Total consumer spending grew 0.7% in July

Insight

Australia needs more housing than ever, but feasibility challenges continue to hamper reliable apartment supply. NAB’s Head of Property Development Finance, Jason MacKenzie explores some options.

In a tight rental market and with migration set to continue, Victoria and Australia face a real housing supply issue. In Victoria, the government’s Housing Statement (announced September 2023), aims to deliver 80,000 new homes each year throughout 2024 to 2034. A material proportion of these are proposed to be apartments.

Charter Keck Cramer’s recent State of the Apartment Market presentation estimates the current demand for Build to Sell (BTS) and Build to Rent (BTR) or Multi-Family apartments in Melbourne is in the range of 15,000 to 18,000 new apartments each year, with current supply nowhere near these levels. BTR is projected to provide more than 50% of the limited supply over the next four years. Right now, the majority of large-scale residential developments in Melbourne are in fact focused on BTR. Most are backed by offshore institutions and, unlike BTS, do not require any pre-sales to establish market acceptance. Financiers generally take a view on the “on completion” value and forecast cash flow to debt size BTR loans. [1]

While BTR provides additional rental supply, it generally targets premium rents based on adding amenity and providing a superior service offering. For those wanting to buy, apartments continue to be a comparatively more affordable option when compared to detached housing.

What will it take for BTS Developers to bring new projects to market?

Once a developer has purchased land, completed planning and engaged builders and other services, traditionally, feasibilities have shown about a 20% profit on cost. Some would argue this is a healthy return, but there are many potential risks throughout the process which can take many years and expose developers to cost escalation.

In today’s market, compounding factors have entirely rocked feasibilities to stall the ongoing, reliable supply of apartments, despite the well-publicised need.

Construction costs rose dramatically during COVID and significant pressure on builders saw many projects and businesses fail.

Today, while costs appear to have settled into a more predictable level, they won’t be retracing to pre-COVID levels, so cost pressures remain elevated.

Lack of subcontractors is also an issue with many trades opting to work on more lucrative and income-certain sites.

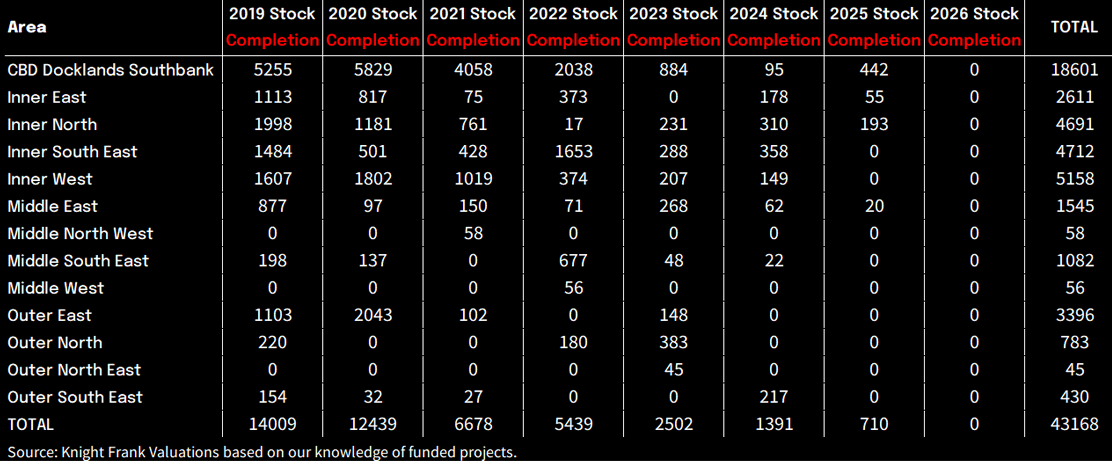

For developers, a key problem is land prices have not materially reduced and revenue has not materially increased, putting most feasibilities under water. The following supply chart from Knight Frank demonstrates how the forecast looks today: since 2019, stock completion has fallen from thousands to hundreds to zero in multiple areas of Melbourne.

Pre-COVID, where development plans were well advanced, builder quotes were also relatively stable, providing developers a reasonable platform to set prices and sell apartments at market rates. Today, this reliability no longer exists, with many builders only offering to hold prices for up to 90 days.

Developers today are finding it increasingly difficult to sell apartments off the plan, and to make matters worse, to justify taking the risk/reward, they need to sell at much higher prices.

Many developers simply aren’t prepared to “roll the dice” and we’ve seen numerous projects pulled after considerable sales campaigns because of feasibility pressure.

For developers to lock in building prices and get construction under way, they need to be able to take on more risk from a revenue/sales perspective. This also requires their capital partners and financiers to be comfortable with this strategy.

Leading into 2017, the “off-the-plan” market was well-established, with developers confident they could sell enough apartments to make a project viable.

Since then, the market has faced significant headwinds:

Project delays and builder failures also mean purchasers now want to physically inspect completed developments and, importantly, obtain a current valuation to eliminate the valuation risk associated with buying off-the-plan.

This, however, doesn’t help developers prove market acceptance of their product.

From a financing perspective, there is ample liquidity, with fewer projects and a growing non-bank lending sector. Banks are also continuing to review lending criteria, aiming to support clients and provide innovative finance solutions at a lower cost than non-banks.

Further government stimulus programs could help increase developer appetite for new projects. One example is the recently launched Housing Australia Future Fund which has sought applications from developers in joint ventures with Community Housing Providers to deliver affordable and social housing.

Other potential levers for different tiers of government could be:

There’s no easy solution and with the complexities involved, this will always need a multi-pronged approach. At NAB we’re here to support our clients, working together to help solve this difficult issue facing the industry and the nation.

Important Note

The information contained in this article is intended to be of a general nature only, it is not research. It has been prepared without taking into account any person’s objectives, financial situation or needs. NAB does not guarantee the accuracy or reliability of any information in this article which is stated or provided by a third party. Before acting on this information, NAB recommends that you consider whether it is appropriate for your circumstances. NAB recommends that you seek independent legal, property, financial and taxation advice before acting on any information in this article. You may be exposed to investment risk, including loss of income and principal invested.

You should consider the relevant Product Disclosure Statement (PDS), Information Memorandum (IM) or other disclosure document and Financial Services Guide (available on request) before deciding whether to acquire, or to continue to hold, any of our products.

All information in this article is intended to be accessed by the following persons ‘Wholesale Clients’ as defined by the Corporations Act. This article should not be construed as a recommendation to acquire or dispose of any investments.

Total consumer spending grew 0.7% in July

Insight

Investing and risk management in a world of shifting and unstable cross-asset correlations

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.