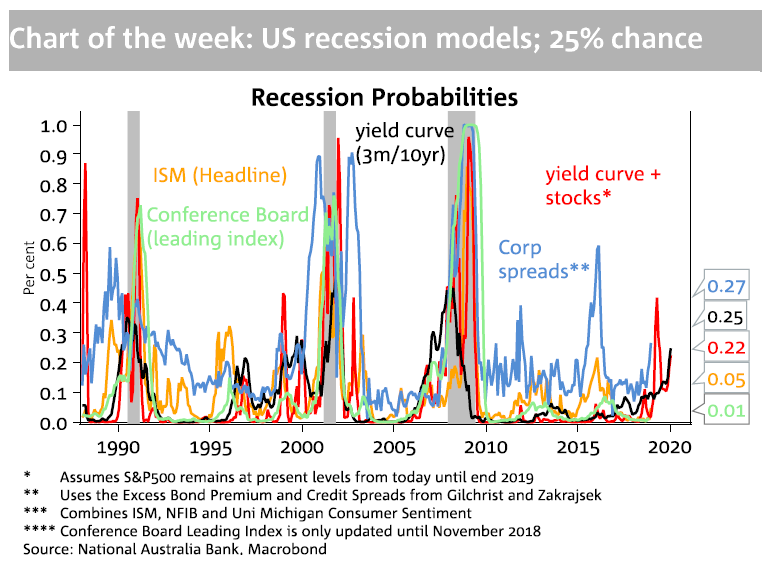

We’ve examined a number of indicators that have tended to signal the prospects of US recession. The shape of the yield curve (the difference between the yields of shorter and longer-dated bonds) has been a very reliable indicator, with inversions in the curve tending to occur some 9-18 months ahead of recession.

Our analysis suggests the 90-day/10 year Treasury bond curve historically has been the best performing of a number of different yield curve indicators in signaling US recession. This curve has not inverted, but has flattened significantly in recent times.

Further, we have statistically converted the message of the yield curve, into implied probabilities of recession, based on historical outcomes. The statistical conclusion is that markets are currently flashing an amber warning signal of US recession, with yield curve shapes currently suggesting around a 15-25% chance of US recession occurring over the next 10-18 months. While this is a relatively higher chance than has been the case at any time since the GFC, market implied pricing/yield curve inversion is not yet at the 40-60% critical levels whereby US recession tends to follow.

Now of course correlation is not the same as causation, so it’s also important to try to understand why implied recession probabilities are currently elevated or in other words, why yield curves are currently so flat.

We see three inter-related fundamental drivers: (i) rising US short-term interest rates (the curve flattens during tightening cycles); (ii) growth slowdowns in Europe and China; and (iii) US-China trade war effects/concerns. With the Fed now signalling that it can be more cautious on further US interest rate increases and with the US and China working on some trade agreement, the “influence” from two of these three factors should reduce in coming months.

We will need to remain alert to signs of further slowing in China and Europe – these are now both very large economies, capable of significantly influencing US and global growth. In a quiet Australian week (with only Housing Finance to be released on Thursday; Mkt. and NAB -1.5% m/m after +2.2% in Oct.), we’ll be watching China Trade figures (today), together with any guidance on Chinese/European growth coming from US earnings season, which kicks off today. For now, our conclusion is that market pricing is not high enough to suggest a near-term US recession.

In terms of markets, the relief rally in equity and commodity markets continues on the back of more positive sentiment towards trade negotiations and the Fed signalling its preparedness to remain patient on further US rate rises. The $A has benefited as a result, but also from a strengthening in the CNY (remember there has been a strong correlation between the $A and Asian currencies and markets in recent months). Yields however, were a little lower over the week as European data disappointed at the end of last week.

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.