Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

President Trump’s missile warning spooks US equity markets for a while, but @NAB’s David de Garis said it was only a mild risk-off mood.

https://soundcloud.com/user-291029717/us-missiles-and-inflation-both-are-on-the-horizon

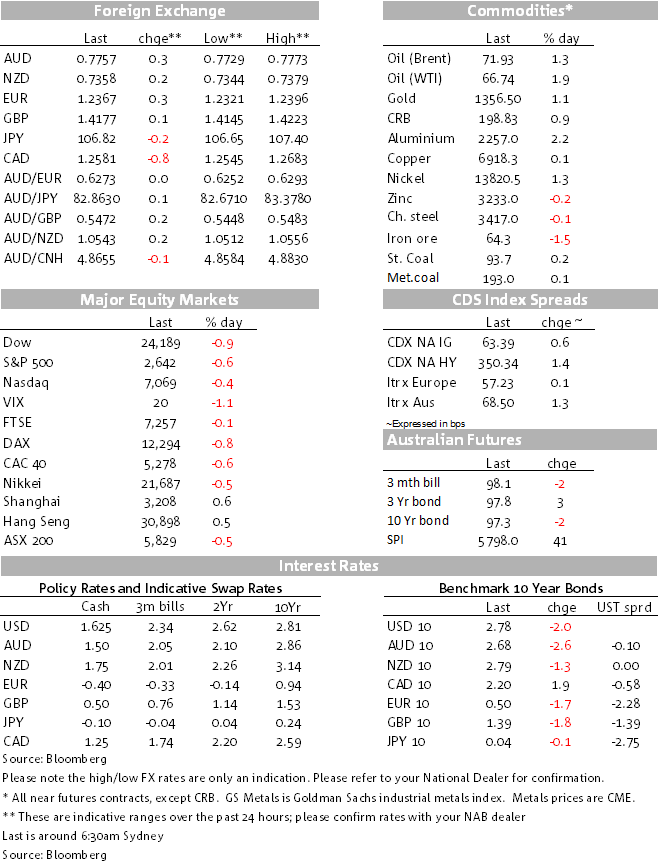

We come in this morning to the news that just 24 hours on from President Xi’s conciliatory speech to the Boao Forum advocating market opening and there’s a semblance of a risk-off market mood. Northern Hemisphere equity markets have closed lower, the Dow closing down 218 points, though not closing on its intra-day lows. Bonds have had a modest bid tone, though again yields are above intra-day lows. The VIX is down slightly to 20.23 (-0.23), oil, base metals and gold are higher (oil the more so), while major currencies have not changed trajectory. The AUD sits at 0.7755/60 this morning. The Rouble is down over 3%.

The reason for this backward risk step has been the reaction from President Trump to more unsettling news about Syria and speculation of European/US missile retaliation. In a tweet before the US market had opened, the President tweeted: “Russia vows to shoot down any and all missiles fired at Syria. Get ready Russia because they will be coming, nice and new and “smart”! He also tweeted that the relationship with Russia is worse than it has ever been, and that includes the Cold War.

That missile tweet was sufficient to frighten the horses to some extent, dampening risk sentiment. In other news, the US March Core CPI was right in line with expectations, increasing 0.2%, while the FOMC Minutes of the March 20/21 meeting had little impact, to be expected given the new forecasts and press conference after that meeting. Headline CPI fell 0.1% in March but annual growth increased from 2.2% to 2.4% thanks to base effects from a decline last March when super cheap cell phone pricing was sufficiently large to drag CPI lower. Core CPI also fell a year ago, while this March it rose by the expected 0.2% taking annual core CPI up to 2.1% from 1.8%. The flow through of this into the Core PCE deflator should see it also lift in March (due 30 April) up from 1.6% to 1.9%. In coming months, a continuation of the 0.2% m/m rise averaged over the past six months should see that deflator attain a 2 handle. Apart from a brief period early last year, it’s been seven years since the PCE deflator has had a 2 handle for any length of time.

It’s not surprising then that the FOMC has been becoming more confident of actually reaching their 2% inflation mandate. (Annualising the growth over the past six months is almost confirmation that the Fed is meeting its inflation mandate.) As to the future of Fed funds, there was wire coverage overnight given to the FOMC Minutes, especially to the Fed leaning toward faster rate hikes. “A number of participants indicated that the stronger outlook for economic activity, along with their increased confidence that inflation would return to 2 percent over the medium term, implied that the appropriate path for the federal funds rate over the next few years would likely be slightly steeper than they had previously expected”.

This can’t have been too surprising given not only last year’s tax cuts but the further bills passed to lift spending this year and indeed the tilt higher in Fed funds forecasts released after the March meeting, including the Fed lifting its dots for 2018 and a higher average for this year, if not quite the median. There was also some scepticism in the Minutes as to how much expansionary fiscal policy would boost potential output as opposed to just being a “sugar hit”. Two other morsels to note: first, the trade risk (agricultural contacts understandably worried), while the Fed discussed changing the language on the stance of monetary policy from accommodative to neutral at some point.

Draghi was also speaking overnight and shied away from directly engaging or batting back against the more strident view of shifting policy now in a more strident view espoused by Nowotny yesterday. Instead, you could be forgiven for thinking that he deflected it from a different angle, the trade/tariffs angle. He noted that while the direct effects of the tariff announcements or proposed were relatively modest, he will be watching to see what impact it has on confidence and the economy through that channel. He was quite upbeat on conditions in the Eurozone, bolstering an expectation that wages will eventually rise. This deflection played to the view that he’s in no rush to make any near term definite statements about what will happen after September when the current QE program ends.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.