We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Overall clients on the Sunshine Coast and Noosa continue to report strong conditions and very tight labour markets. While only a microcosm, the themes from these clients are broadly reflective of what we are picking up in the NAB Business Survey, and it is clear the RBA is not yet in sufficiently restrictive territory to slow demand enough to be confident that inflation will return to the 2-3% target

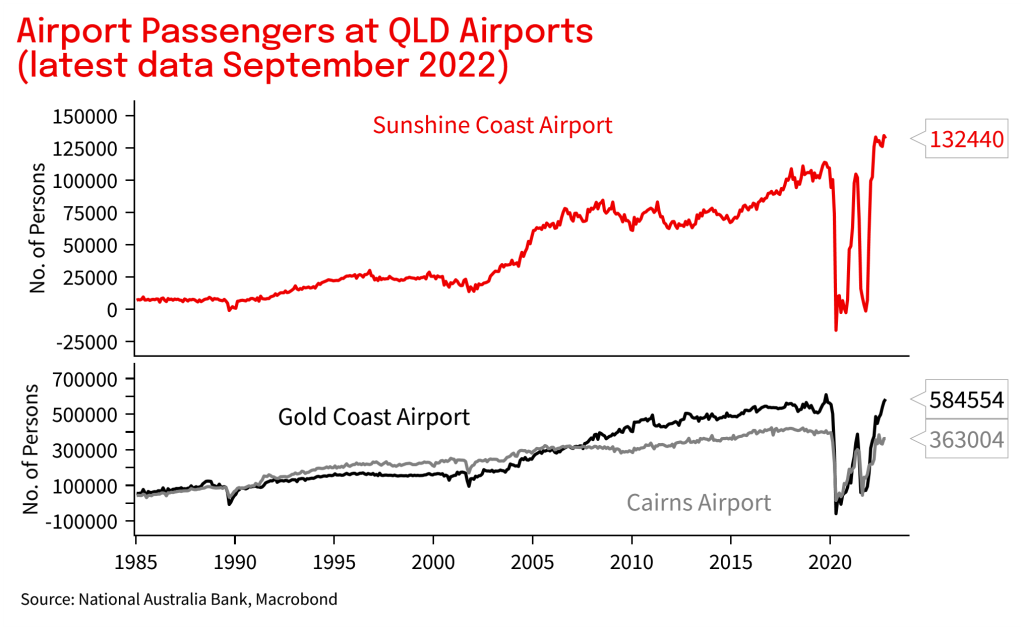

Chart 1: Travel has rebounded sharply on the Sunshine Coast

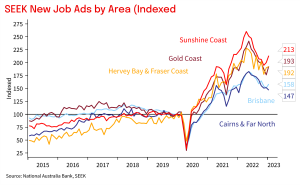

Chart 2: Labour market remains very tight with job ads still over double pre-pandemic levels on the Sunshine Coast

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.