Total spending grew 0.9% in June.

The US dollar is on the slide again. As Phil Dobbie discusses with NAB’s Ray Attrill the volatility remains ahead of US CPI figures tonight.

https://soundcloud.com/user-291029717/valentines-day-nerves-ahead-of-cpi-aussie-nudges-higher

US stocks were off a few tenths of percent when I left for work but now less than an hour ahead of the close indices are all back in the green with gains of 0.1-0.3%. There’s no obvious catalyst for the intra-day turnaround, with all sectors bar energy showing similar sized gains. It must be love.

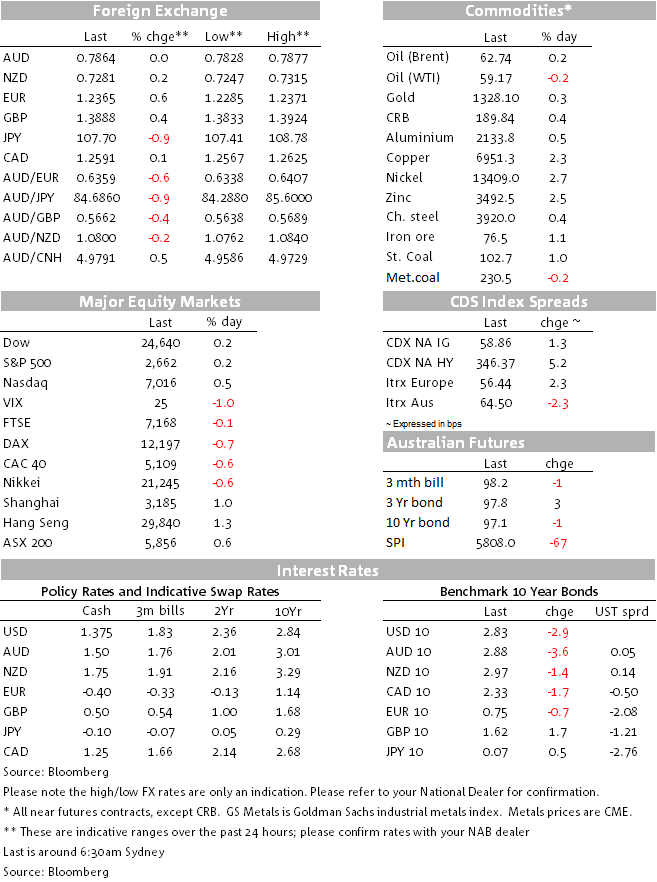

Energy stocks are being pressured by the sharp fall in oil prices in recent days – Brent and WTO crudes both off 12-13% in February to date – and where the sharp rise in the North American rig operating rig count and signs of inventory rebuilding have added significant momentum to moves that initially began when the US dollar started finding its feet at the beginning the month. I was listening to BP CEO Bob Dudley being interviewed on the business channels a few hours ago and he was adamant that the efficiency and speed to market of the shale oil producers meant that $50-65 was a much more realistic range for Brent crude in the coming few years than the $70+ levels we witnessed (briefly) last month. The oil-sensitive Canadian dollar is the weakest G10 currency overnight.

Bonds haven’t done a lot a lot with the Treasury yield curve (2s-10s) a few basis points flatter thanks largely to a 2-3bps uptick in 2-year yields (gains that are testament to market nervousness ahead of tonight’s all important US CPI release – more below). We had comments from Jerome Powell overnight following his swearing in as Fed chair, who said that global economy is recovering strongly for the first time in a decade, that the Fed is in the process of ‘gradually’ raising rates and trimming its balance sheet, and that ‘we will remain alert to any developing risks to financial stability’. Cleveland Fed President Loretta Mester also spoke and was non-committal about how many rate hikes she favoured this year (or indeed whether March was the likely date for a next move). Gradual rate hikes are still appropriate, she says.

The more interesting market moves overnight have been in FX, where significant USD/JPY slippage in our day Tuesday (testing ¥108) was pressuring the DXY index (13.6% weight) alongside a failure of Japanese equities to key positively off the prior two days’ US stocks market gains. The pair lost another ¥0.5 to ¥107.50 in London, with pressure on USD indices then compounded by a jump in Sterling after December’s inflation figures printed 1/10% stronger than expected to leave annual CPI inflation at 3.0% rather than fall back to 2.9% as had been expected.

EUR/USD has also been finding some love following the early month drop from 1.25 to 1.22. The general point to make about the big dollar here is that there is righty now more focus on the ‘twin deficits’ implications of US tax reform (and the spending increases approved last week) rather than the potential short term growth/Fed policy implications. Rising twin deficits historically go hand in hand with a falling US dollar.

AUD has been more of a sideshow in the last 24 hours but has suffered a bit alongside other commodity currencies. There was little reaction to yesterday’s NAB business survey, which overall conforms with the RBA view of economy – better activity, but retail lagging, prices and wages not showing much movement as yet, but capacity use trends suggests reasons for expecting that they will pick up in time. In a speech by RBA assistant governor Luci Ellis yesterday, she noted that “Our central forecast is that this weakness will end as the drag from the end of the boom dissipates and spare capacity is absorbed, such that average earnings growth recovers. There is no guarantee of this, though, and therein lies the risk.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.