Coming in for landing in a heavy cross wind

Insight

The RBA Review is underway and the three panel members recently publicly discussed their approach. In this Weekly we summarise these discussions and what changes the RBA panel is likely to recommend.

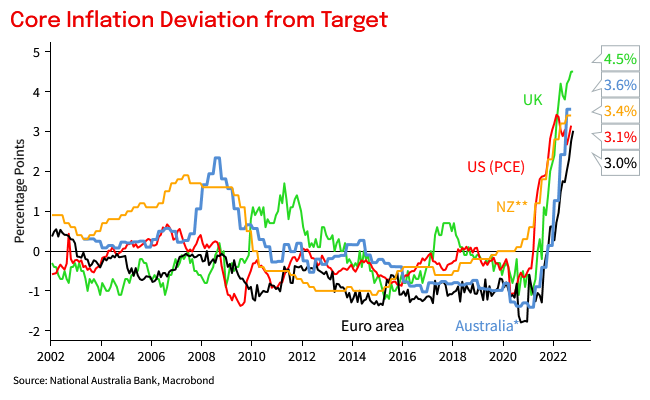

Chart 1: Review is being conducted in an era of high inflation

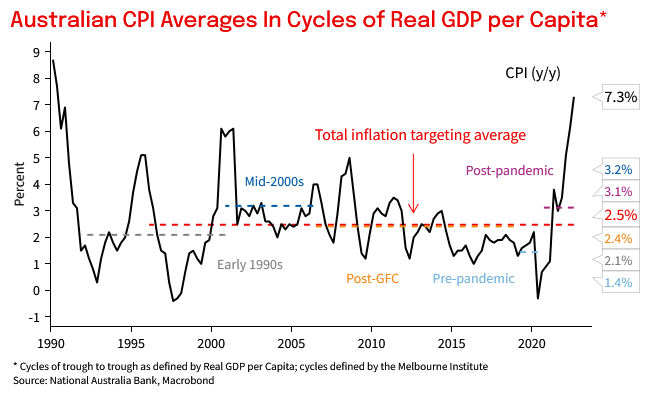

Chart 2: Australian inflation has averaged 2.5% since 1996

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.