Online retail sales growth slowed in May following a fairly strong April

Insight

Central bank officials from around the world met at Jackson Hole last week. In this Weekly we highlight the key discussion points and what implications this may have.

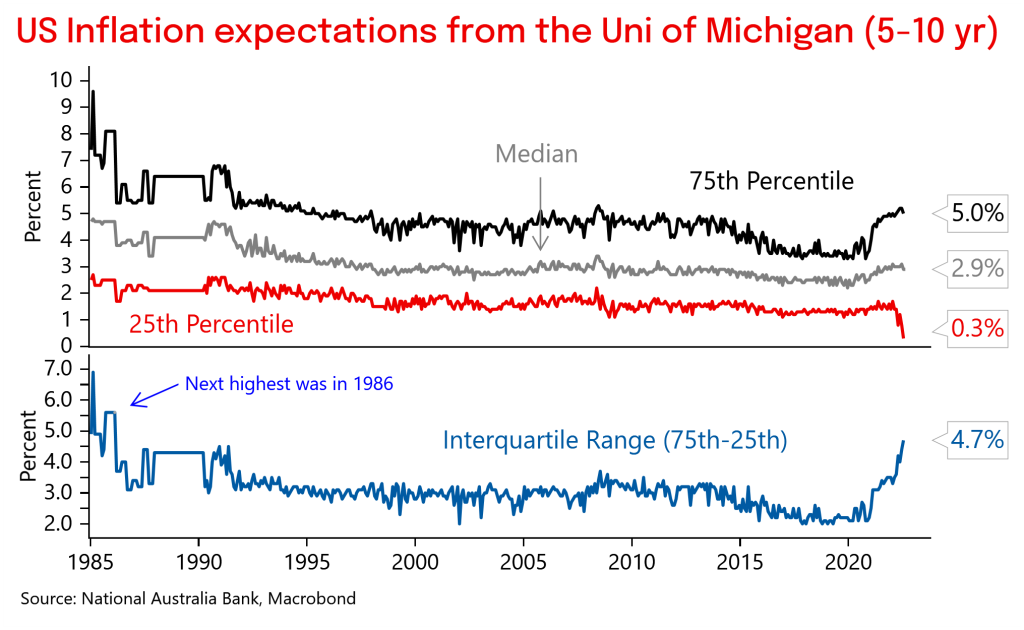

Chart 1: Inflation uncertainty is the highest since 1986

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.