AMW: RBA: the top ten reasons we expect today’s interest rate increase to be 25bps

The RBA’s Board meets today and a further interest rate increase is unanimously expected by market economists with the size of the rate increase uncertain.

Analysis: RBA: the top ten reasons we expect today’s interest rate increase to be 25bps

The RBA’s Board meets today. Unlike May, when there was some debate as to whether the Board would move interest rates at the Meeting, a further interest rate increase is unanimously expected by market economists. Today, it’s the size of the rate increase that is uncertain. In today’s weekly, we outline the top ten reasons why we expect the RBA to deliver another 25bps rate increase tomorrow, as well as outlining the arguments in favour of faster moves.

The RBA has not tightened by more than 25bps since 2000 (it has eased by larger amounts).

The RBA considered tightening by 40bps last month, but chose to tighten only by 25bps, signalling a return to normal operating conditions after the pandemic, when rate rises are 25bps in quantum.

The RBA Board meets monthly (eleven times a year), whereas other central banks meet six-weekly/eight times a year. This allows the RBA to move rates more frequently at smaller increments.

The Bank continues to see Australian developments as being different to other countries such as the US.

The Bank still wishes to see Australian wages accelerate so that inflation is sustainably at target once pandemic and war shock effects wear off.

There are considerable temporary and one-off inflation shocks in the system at the present time related to COVID and Russia’s invasion of Ukraine.

Australia runs a flexible inflation targeting regime and therefore does not have to quickly return inflation to target.

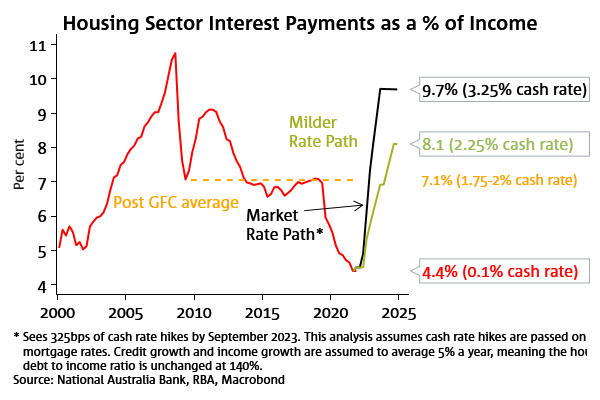

Australia’s interest rate structure is predominantly floating rate, rather than fixed rate. Combined with the high level of household debt, this makes changes in Australian official interest rates extremely effective and naturally inclines the RBA to a degree of caution in moving interest rates higher.

The data released during May support a further tightening of interest rates, but do not appear to provide additional support for a shift to a larger tightening increment relative to the RBA’s May expectations.