Online retail sales growth slowed in May following a fairly strong April

Insight

The US Treasury plans to issue $151 billion in bonds today, $258 billion across the week.

Phil Dobbie asks NAB’s Rodrigo Catril what this will mean for bond yields in the US and around the world. They also discuss the big correction – is it over yet? – and Japan’s trade balance.

https://soundcloud.com/user-291029717/roll-up-roll-up-its-the-258-billion-treasuries-sale

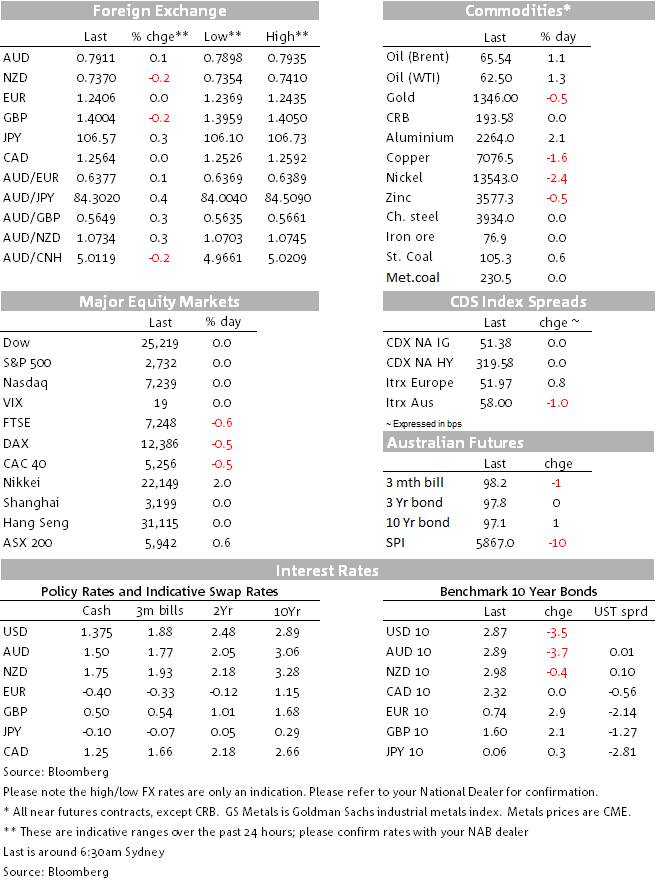

Amid a thin holiday trading environment with China, Hong Kong, the US and Canada all out on Monday, European equities were unable to follow the positive lead from Japan, closing marginally lower. European bond yields pushed up with the move led by the back end of the curve, oil prices continued to march higher while moves in currency have been rather subdued. Governor Carney has been speaking this morning and just like The Who, he admits he has no idea when the next UK financial crisis will be, but the best strategy is to prepare for it nonetheless.

Yesterday in our session Japanese’s equities had a solid day with the Nikkei up almost 2%, its best daily performance since January this year. Our own S&P/ASX 200 also closed higher, but this positive lead from Asia didn’t have a lasting effect in Europe overnight. After initially opening higher, European equities drifted lower over the course of the session with the STX Europe 600 index closing 0.63% down on the day.

Meanwhile European government bonds drifted higher with the move led by the back end of the curve. 30y Bunds climbed 4.6bps to 1.388% while the 10y tenor rose 2.8bps to 0.73%. UK Gilts also rose with the 10y bond climbing 2bps to 1.60%.

After an initial surge close to the end of the European session, USD indices have given back most of these gains and are essentially unchanged over the pat 24hrs. Looking at G10 currencies, JPY is the big underperformer, down 0.32% against the USD and the pair currently trades at ¥106.55, almost one big figure above the lows recorded last week. Yesterday’s Japan better than expected trade data had little effect on the currency, but the positive move seen in the domestic equity market appears to have been the driver for the softer yen. That said given the sharp decline in USD/JPY over the past week, is not that surprising to see the currency stage a small rebound.

GBP briefly traded sub 1.40 overnight and BoE Governor Carney’s speech this morning didn’t elicit a reaction by the currency. The Governor said that “Something will go wrong again even if we do not know exactly what or precisely when,” adding that “Accepting this means our best strategy is to create an anti-fragile system that can withstand potential shocks when they happen.”

In commodities, oil prices have continued to surge higher with WTI +1.3% and Brent 1.9%. Soothing words from OPEC representatives appears to have been the driver for the gains. The “market rebalancing has gained massive momentum” as the Organization of Petroleum Exporting Countries and its partners work to trim output, OPEC Secretary-General Mohammad Barkindo said Monday in Nigeria. Meanwhile, United Arab Emirates Energy Minister Suhail Al Mazrouei said OPEC, Russia and other producers are looking at ways to “institutionalize” their cooperation beyond the end of this year.

Although the AUD has had a quiet session, up 0.06% over the past 24hrs and currently trading at 0.7911, relative to other G10 currencies, the AUD is the best performer, followed closely by NOK and DKK. The move higher in oil prices probably played a supporting role for the AUD and NOK, although looking at other commodities, performance has been mixed. Iron ore is unchanged at $76.89 while gold is down 0.53% and copper is off 1.6%.

Last but not least NZD is a little bit softer, down 0.22%, but at 0.7370 the pair is still trading close to the upper end of its 0.7177-0.7437 range seen over the past month. Our BNZ strategist notes today’s NZ producer price inflation data is unlikely rattle the currency, but the GDT dairy auction overnight has more potential to cause movement if it comes out substantially different from indicators and BNZ’s expectation of a flat to small rise.

UST auction-rama begins early tomorrow with the US Treasury aiming for record-sized sales of three- and six-month bills ($151bn) and total issuance of $258bn on the week. The market will be looking at the auction results to gauge the appetite for US Treasury bills and bonds along with the potential rise in the cost of borrowing for the US government

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.