Online retail sales growth slowed in May following a fairly strong April

Insight

Focus is currently on Washington where a US government shutdown deadline looms this weekend unless a stopgap funding bill is agreed.

Overview:

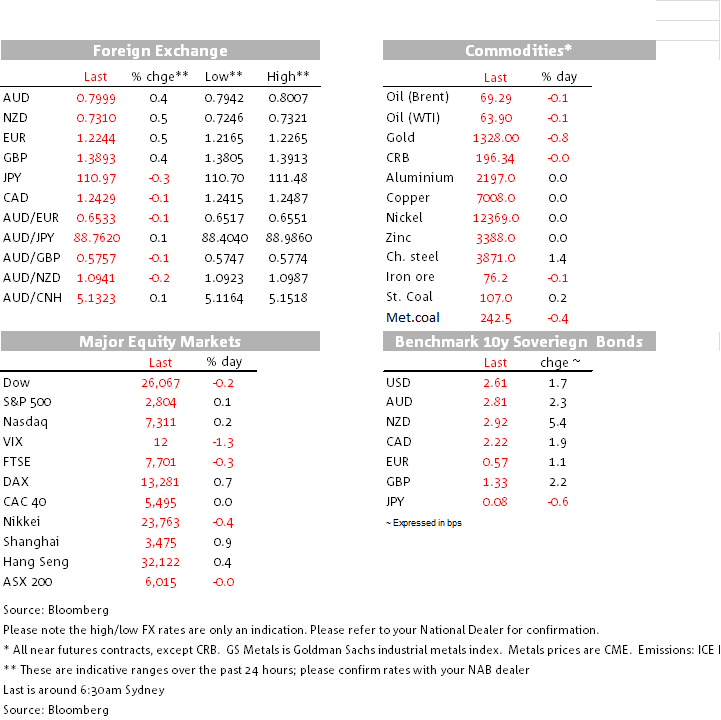

Focus is currently on Washington where a US government shutdown deadline looms this weekend unless a stopgap funding bill is agreed. That hasn’t perturbed US equities, which remain near their recent record high, but USD indices show a distinctly lower trend as the hours tick by with no agreement, while the US 10-year rate pushed up through 2.60% for the first time since March. At the time of timing we still await a vote on a stop-gap spending bill, with a tweet by Trump last night adding to the difficulty in getting agreement.

With all this going on, economic data have taken a backseat. US data were mixed, but dismissed by the market fairly readily due to their inherent volatility – a plunge in jobless claims following their recent upward spike; and ditto for housing starts, while permits were in line. A slightly weaker Philly Fed survey might be explained by harsh weather. On a more positive note, China data confirmed that growth was solid, with full-year GDP rising by 6.9%, its first increase since 2010. Retail sales growth was weaker than expected but all the other key indicators were slightly stronger.

Angst around the possibility of the US government shutdown may have been a factor in pushing the US 10-year rate up to as high as 2.62%, just 1bp shy of the peak in March last year and a key technical level to watch. We’ve been down this road many times before, with noise about the US government shutting down and possibility of defaulting on an interest payment, but the end result has always been a kicking of the can down the road and no default event. But one doesn’t need to search hard to find reasons why rates are back up to 2.6%, with the upward trend this year easily explainable by the stronger US growth and inflation picture and higher conviction on further Fed tightening this year.

Outgoing NY Fed President Dudley gave an interview to the FT where he suggested that the Fed should put a review of its inflation target on the agenda this year, investigating the case for moving to a price level target to achieve inflation of 2% over the medium to longer run or moving to a range like 1.5-2.5%. On current monetary policy, his view seemed to be in line with the Fed’s forecast of three rate hikes this year and on the hawkish side he indicated that the balance of risks is shifting away from inflation being too low to the risk of the economy overheating.

Broadly based USD weakness has seen the AUD retest the 0.80 mark this morning, twice, but failing to push on higher, with 0.8007 being the peak. Arguably, the AUD deserved to push higher anyway following its fall after yesterday afternoon’s employment report, where the market chose to focus on the nudge up in the unemployment rate and ignore the stronger jobs data. That data helped pushed AUD/NZD down to 1.0930 by the Sydney close, where it met support and it trades this morning slightly higher.

Amidst the weaker USD backdrop, EUR is hovering up around the 1.2240 mark and GBP traded back up through 1.39 this morning. USD/JPY traded down to 110.70 but has since recovered to a 111 handle.

A light calendar during Asian trading hours. NZ PMI data will be released where we’ll be seeing if activity has held up or not post-election despite the plunge in business confidence. The NZ Black Caps are on a winning streak and should easily make it 5-0 against Pakistan today.

Globally, the key focus will remain on US shutdown risks. The economic calendar looks light with UK retail sales and US University of Michigan consumer sentiment, with the speech by the Fed’s newcomer Bostic on the US economy of some interest.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.