Total spending grew 0.9% in June.

US equities extend Friday’s rally and Europe joins the party.

Phil Dobbie asks NAB’s Gavin Friend whether company buy backs could be part of this shift.

https://soundcloud.com/user-291029717/markets-up-budget-ignored-zuma-to-go

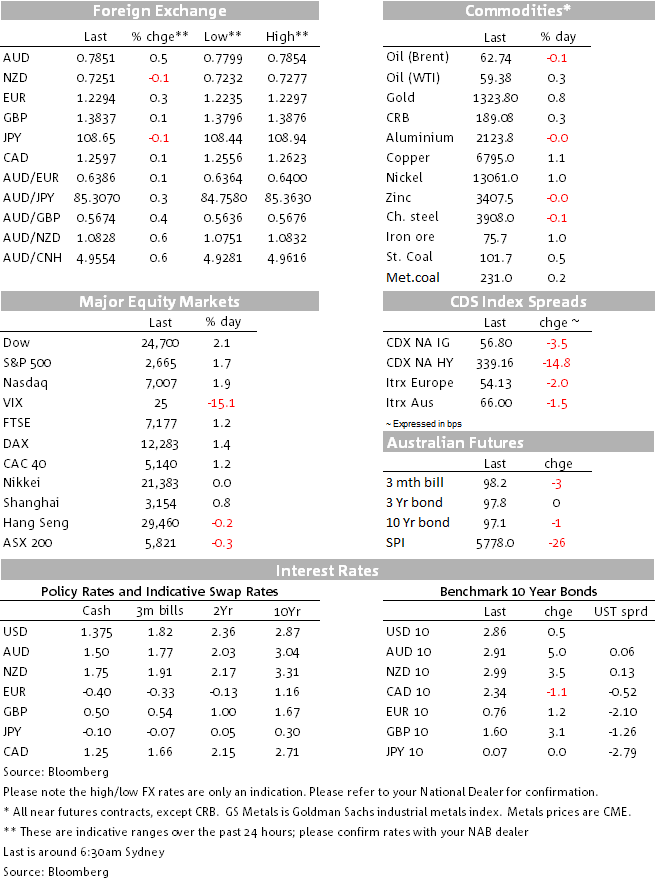

US equity markets have started the new week on a positive note and after two consecutive days of negative returns, European equities play catch up, posting gains across the board. Excluding the back end of the curve, UST yields are marginally higher and the USD has given back Friday’s gains. Commodities are up, helping the AUD outperform and late in the session President Trump unveiled his infrastructure plan to fix America’s crumbling infrastructure.

After taking a beating over the past two weeks, US equities are showing signs of stability and look set to record a second consecutive day of gains. Looking at the S&P500 sector breakdown all 11 sectors are up on the day with materials and financials leading the way. Meanwhile the steady rise in US equities since late Friday has helped the VIX index settle around the 26 mark and early in the session all major European equity indices closed in positive territory, ending a two day losing streak.

Ahead of the US CPI data on Wednesday, US Treasury yields opened the day higher, but then drifted a bit lower over the course of the overnight session. The 2y rate is essentially unchanged at 2.07%, 10y UST are currently trading at 2.85%, half a bps higher, but the back end of the curve has been the big mover with the 30y tenor down 2.5bps to 3.135%.

Yesterday during our APAC session, the USD eased a little bit and after a brief rally during the overnight session, it has eased again. DXY trades at 90.21, a smidgen above yesterday’s low of 90.073.Price action in G10 currencies has also been a little bit subdued although notably the NOK and AUD are up 0.54% and 0.36% respectively. A positive night for commodities is probably one factor supporting these currencies, although after a solid opening, oil prices have started to roll in the past few hours. Meanwhile copper and iron ore have led the way with both commodities up over 1%.

The AUD intraday chart shows the currency on a steady upward path and the pair currently trades at 0.7850, almost a full cent higher relative to the lows seen on Friday. NZD on the other hand has struggled overnight, down nearly all crosses . The kiwi briefly traded to an overnight high of 0.7277 and currently trades at 0.7250. Meanwhile the AUDNZD cross is back above 1.08, after trading to a low of 1.0748 on Friday.

EUR is a little bit stronger at 1.2290, up 0.27% and looks set to end a fourth consecutive day with a 1.22 in front of it. Meanwhile and ahead of the UK CPI release tonight, GBP is little changed at 1.3839. Overnight, BoE’s Vlieghe endorsed last week’s view of the MPC in commenting that a bit more than three 25bp policy rate increases were probably needed over the next three years. Under current market pricing of three hikes over three years the economy would still have excess demand and wouldn’t get inflation back to target. Fellow policy-maker McCafferty seemed to endorse that view as well, suggesting in a radio interview that it is likely rates would need to go up earlier. GBP hardly moved on the above comments.

Overnight President Trump unveiled a $200bn infrastructure plan aimed at fixing America’s crumbling infrastructure. The plan aims to encourage about $1trn of extra investment from the private sector, state and localities, but it falls short of the $2trn needed according to the American Society of Civil Engineers. States and localities budgets are tight and after the recent federal deductions, support for infrastructure is unlikely to come easily, the plan is also likely to face opposition in Congress from both Republicans and Democrats. Democrats have already unveiled an alternative plan of $1trn in direct Federal spending and after passing the huge budget and tax plan, fiscally Conservative Republicans are unlikely to support additional spending. So best guess is that after some wrangling in Congress the infrastructure plan, if passed, will look very different to the current proposal.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.