Asset finance and leasing is in a growth phase in Australia as organisations seek a capital-effective way to modernise and upgrade across a broad range of asset classes and industries.

Will the Syria missile strikes hit the markets today. @NAB’s Ray Attrill says not on today’s edition of #TheMorningCall podcast

https://soundcloud.com/user-291029717/syria-strikes-unlikely-to-hit-markets

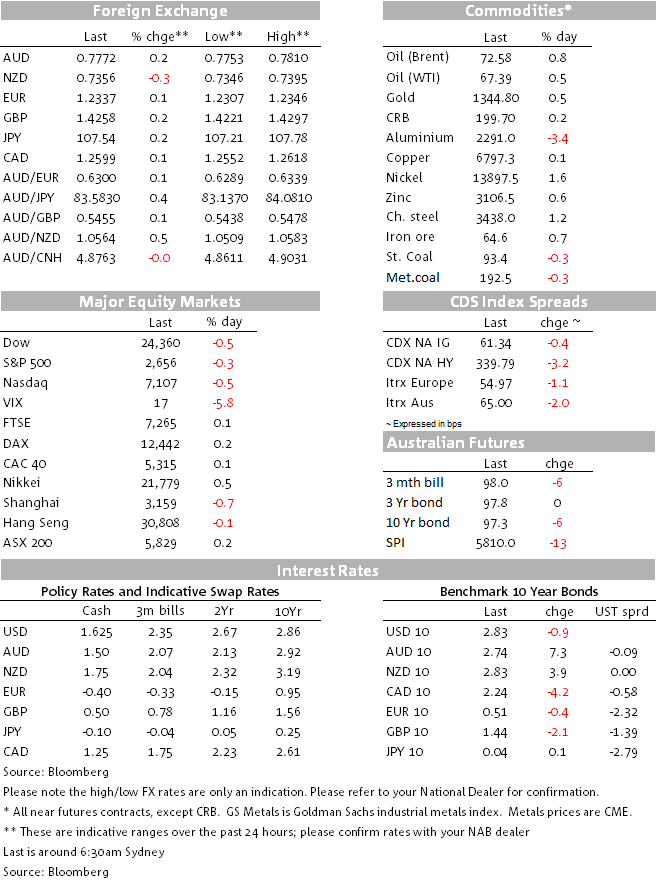

Friday night’s joint US UK and French air strikes against Syria have thus far drawn only verbal condemnation from Russia (and too Iran and China) with Russia’s prediction of ‘global chaos’ if the West hits Syria again not filling markets with fresh dread, at least judging from the limited FX mark movements evident in the first two hours of the new trading week. Both the risk-sensitive Australia and New Zealand dollars have started the week marginally weaker than they ended on Friday night, prior to the military action against Syria.

On Friday, JP Morgan, CitiiGroup and Wells Fargo all beat their street estimates for Q1 earnings yet their stocks all fell, showing just how high the bar has been set for earnings growth to continue propelling stocks forward. JPM’s adjusted EPS of $2.37 beat its $2.27 estimate, Citi reported EPS of $1.68 against $1.61 expected. Wells Fargo reported $1.12 against $1.06 expected. The latter’s stock fell 3.1% after disclosing it faces additional penalties of as much as $1 billion linked to auto insurance and mortgage sales practises.

Not helping the broader market was a downside surprise on the UoM consumer sentiment reading (97.8 from 101.4 last and 100.3 expected). The February March stocks market volatility received the blame, though the absolute level of confidence remains very elevated (the prior reading was after all the highest since early 2004).

Despite Friday’s dip in all the major US stock indices, of between 0.3% and 0.5%, they all produced decent gains on the week, NADAQ leading the way despite the recent travails of the some of the ‘FANGS” stocks. The VIX closed the week a point lower at 19.0

In FX, it turned out to be a fairly uneventful Friday save for another pasting for the SEK adding to the earlier week post CPI pain, off another 0.8%. AUD was well ahead of the G10 pack after punching above 0.78 to a high of 0.7806 in mid-morning London trade before pulling back to 0.7764 to be just 0.13% up on the day (still the best performer). The other commodity linked currencies, NZD, CAD and NOK, all finished lower despite oil adding another 30-60 cents: On the week, USD indices were down by 0.3-0.5% while NZD, CAD and AUD (in that order) were the top performers, all up over 1%:

US Treasury yields were narrowly mixed on Friday with the 2-10s curves flattening by another 2bps or so to 47bps. On the week 2s are up just under 9bps and 10s just over 5bps:

In commodities, oil continues to push ahead on an enduring impact from the factors that have been driving it up for a few weeks now (geopolitics – speculation of US policy on Iran in particular – declining inventories – below 5 year averages – and Saudi’s reported desire to see Brent at $80). Friday’s Baker Hughes rig count saw US drillers adding a further seven rigs, bringing the total to 815, the highest since March 2015, but evidently we are not seeing a ramp up in North American shale oil production to counter these other influences. Iron ore and gold were also higher Friday but coal and the broader metals complex were lower. On the week oil is up an impressive 8%+ with coal (both metallurgical and steaming) the only hard commodity to be lower:

In other news Friday, the US Treasury Department’s semi-annual report to Congress on macroeconomic and foreign exchange policies of major trading partners has added India to the list of countries whose foreign exchange and economic policies are under its close scrutiny, while again opting not to accuse leading trading partners of being currency manipulators. So the Treasury decide once again not to label China a currency manipulator despite President Donald Trump’s vows during the election campaign that he would do so. The report declared nevertheless that the Trump administration is “deeply concerned” by the large trade imbalances that exist across the world economy. “China has an extremely large and persistent bilateral trade surplus with the United States, by far the largest among any of the United States’ major trading partners,” it said. The report also said the China’s economic development was going in an “increasingly non-market direction”.

Boston Fed President Eric Rosengren (hawk) said Friday the Federal Reserve will probably need to raise interest rates at least three more times this year in the face of a robust U.S. economy, even while possible trade disruptions pose risks. In contrast St. Louis Fed President James Bullard (dove) said he’s worries aggressive rate rises could invert the yield curve later this year or next and sees no reason to lift rates now.

Finally, China published its March money supply and credit growth numbers on Friday evening and they all came in a fair bit softer than expected and down in annual growth terms from the start of the year. March M2 money supply printed 8.2% y/y (8.9%E, 8.8%P) and the broad Aggregate Social Financing credit measure ¥1,330bn (1,800bn E, 1,173.6bn P). These come in front of Tuesday’s Q1 GDP and march activity readings, and suggest some risk of small downside surprise on the latter, industrial production in particular.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Asset finance and leasing is in a growth phase in Australia as organisations seek a capital-effective way to modernise and upgrade across a broad range of asset classes and industries.

Growth in the major advanced economies bounced back in Q2

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.