AMW: Preliminary Q3 CPI thoughts and the inflation outlook

In this weekly we give our initial thoughts on Q3 CPI following last week’s August monthly CPI indicator. We will provide a full preview early next week ahead of Q3 CPI on 26 October.

Analysis: Preliminary Q3 CPI thoughts and the inflation outlook

In this weekly we give our initial thoughts on Q3 CPI following last week’s August monthly CPI indicator. We will provide a full preview early next week ahead of Q3 CPI on 26 October. Our preliminary thoughts are a headline print of 1.3% q/q and 6.7% y/y. For the RBA’s closely-watched core trimmed mean print we see 1.6% q/q and 5.7% y/y. That is broadly consistent with prices data within the NAB Business Survey.

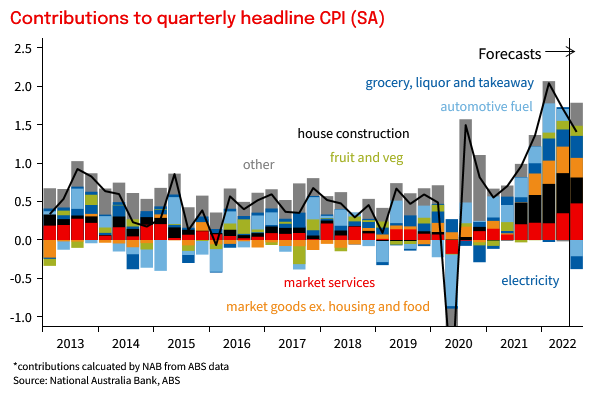

A key uncertainty for the trimmed mean is whether new dwelling construction costs are again high enough to be trimmed out – according to the monthly CPI indicator we think they will be and we see constructions costs being 3.5% q/q from 5.6% last quarter with a more meaningful moderation likely in Q4 – but if they slow more sharply trimmed mean could print around ¼ point lower than our forecast due to the influence on the distribution of prices (as well as adding less to headline).

Outside of new dwelling costs, a key driver this quarter is likely to be the first fall in fuel prices after eight consecutive quarters of increase. On the goods side, there is no sign of a broader slowdown yet according to the monthly CPI indicator. Rent inflation is also expected to accelerate to 1.0% q/q from 0.7% q/q, its fastest pace since 2013. Market services inflation which includes rents should rise by 1.7% q/q.

As for the near-term inflation outlook, NAB expects inflation to peak in Q4 2022 at around 7½% before moderating convincingly over 2023 as the special factors driving the goods and construction led inflation surge fading. Over the past nine months there has been a clear pull-back in shipping costs (freight from China to West Coast USA is back to 2018 levels), supply backlogs are being worked through, while some indicators point to an emerging slowdown in global goods demand.

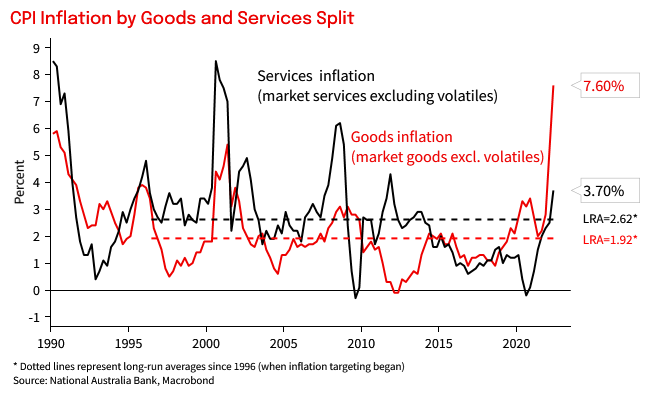

Of more importance for the longer-term inflation outlook, service inflation is picking up, and may prove a more durable source of inflation pressure. Some easing of goods and housing drivers are thus unlikely to be sufficient for the RBA in the context of the strong demand backdrop and tight labour markets. While the composition of inflation may shift it will be the strength of the nominal demand backdrop that ultimately underpins where overall inflation may fall back to over the next couple of years.

For the RBA, Q3 inflation along the lines of our preliminary forecasts would be broadly in line with those contained in the August SoMP, and thus still reflect too‑strong inflationary pressure. Having slowed the pace of hikes at yesterday’s meeting it is clear the era of front-loading is now over with the RBA more data and outlook focused.

Further evidence of moderating goods and construction inflation will take some of the pressure of the RBA to respond aggressively to headline inflation prints, but with forecasts for inflation to only fall back to the top of the 2-3% band by the end of 2024, upward surprises would likely push the RBA to further into restrictive territory. NAB sees the RBA cash rate getting to 3.10% with upside risks given the inflation outlook.

Chart 1: Home construction and goods have led the increase so far, but market services inflation is quickening

Chart 2: Services inflation will be an important driver of the inflation outlook as the exceptional drivers’ goods and construction inflation fade