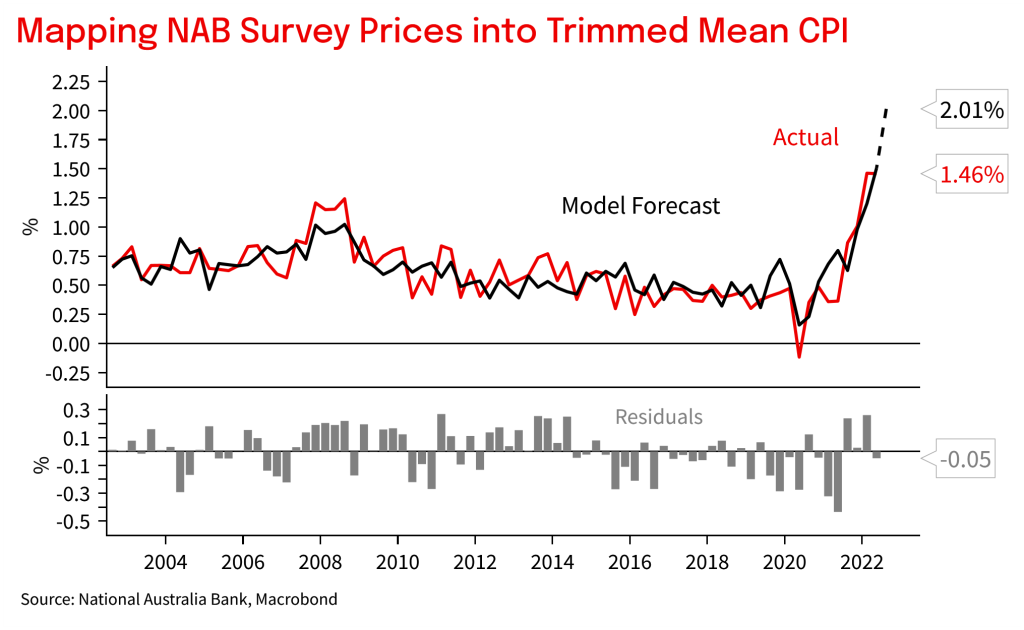

This week we update our analysis of the inflation reads in the NAB Business Survey and what this may mean for CPI pressures in Australia, particularly in Q3.

Chart 1: NAB survey implies a hot Q3 CPI

NAB Markets Research Disclaimer

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

RBA surprises with a hold, NAB still sees cuts in August, November and now February

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.