Total spending grew 0.9% in June.

The markets are waiting for today’s CPI figures from the US.

Phil Dobbie asks NAB’s David de Garis whether they will influence speculation on the path of rate rises this year.

https://soundcloud.com/user-291029717/will-cpi-rise-will-abe-go

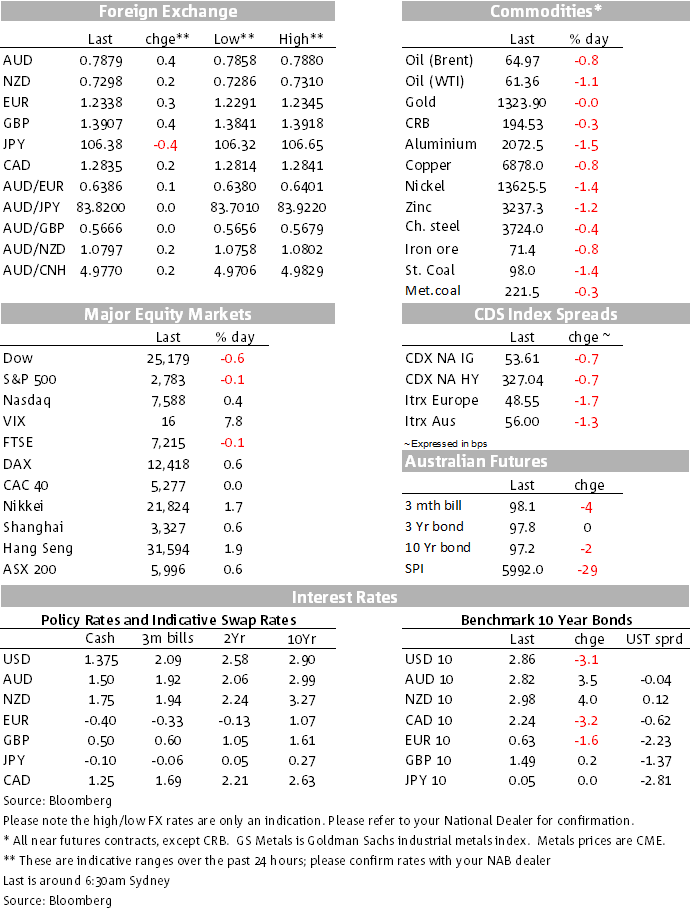

It’s been a night of very contained markets with US Treasury yields trading within recent ranges, stocks mixed, and the USD losing a little more ground against most majors. There’s been no major data of note. Notwithstanding a somewhat softer USD, base metals, oil, and gold were all lower overnight. China’s steel and iron ore futures yesterday saw little new change in price direction at the start of the week after the sizeable falls of last week, including for iron ore. Tomorrow sees the first glimpse at Chinese growth for the year with monthly growth data for Industrial Production, Retail Sales, and Fixed Assets Investment, this one is Feb year to date to traverse shifting Lunar year effects.

The US Treasury auctioned $28bn of 3 year Treasury notes and $21bn of 10s overnight. There was no sign of indigestion, nor pre-CPI nerves, from the bond market with 10 year yield down on net for the day by 2.75bps to 2.866% and the 3 year yield down by 0.8bps. The auction of 3 and 10 year Treasury bonds met with reasonably good demand ahead of the Treasury issuing 30 year bonds tonight. The bond market has been calm and measured.

After the Goldilocks payrolls report sugar hit for stocks on Friday, US equities have opened this week mixed. The Dow has given back some of Friday’s gains, down around ½%, while the S&P 500 is wavering at about square into the last hour of trade and the Nasdaq outperforming, up around ¼-½%. European equities made mostly some gains.

Most currencies have made up some ground on a soggy USD, though the NZD and the CAD have underperformed somewhat, the CAD seemingly held back by a pull-back in oil prices at the start of the week. The AUD has edged marginally higher against the USD, trading overnight in a 0.7855/0.7880 range, the Aussie currently toward the top end of that range. After rising from 0.7285 to 0.7323 during the local session yesterday, the Kiwi fell back to 0.73 overnight. RBNZ Acting Governor Grant Spencer is speaking today with the topic being “Getting the best out of macro-prudential policy”, although this is unlikely to be market-moving.

One currency that has been under the spotlight over the past 24 hours has been the Japanese yen over a re-developing political land scandal. The JPY strengthened yesterday afternoon in the wake of a growing scandal involving Japanese Prime Minister Abe and Finance Minister Aso. The scandal erupted last year, PM Abe saying at the time he would resign if he or his wife were implicated in a controversial sale of public land. The Ministry of Finance released a report yesterday stating that an MoF official had removed reference to PM Abe’s wife in a document related to the sale. Finance Minister Aso, a close ally of Abe, has come under pressure to resign, but yesterday said he had no intention of stepping down.

While a less stable government might ordinarily lessen support for that currency, the market is also mindful about whether this could potentially call into question the longevity of the Abenomics reflation agenda, which includes the BoJ’s QQE, if Abe is forced out. For now though, the market reaction has been reasonably contained and not suggestive of major political change, nor indeed a clear yen out-performance on the crosses so far this week. The USD/JPY has fallen from close to 107 yesterday lunchtime to around 106.35 now; AUD/JPY has been trading in the high 83s.

Ahead of the UK Chancellor’s Spring Statement tonight, the GBP has also been making some positive headway. The mood music around Brexit has been a little more positive after UK Brexit Minister Robin Walker said the UK and EU were very close to agreeing a transitional deal for after March-2019. Walker said “U.K. and EU’s access to each other’s markets should continue on current terms” during such an implementation period. The UK hopes to agree a transitional deal at next week’s EU Summit, although there is a risk that the ongoing dispute around the Irish border delays this; that’s certainly the event to watch. As for the Spring Statement on the economy with its forecasts for the economy and public borrowing, markets will also be closely eyeing an appendix that is expected to set out the costs of Brexit.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.