Firmer consumer and steady outlook

Insight

The AUD/USD in 2021 – the story so far and what lies ahead?

While not coming close to the volatility witnessed during the early stages of the Covid-19 pandemic in 2020, the AUD/USD exchange rate has nonetheless undergone quite a wild ride in the first two months of 2021 (Chart 1).

From a low of 0.7564 on February 2, AUD/USD briefly traded above 0.80 on 25 February (high of 0.8007), the first time it has been above this psychologically important level since 2 February 2018.

The most remarkable feature of trade in the AUD so far in 2021 has been the speed and magnitude of the fall-back in just 24 hours right at the end of February, from above 80 cents to below 77 cents. A graphic reminder of why the AUD has over the years earned its moniker as a currency that ‘goes up the stairs and down the elevator’.

AUD always has been – and likely will be for years to come – a ‘risk sensitive’ currency. Australia is highly integrated into the global economy and financial system, and dependent on the ‘kindness of strangers’ to fund close to one trillion dollars’ worth of external debt built up over decades.

Whenever the world goes ‘risk off’ and investors retreat to the safety of their home shores, the AUD tends to suffer, just as the US dollar tends to benefit from its safe-haven characteristics as the world’s preeminent reserve currency.

The flip-side of these periodic AUD sell-offs, is that when the world’s financial markets are in a happy place (or ‘risk on’) and optimism about the outlook for the global economy is running high, the AUD tends to do well.

This is exactly where we’ve been for most of the last ten or eleven months, with only brief interruptions, aided by an enormous amount of monetary and fiscal support.

Risk sentiment has also been supported by confidence that the pandemic is being brought under control, vaccine roll-out will proceed apace, allowing economies to fully re-open by the end of 2021 (barring international travel).

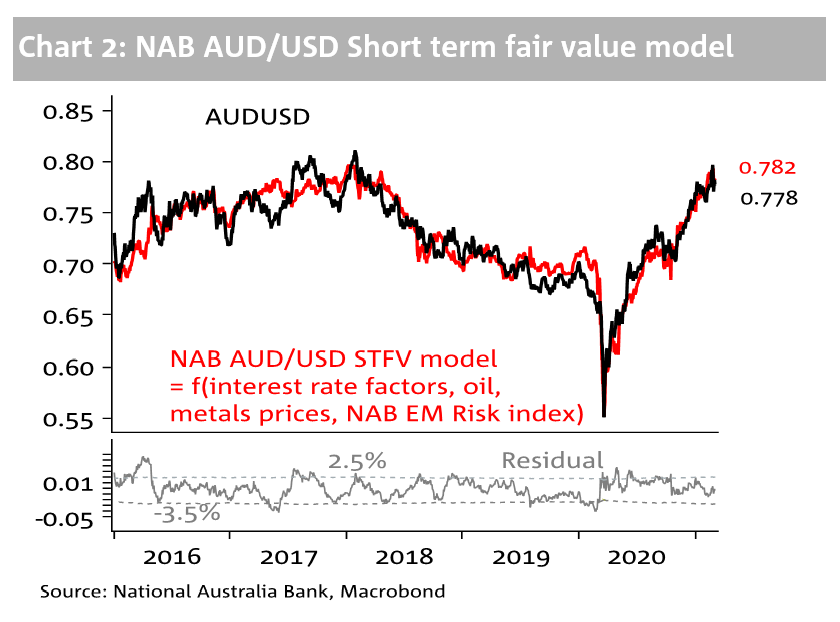

This optimism has shown up most noticeably in commodity prices, especially for oil and industrial metals. These feature prominently in NAB’s ‘fair value’ model for the AUD/USD exchange rate (Chart 2).

The combination of positive risk sentiment and higher commodity prices has meant that NAB’s fair value estimate has been steadily rising since about April last year, and AUD/USD has accordingly tracked higher after reaching a post-2002 low of 0.55 last March.

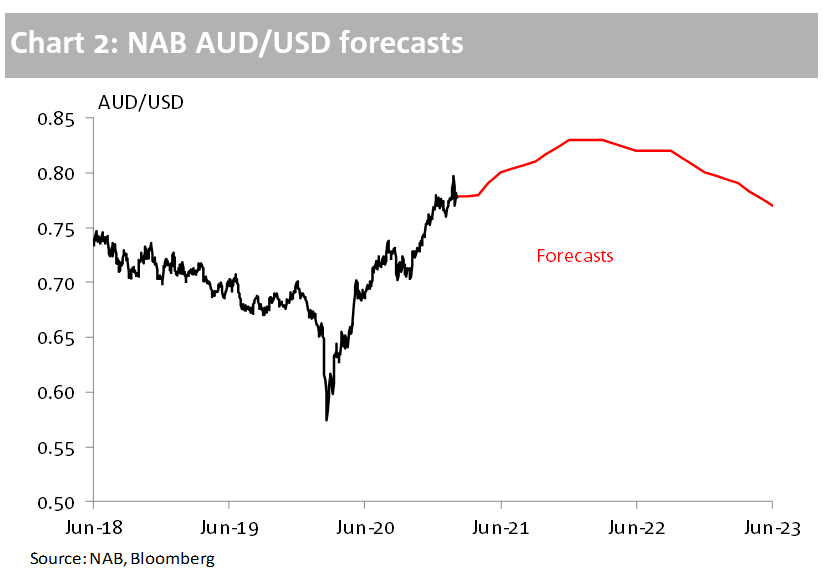

The expectation of NAB’s FX Strategy team is that providing the prevailing optimism about fuller (global) economic re-opening in H2 2021 is vindicated, then key Australian commodity export prices will remain elevated (and in some cases rise further) while risk sentiment will, by and large, remain healthy.

This is turn should mean that AUD/USD will rise further, likely in conjunction with renewed weakening in the US dollar.

In the second half of 2021, we envision AUD/USD spending most of its time within a 0.80-0.85 range.

Inevitably there are risks, either side, to our forecasts. Most notably on the downside if optimism toward global economic re-opening proves premature (in which case both risk sentiment and commodity prices well likely suffer); and to the upside should commodify prices relevant to Australia significantly extend their 2020 and early 2021 gains.

Firmer consumer and steady outlook

Insight

Having passionate young professionals on the team is proving a powerful differentiator for Ecovis director Elissa Lippiatt.

Video

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.