Total spending grew 0.9% in June.

USD is set to close lower for a 4th consecutive day and US equities look set to climb for a fifth day in a row

Phil Dobbie talks to Rodrigo Catril about the latest US data, Europe’s widening trade gap with the US, the rise and rise of the Japanese Yen, and what we can expect from RBA Governor Philip Lowe at a the House of Reps Standing Committee today.

https://soundcloud.com/user-291029717/more-inflation-signals-but-recovery-continues

After an initial wobble , US equities have recovered and look set to climb for a fifth day in a row.10y UST yields are unchanged after trading to a new 4 year high while the US dollar has continued to fall and is now down almost 2% so far this week. Lunar New year celebrations for the Year of the Dog begin in Asia with China, Singapore and Hong Kong amongst other Asian countries out today.

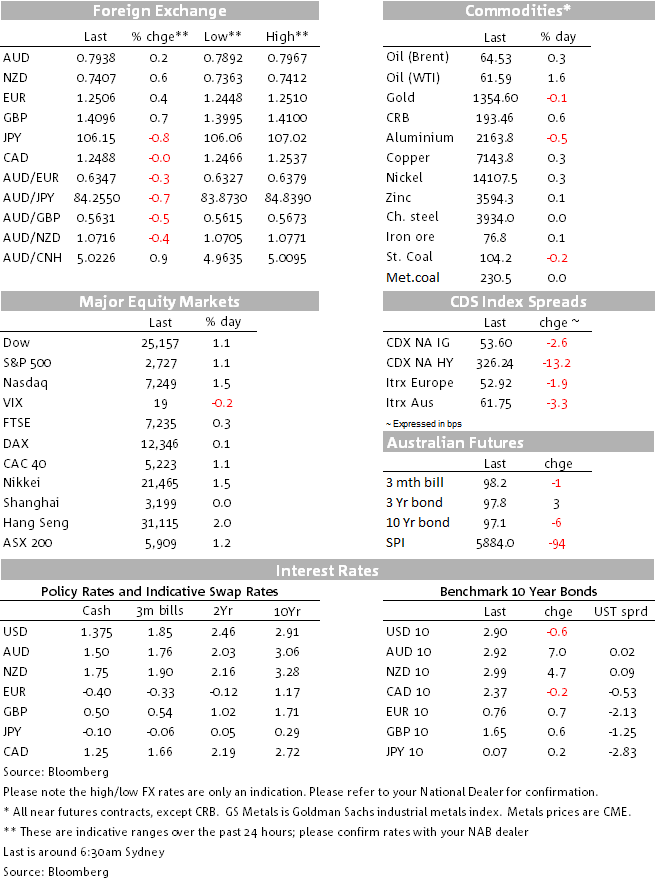

After falling almost 1% early in the overnight session, the S&P500 is now trading close to 1% up and the intraday charts show a similar pattern for the Dow Jones and NASDAQ indices. US equities are up around 5% to 6% in the past five days, after losing around 8% to 9% in the previous 5 days. Meanwhile, over this 10 day period and amid further evidence of higher inflation, UST yields have continued to climb. Two Monday’s ago 10y UST yields closed at 2.70% and now the 10y tenor trades at 2.89%, after reaching a new four year high of 2.94% during the overnight session.

For now it seems that US equities are coming to terms with a higher yield environment, however with recent inflation readings surprising to the upside, UST yields still have the potential to climb higher. As long as US data support the prospects for higher economic growth then, in theory, US equities should be able to cope with a higher yield environment. For now that seems to be the case, but if US Treasury yields climb above 3%, the ability for US equities to cope is likely to remain questionable. We suspect the push-me/pull-you contest between yields and stocks is likely to remain a market theme for a while yet.

Meanwhile, USD dollar weakness remains the main theme in currencies. CHF (0.73%) and JPY (0.71%) are the big outperformers in G10, so despite the risk positive environment evident in equities, there is a clear bid for safe haven currencies. JPY strength was aided by comments from Japanese finance minister Taro Aso, noting that yen’s strength was not abrupt enough to trigger intervention. GBP has also had a good night, up 0.67% with the pair now threatening to move above the 1.41 mark after trading down to a low of 1.3800 two days ago. News of a softening in EU negotiation stand appears to have been the trigger for GBP with Politico reporting that EU officials are considering watering down the mechanism that would sanction the UK if it breaks EU rules during the Brexit transition periods. Later, an EU official said that no decision had been taken.

Amid a broad soft USD environment, CAD and AUD are the strugglers over the past 24hrs with both currencies little changed against the USD. Yesterday’s AU Labour market report came in line with expectations, revealing a 16K net job gain (+15k consensus) with the jobless rate also printing in line with expectations at 5.5%. The detail looked a little bleaker with -50k full-time jobs and the creation of 66k part-time positions. This might have been a factor weighing on the AUD overnight, although underperformance against other crosses might have been at play too, AUDJPY for instance had another look sub ¥84 overnight and AUDNZD has remained in a downtrend, reaching an overnight low of 1.0705. Higher oil prices (WTI +0.3% and Brent 1.6%) didn’t help the CAD, but just like the AUD, crosses underperformance are probably a downward factor. EURCAD, for instance, made a fresh 2 year high overnight.

In economic news, US PPI was +0.4% m/m in Jan, matching the consensus, however, the core measure ex food & energy beat expectations printing at +0.4% m/m, above the +0.2% consensus. Meanwhile, US Industrial Production was -0.1% m/m in Jan, below the +0.2% consensus. So although recent US economic data has come below expectations and below levels activity indicators have been suggesting, inflation readings have continued surprise on the upside.

Lastly on the other side of the Atlantic, Eurostat reported that the EU’s trade surplus with the US rose by 7% to $160bn in 2017 despite the stronger euro. Jason Wong, our BNZ market strategist notes that the report supports the view that in a medium-long term context the euro is still a cheap currency despite its recent strong appreciation, while data like this might also get the attention of President Trump and his penchant for imposing trade barriers.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.