Coming in for landing in a heavy cross wind

Insight

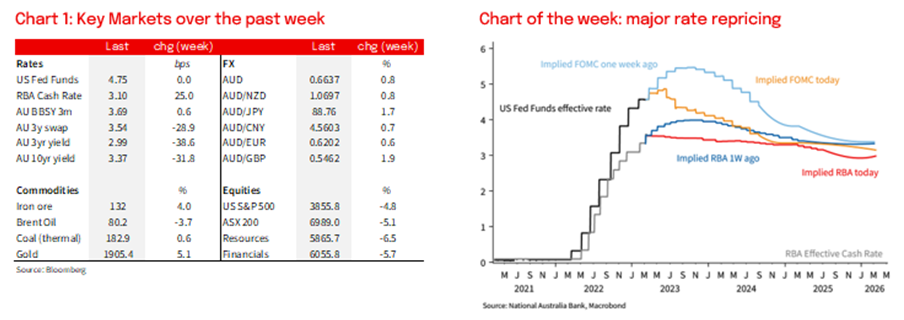

This week, we consider the likelihood of further tightening by the RBA and what impact - if any - the recent failure of Silicon Valley Bank might have.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.