Total spending grew 0.9% in June.

US 10-year treasury yields have moved passed 3 percent, boosting the US dollar and sending the Aussie dollar careering downwards.

https://soundcloud.com/user-291029717/us-treasuries-pass-3-percent-aussie-dollar-heading-lower-start-of-a-trend

Probably the biggest market news since Australia and New Zealand broke off on Tuesday for ANZAC day is that 10 year US Treasuries now trade clean above 3% for the first time since early 2014. This has supported a further rise in the US dollar with the narrow DXY index now above 91 and so above the range in which it has been confined since mid-January (the broader Bloomberg BBDXY index having broken up out if its range earlier in the week).

US stocks have taken the latest rise in yields on the chin, though this can’t disguise the fact that the pull back in the S&P from above 2700 to below 2650 since mid-April has gone hand in hand with the break up in 10 year Treasury yields from just above 2.8% to now 3.03%. It has also come as the vast majority of incoming S&P500 earnings (and revenue) have exceeded street estimates (Ford and Twitter the latest two) but with suggestions from several household names (e.g. Caterpillar yesterday) that Q1 might have represented a near-term high water mark for revenue and EPS growth.

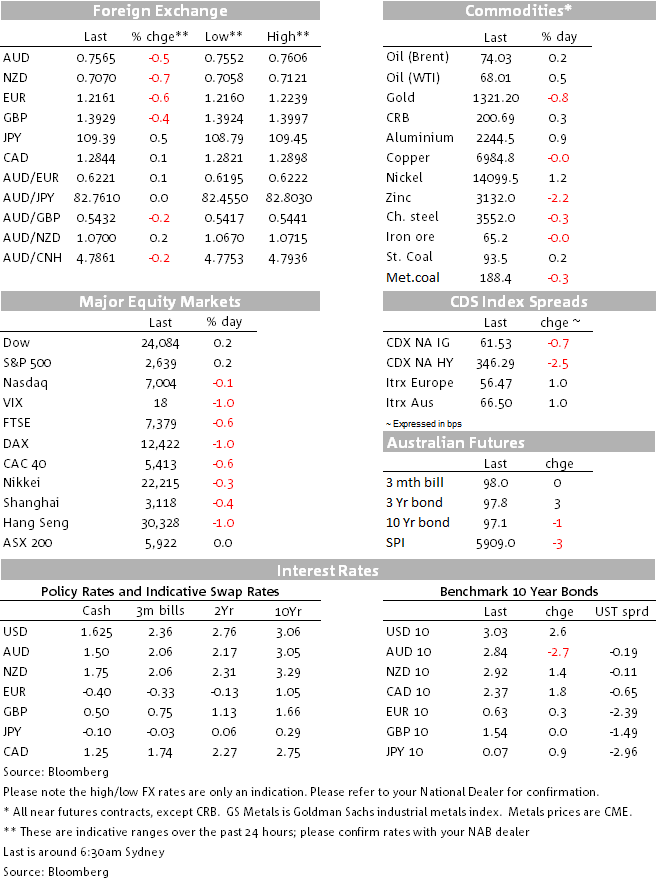

The fall in AUD/USD during this time, from above 0.78 to a new 2018 low of 0.7552 needs to be seen largely in the context of US dollar strength, though both AUD and NZD have underperformed most major currencies in the past week. This owes something to the modest decline in risk sentiment (VIX is back nearer 20 than 15) and generally if not universally, weaker commodity prices. In the case of NZD and as we have been noting, stretched speculative long positions has doubtless also had a hand, evident in AUD/NZD now trading above 1.07 from below 1.05 back on April 12th.

AUD is now within half a cent of challenging its December 2017 low of 75 cents (I was last below 0.75 in June 2017). This is as significant level that we expect to provide more formidable support than either the 0.7650 recent range lows or the 0.76 level. Current levels might provide attractive to local exporters today, who were away from the market yesterday. We’ll see.

As my BNZ colleague Nick Smythe notes today, when Us 10s were last above 3% in 2014, the Fed funds rate was 0.25%, the unemployment rate was 6.7% and the Fed’s core PCE measure of inflation was running around 1.5%. Fast forward to now, and the Fed funds rate is 1.75% and likely to be 2% by the end of June, the unemployment rate, at 4.1%, is the lowest since 2000, and core PCE is expected to be 2% when the data is released next week. Add to that the fact that the Fed is reducing, rather than increasing its holdings of US Treasuries, and the foundations for US rates above 3% are far stronger this time around than they were in early 2014.

Of some note in analysing the last 3-4 bps of the run up in Treasury yields is that have not been driven by ‘break-evens’ or the inflation expectations component of yields, which of late have gone hand in hand with the rise in oil prices that has seen Brent crude rise from $67 to $75. Crude has actually eased back in the last 24 hours, to below $74, seemingly on hopes that French President Emmanuel Macron’s pleas to President Trump not to revoke the prevailing nuclear deal with Iran will have influence (this after Trump yesterday called the deal ‘insane’). Rising real US bond yields are better for the US dollar than a largely inflation-driven rise in nominal yields.

There’s been limited economic news flow since we broke off on Tuesday, perhaps the most significant being strong US consumer confidence on Tuesday night (128.7 from 127.0 and above the 126.0 expected).

Coming Up

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.