Inflation still too high despite slow demand growth

Insight

It’s company earnings and global politics driving markets today. @NAB’s Rodrigo Catril joins Phil Dobbie to talk about President Trump, Shinzo Abe, Theresa May, Michael Cohen and the next Deputy Governor of the US Federal Reserve.

https://soundcloud.com/user-291029717/syria-blows-over-strong-earnings-new-fed-vice-chair-struggles-for-brexit-and-abe-cohen-in-court

Weezer’s little known 2009 track ”Run over by a truck”, tells the story from the overnight session. Strong earnings reports by trucking companies have helped US equities end the day in a positive note shifting focus away from geopolitics and back to fundamentals. The USD is weaker on the back of President Trump’s tweet accusing China and Russia of playing “currency devaluation game” and Richard Clarida gets Trump’s nod for Fed Vice chair.

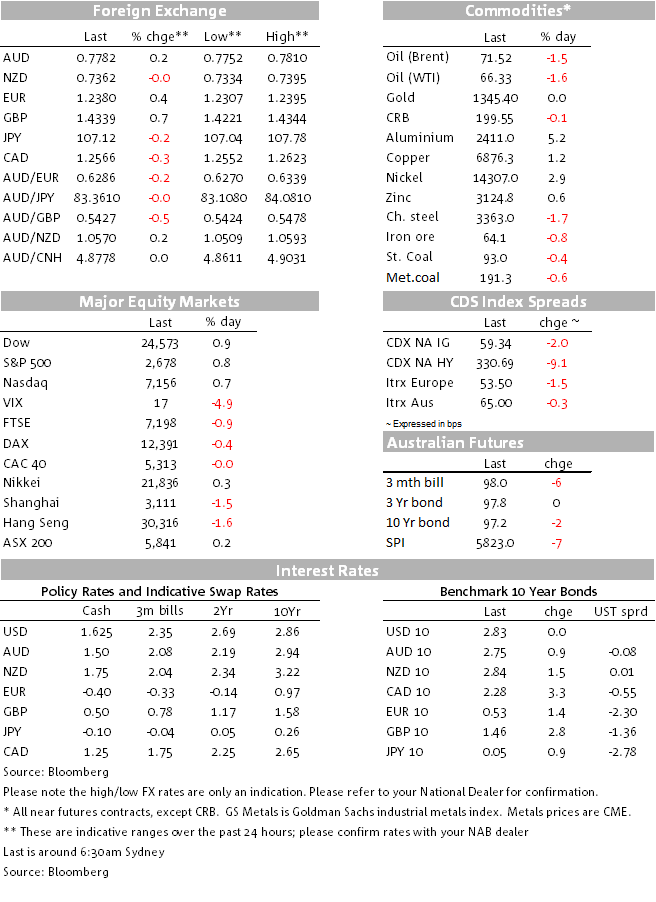

After a mixed Asia session and a negative European close, US equities have ended in positive territory with the market shifting focus away from geopolitics and back on to fundamentals as the US reporting season gets underway. Old School companies were on the spotlight with trucking firms and rail-road operators reporting decent earnings, boosting gains on major US equity indices. The Dow closed 0.87%, S&P gained 0.81% and the NASDAQ closed 0.70% higher. After the bell Netflix reported better than expected results with its shares initially jumping over 8% in extended trading.

Meanwhile, early in the session Bank of America reported better than expected earnings (following Citi, JPM and Wells Fargo on Friday) and the shares outperformed (0.47%) the S&P banking sector (-0.12%). But just like the other US banks, anaemic loan growth was the one question mark on the results.

The USD is broadly softer and both DXY (0.43%) and BBXDY (-0.28%) have retained their downtrend established since early in April. A tweet from President Trump accusing China and Russia of “playing the currency devaluation game” didn’t help greenback, but the move lower in UST yields might have been a factor too. President Trump did not offer any evidence to substantiate his accusations against China and Russia, still his comments were somewhat surprising given that only a few days ago a US Treasury report concluded that no country was currently manipulating its exchange rate. Looking at the charts, CNY has been on a steady appreciation over the past year and we could argue that Rubble’s weakness has more to do with Putin’s political decisions. Cynic would suggest that Trump’s complains for other currencies to be stronger mask his true desire for a weaker US dollar.

Looking at G10 currencies in more detail, after a few days under the cosh, SEK (+0.67%) had a small rebound overnight and GBP was the other outperformer on no new news. The Pound appears to be benefiting from technicals suggesting the currency has room to move higher, not only against the USD, but also against other currencies such as EUR and even AUD. That said, the withdrawal bill is the political focus in the UK this week, , the House of Lords is expected to vote in favour of continuing in the common customs union, an outcome which may set the tone for Parliament’s final vote later this year on Britain’s withdrawal from the European Union.

The AUD and NZD were bystanders in the overnight session with both pairs little changed. AUD currently trades at 0.7780 and NZD sits at 0.7363. RBNZ Governor Orr has been doing a round of interviews (radio yesterday, NZ Herald today) and our BNZ Strategist Jason Wong notes the Governor is coming across as a practical policy maker and keen to improve RBNZ communications. Orr said speculation on whether he’d be a more hawkish or dovish governor – more inclined to raise or cut rates – was naive. Orr said he wasn’t bringing any new “frameworks or theories” about how the economy works. “You just have to take the context in and make the best decision at the time.”

10y UST yields are unchanged at 2.82%, after reaching an overnight high of 2.8617%. Front end yields have held up, leaving the curve flatter. US retail sales met expectations (headline 0.6% m/m, core 0.3% m/m). The Atlanta Fed GDPNow estimate of Q1 GDP was essentially unchanged at around 1.9% (annualised). Fed speak couldn’t add much to the market’s thinking, although both Dudley and Kashkari said the Fed shouldn’t overreact to a modest inflation overshoot.

In other Fed news, President Trump announced his intention to nominate Richard Clarida, a respected economist and PIMCO adviser, as vice chairman of the Federal Reserve. News articles describe the Columbia Professor as “centrist and pragmatic” and Bloomberg notes that in a December interview Clarida noted that the US neutral rate is probably closer to 2% rather than 3%. But Clarida also said at the time that “We could get four hikes if the growth in the economy is stronger because of the tax cuts,” adding that “But importantly, also, you’d actually need some indication that inflation is moving up too quickly for the Fed’s taste.”

Trump also announced his intention to nominate Kansas State Bank Commissioner Michelle Bowman as Fed governor representing the interests of community banks. Both selections, which were first reported by the Wall Street Journal, are subject to confirmation by the US Senate.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Inflation still too high despite slow demand growth

Insight

Trade tensions continue to mount, with critics claiming that China is exporting its industrial overcapacity

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.