Online retail sales growth slowed in May following a fairly strong April

Insight

A bumper year of corporate issuance in Australia and the re-emergence of value in offshore markets leaves Australian issuers with great funding choices heading into 2022.

Ahead of the COVID crisis Australia had already seen a metamorphic change in the domestic market during the second half of 2019.

With expansive monetary policy and an increasing breadth of investors we witnessed an expansion in appetite for risk and duration, two aspects which were previously the default concerns for issuers looking at the market. Suddenly the trade du jour was a BBB band credit in 10-years.

2020 and the onset of the pandemic did give rise to concerns around how permanent this change would be. With market dislocation shuttering the primary markets for several months domestically we saw larger issuers head offshore and smaller issuers lean more on banks. However, the reopening after the Woolworths transaction in May proved the concerns to be ill-founded.

We continue to see an investor base which has extended its duration focus, with seven-years the new five-year, and cemented the BBB ratings band as a core part of the market.

The parallels between our domestic market growth and that of the Euro market post the Greek debt crisis are eerie, which gives us a template when considering what the market is capable of delivering in the future.

Comparing the types of orderbook statistics that reflect the health of the market, the average transaction done by NAB in the 2019-2021 period is in line with the best 2015 transaction in terms of book size, diversity of investors and offshore participation.

The local investor base has demonstrated more flexibility, akin to larger global markets, around pricing moves, terms and conditions and timelines.

That said we need to be mindful that we are a smaller a market here in Australia. We have seen resistance to deal flow from investors during peak issuance – September 2020 springs to mind – where the supply side has overworked the investor. As such, issuers need to be cognisant of the total supply pipeline in the AMTN market, not just comparable credits.

The good news though is that issuers have a plethora of alternatives in accessing long-term debt capital.

This domestic market growth we’ve witnessed has been occurring alongside a pre-GFC style expansion of risk in global markets fuelled by low rates and aggressive central bank buying of credit assets in the two largest markets, the US and Europe. We are now seeing corporate sub-investment grade USD issuance outstripping A band issuance or above by a ratio of circa 2:1 (see USD Dealogic chart below).

Under current conditions the transactional optionality rests with issuers, not investors. The reason we are seeing the basis elevate to high levels is actually testament to how open traders believe that the major banks are capable of printing significant trades in offshore markets.

Now this isn’t to say there aren’t risks.

With spreads in the bottom quartile despite the economic backdrop and a showdown between trading rooms and central banks on interest rates, it is clear that there is a sizeable risk to the cost of debt increasing in the coming 12 months.

However the base from which those potential risks will manifest should give issuers of all ratings, sectors and tenor preferences comfort that there will remain scope to access capital efficiently and with minimal execution risk.

The impact of COVID-19 in some ways serves as the template for that. We saw significant dislocation to market pricing, volatility peaking above the GFC and fund outflow some three times the GFC period. Despite that, there was a torrent of issuance, with investors willing to engage on primary issues and bid circa 1 trillion into order books in a single week1.

So I believe that while issuers need to be aware of pricing risk in the near term, the risk of being unable to access capital is incredibly low given the auspicious credit backdrop we have in right now.

USD corporate issuance by rating

Source: Dealogic

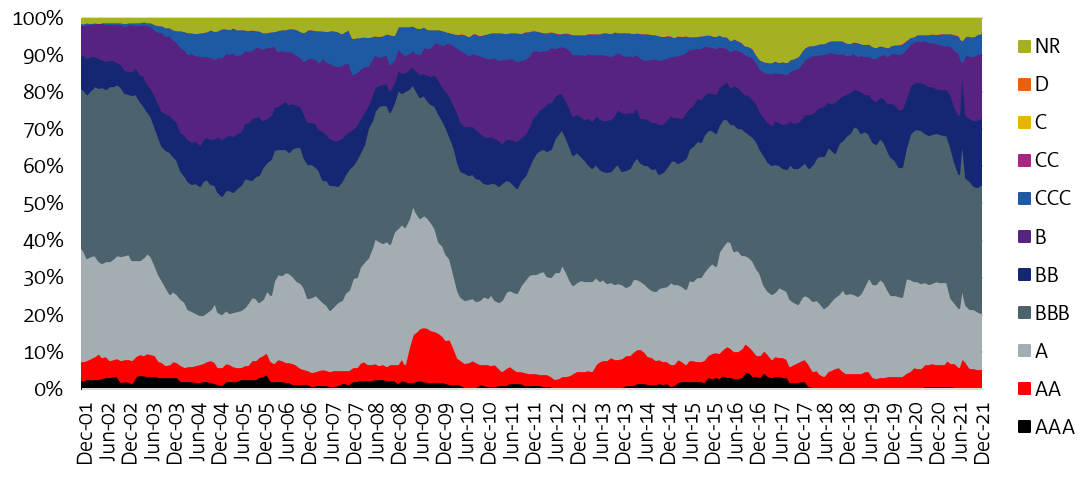

AUD corporate issuance by rating

Source: NAB data

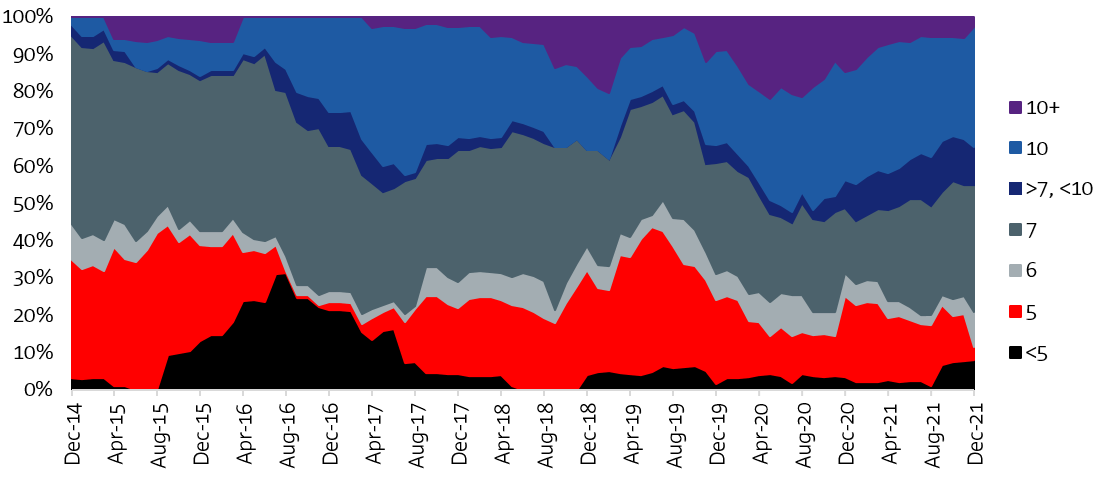

AUD corporate issuance by tenor

Source: NAB data

By Brad Peel, NAB Director Corporate Origination

____________

1 IGM

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.