Online retail sales growth slowed in May following a fairly strong April

Insight

A Brexit breakdown pummels the pound – on #TheMorningCall Phil Dobbie asks @NAB’s Ray Attrill if we can expect the pound to fall further as the UK & EU draw lines in the sand.

Today’s Podcast

A transition agreement for Brexit is by no means a done-deal. The EU’s draft agreement is far from acceptable to the UK. The reaction has hit the pound, bond yields and equities – Phil Dobbie asks NAB’s Ray Attrill if the situation could worsen if Theresa May offers up no answers.

https://soundcloud.com/user-291029717/brexit-breakdown-pummels-the-pound

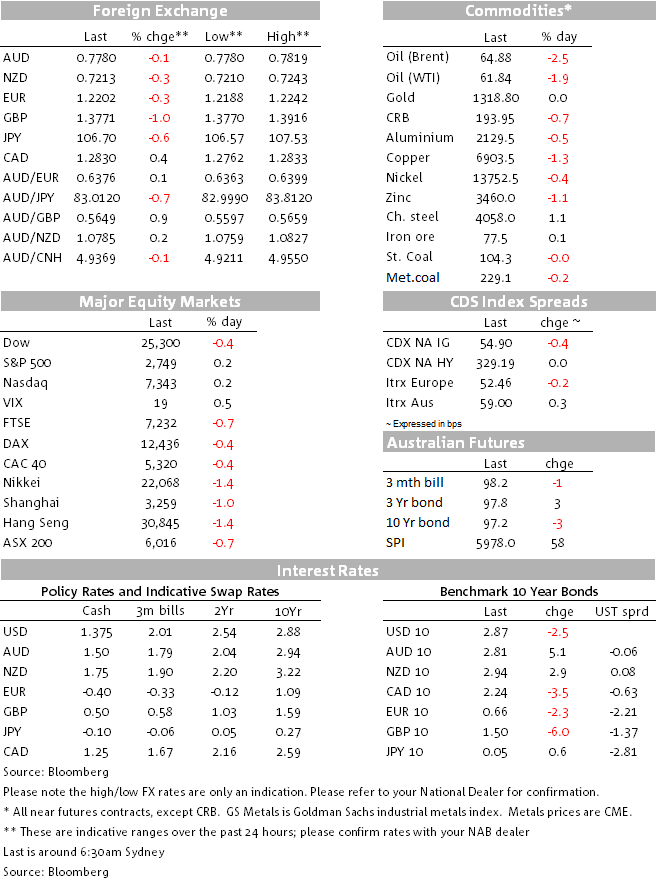

Looking across markets this morning, the standout feature on what is the last day of a fairly tumultuous month (and the first day of Autumn here – boo) the standout feature is the relatively sharp fall in all things Sterling. This following the 120 page presentation by the EU chief Brexit negotiator Michel Barnier, in which he suggests a ‘fall back’ positon whereby Northern Ireland would remain in the EU’s Customs Union post Brexit in order to avoid a hard border with the Republic of Ireland. UK PM Theresa May’s immediate response has been to condemn the proposal as complete unacceptable to the United Kingdom. Monsieur Barnier’s related suggestion that we are far from agreement to a Brexit transition arrangement has similarly alarmed UK markets (recall that the key issues to resolve here relate to the status of the Irish border, the financial ‘divorce’ settlement and the willingness of the UK to subject itself to the strictures of the European Court of Justice to settle any disputes arising during the transition period).

The clock is now ticking loudly counting us down to the March 22 EU Summit. If a transition deal can’t be agreed by then, Sterling is vulnerable to a further – and sharper – turn for the worse, bringing with it as it would the increased prospect of a ‘hard Brexit’ in March 2019. This really all just goes to show that in the last 18 months, the UK government has simply been negotiating (or as Billy Idol sang, dancing) with itself, due to the seemingly intractable differences between the hard and soft Brexiteers.

At the other end of the FX spectrum, USD/JPY is 0.6% lower, building on the rally seen during our time zone after the BoJ reduced its purchases of 25-40 year bonds – not that this means anything at all regarding prospects for the BoJ backing of its +/-0% 10-year JGB YCC policy anytime soon.

Elsewhere across markets there’s been little by way of a second wave reaction to Fed chair Jay Powell’s testimony on Tuesday (he repeats the affair in front of the Senate Banking Committee tonight). Month-end considerations are probably standing in the way of more macro-fundamental impulses just at the moment after what has been a big month for markets that sees US stocks ending with loses of about 2.7% for the S&P 500 and 3.3% for the Dow (The NASDAQ in contrast is currently down just 1.0% on the month).

US bond yields have eased back a touch in ‘bull flattening’ moves (2s -0.2bp, 10s -2.4bps to 2.87%). Despite lower yields, the US dollar looks to have been the beneficiary of month end demand (e.g. some non-US asset managers buying back US dollars in order to preserve existing hedge ratios given the fall in stocks in February). There might possibly be more of that come during today’s sessions, if so a potential small weight on AUD/USD. AUD is currently lower than where we left it last night, at 0.7771, having achieved an intra-day high near 0.7820.

In commodities, oil had a bad night with both WTI and Brent crudes off more than 2% (Brent -$1.75 to 64.78 – its lowest since mid-February). EIA data showing revised November US crude production above 10 million barrels to its highest on record (10.057m b/d) and inventory data showing a 3.02m barrels build in crude stocks is responsible for the fall. Elsewhere hard commodities are narrowly mixed while softs are all higher, led by 3.8% jump for wheat.

US data has not been market moving, with the second estimate of US Q4 GDP revised to 2.5% from 2.6 as expected. Earlier in the night, Eurozone February CPI came in at 1.2% from 1.3%, also as expected.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.