AMW: RBA Review – is it matching expectations so far?

The RBA Review is underway and the three panel members recently publicly discussed their approach. In this Weekly we summarise these discussions and what changes the RBA panel is likely to recommend.

Analysis: RBA Review – is it matching expectations so far?

The RBA Review is underway and the three panel members (Professor Wilkins, Professor Fry-McKibbin, and Dr de Brower) recently publicly discussed their approach to the Review and the themes that have emerged from these consultations ahead of the Panel’s report to the Government in March 2023. In this Weekly we summarise these discussions and what changes the panel is likely to recommend.

Importantly for markets, there seems to be broad support for the flexible 2-3% inflation target which is currently formalised in the Statement on the Conduct of Monetary Policy between the Treasurer and the RBA Governor (“goal is to keep consumer price inflation between 2 and 3 per cent, on average, over time”). We do not think the review panel will recommend changes to this target, though it may be clarified.

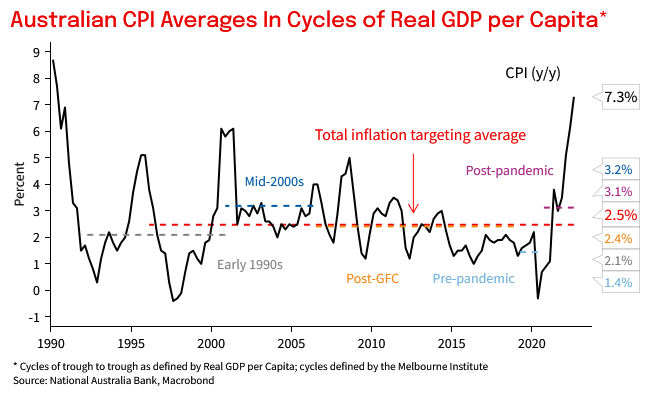

Indeed, Australian headline inflation has averaged 2.48% since the inflation target was formally adopted in 1996 (see Chart of the week below). Even using alternative averages such as business cycles as dated by the Melbourne Institute, inflation has mostly averaged between 2-3%, except for the mid-2000s cycle which was overstated due to the impact of the GST. Note the current post-pandemic cycle average is 3.1%.

However, there were concerns in submissions around how monetary policy will respond to future shocks. In this context there was some discussion about clarifying what inflation at 2-3% “on average, over time” meant. There was also discussion of the interplay of the inflation target against its broad objectives of financial stability, and the RBA Act’s defined responsibilities of maintenance of full employment.

There was some discussion around policy at the zero lower bound, and the relative merits of formal price level targeting (albeit an average inflation target can be similar to a de-facto price level target), and nominal GDP targeting (your scribe notes Australia’s volatile terms of trade and large revisions to historical GDP makes nominal GDP targeting far from ideal).

Given the 2-3% inflation target looks to be broadly agreed upon, most recommendations from the review panel are likely to focus on communication, governance, and culture. On communication, there was a lot of discussion on whether the RBA’s communications were “as clear and fulsome” as possible. This was particularly centred around the RBA’s experience of unconventional policies, where full risk analysis, clear exit strategies and triggers of review where not formalised. There was also some discussion around formalising RBA-APRA communications.

On governance, there was discussion whether there should be a separate Monetary Policy Committee to the current RBA Board. A change here would require a change to the RBA Act for which there appears to be a high bar. Board appointments are at the discretion of the Treasurer, so changes in composition can be implemented relatively quickly. There was also talk of Board members getting staff resources. The review panel also noted it may present two sets of proposals – one set that doesn’t require any changes to the RBA Act, and one set that would amend the Act.

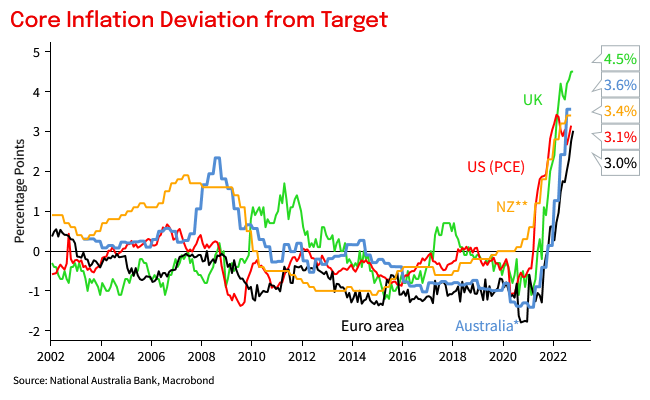

Chart 1: Review is being conducted in an era of high inflation

Chart 2: Australian inflation has averaged 2.5% since 1996