Online retail sales growth slowed in May following a fairly strong April

Insight

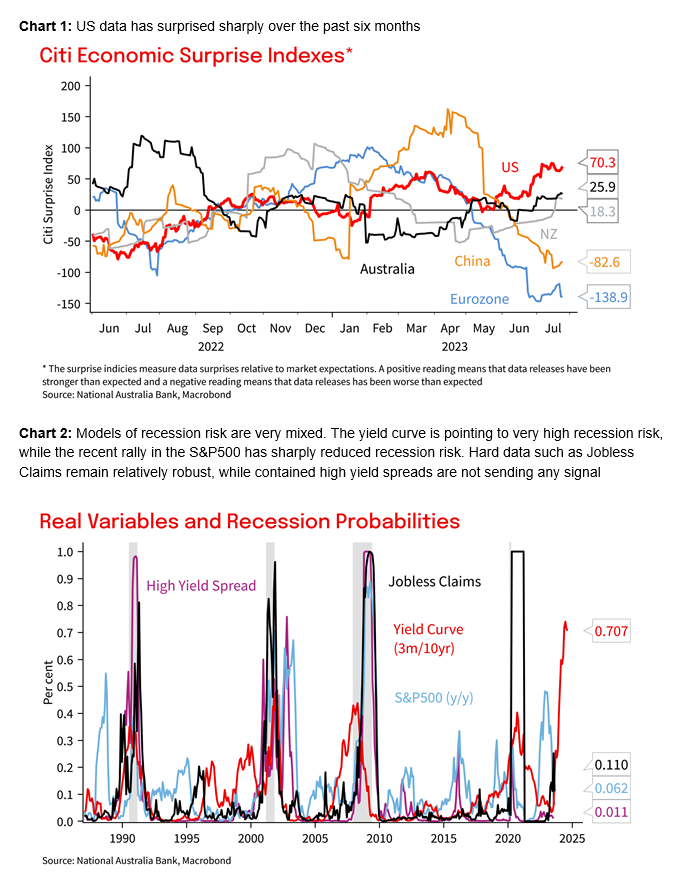

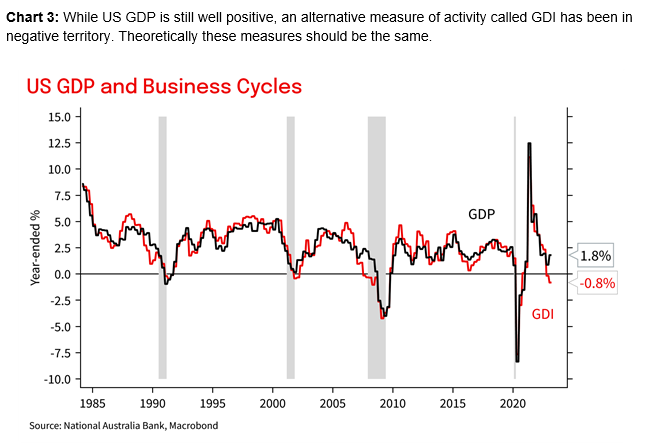

Calling a US recession has been a bit like “Waiting for Godot”, the title of the 1953 play by Samuel Beckett.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.