Total spending grew 0.9% in June.

Lots of numbers out overnight but it’s politics driving the markets right now, with President Trump saying he will sign the order next week to impose tariffs on steel imports.

Phil Dobbie talks to NAB’s Rodrigo Catril about the market reaction. Plus, an election this weekend in Italy, the SDP vote in Germany that could determine whether another general election is imminent, and Theresa May’s response to the EU – what’s her answer to the Irish border question?

https://soundcloud.com/user-291029717/trump-rolls-out-steel-tariffs-politics-dominates-europe

Risk sentiment has taken a beaten in the past few hours after President Trump confirmed that he plans to impose import tariffs on steel and aluminium next week. US equities were struggling earlier in the session, but the announcement triggered a sell-off across the board with steel and aluminium companies the notable exceptions. UST yields are lower with the move led by the 5y part of the curve and after initially holding its ground, the USD has come under pressure in the hour. The line in Jimmy Barnes working class man lyrics “ he’s a steel town disciple” almost made it into today’s title, but I just couldn’t passed up the chance to use Superman (man of steel) by REM or Eminem!

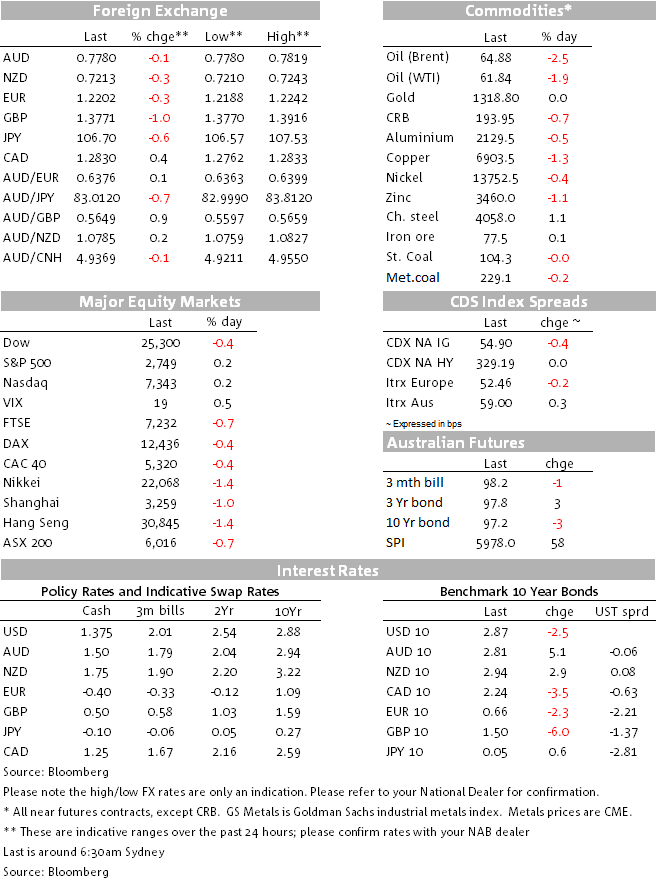

After a mixed Asian session and a soft European close, US equities opened under pressure, but then settled into a sideway pattern. This all changed in the afternoon session after President Trump confirmed his plan to impose new tariffs on steel and aluminium next week. Trade war fears and potential impact on inflation sparked a sell off in risk assets and a bid for US Treasuries. The Dow, S&P and NASDAQ now look set to end a third day in a row with negative returns and after five days of trading with a 1 in front of it, the VIX index currently trades around 23.

Risk aversion rather than concerns over additional inflationary pressures has seen UST yields move lower along the curve with the 5y tenor leading the way, down 5.4bps to 2.587%. Earlier in the session, UST yields moved a little bit lower following slightly dovish comments from Fed Chair Powell before his Senate appearance. The Fed Chair said that he sees no signs the US economy is overheating even as the outlook for growth strengthens and the labour market tightens, he then added that he didn’t see “any strong evidence yet of a decisive move up in wages.”. The move lower in yields was then reversed after Fed Dudley said that he was ‘even more confident’ in pursuing rate rises adding that “four rate rises in 2018 would still be gradual”.

Meanwhile on another day, the unexpected jump in the ISM manufacturing (60.8 vs 58.7 exp.) to its highest level since May 2004 would have been a catalyst for a bid in risk assets and higher UST yields, in the end however trade threats trumped the strong data. Notably too, all the key subcomponents of the survey were strong with the ‘prices paid’ index rising to its highest level since 2011 and, encouragingly ahead of payrolls, the employment index also rose to near mutli-year highs. US PCE data was also out overnight, core PCE prices were +0.3% m/m in January, matching consensus, leaving the yoy number unchanged at 1.5%.

When I walked in this morning and looked at the screens, the USD was little changed and the AUD and CAD were the big underperformers. My rationale at the time was that the AUD was still suffering from yesterday’s soft capex report while news of US tariffs and implicit concerns over trade war appeared to have weighed the most on the CAD (Canada is the US’s largest foreign supplier of steel) and partly on the AUD, given the openness of both the Australian and Canadian economies. The odd one out at the time was the Kiwi, which was outperforming the USD. That all changed in the past hour, the USD appears to have succumbed to the move lower in UST yields and now the greenback is softer across the board. Early in the session DXY was threatening to make a break above 91 and now the index is at 90.30,over half percent lower in the past hour.

After trading to an overnight low of 0.7713, the AUD has essentially erased all the losses post yesterday’s capex report and at 0.7763, the pair is essentially unchanged over the past 24 hrs. NZD (@0.7256) and NOK (@7.84) are the top performers up 0.76% and 0.60% respectively and the Euro is not far behind up 0.57% and currently trading at 1.226. We remain cautious on the broad USD sell-off, if Trump’s decision to impose tariffs triggers a retaliation by the US main trading partners, a trade war is not just a negative for risk assets, it is also a negative for small and open economies such as Australia. Thus, we wouldn’t be surprise to see the big dollar regaining its poise against currencies such as the AUD, CAD and NZD. Meanwhile safe haven currencies such as JPY and CHF are likely to be the winners with the Euro not too far behind.

As for commodities oil prices are softer, although they have settled a bit in the past hour. Copper and nickel are also a bit lower and iron is unchanged.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.