Coming in for landing in a heavy cross wind

Insight

The share markets rebounded today. NAB’s Tapas Strickland says it’s a positive sign that the reaction was contagion from tech stocks rather than anything more lasting.

Markets prepare for the Fed meeting, with an announcement tomorrow morning Australia time.

https://soundcloud.com/user-291029717/markets-rebound-ahead-of-fed-facebook-loses-friends

Some mornings finding a suitable title is, after getting up early, the hardest part of writing the morning note, and others like today, you are spoiled for choice. US and EU equities have edged higher, recovering some of yesterday’s tech led loses, but Facebook continues to lose friends (The Dandy Warhols edged Demi Lovato “Ruin the Friendship” and Placebo “Without you I ‘m nothing”). Ahead of the FOMC early tomorrow, the USD is a little bit stronger across the board and US Treasury yields are also a couple of bps higher.

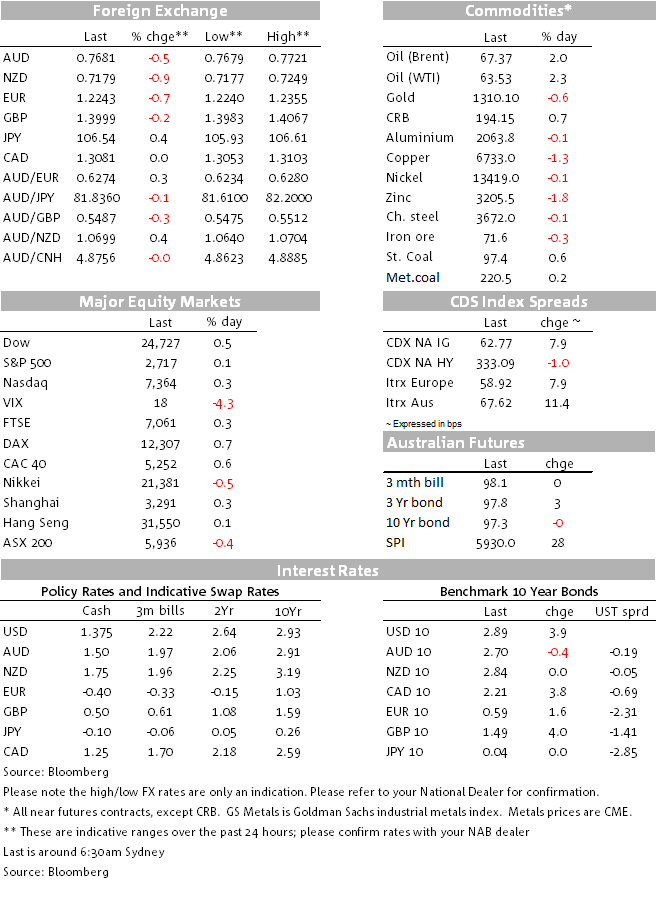

US and EU equities have recovered some of yesterday’s tech led loses with the energy sector leading the way. Oil prices jumped overnight ( WTI +2.16% and Brent 1.94%) boosting energy shares after reports that OPEC believes the global crude market will come into balance by the end of September, sooner than previously forecasts. Meanwhile, Facebook shares declined for a second consecutive day on the back of reports that several US Congress committees are probing whether Facebook breached the terms of privacy laws. The S&P 500 closed +0.15%, NASDAQ was +0.27% and the Dow +0.47%.

The USD is stronger against most currencies with NZD (-0.84%) and EUR (-0.70%) amongst the big underperformers while CAD is unchanged and at the top of the G10 leader board, boosted by the jump in oil prices . In index terms the USD is up 0.63% when looking at DXY and BBDXY is up 0.35%. Ahead of the FOMC early tomorrow, both indices are now closer to the upper edge of their ranges held since the start of the year.

Higher UST yields (up around 2.5bps across the curve) was one factor helping the USD and after yesterday’s Washington post report that Trump plans to unveil a package of $60bn in annual tariffs against China, aiming to protect US intellectual property and create more American jobs, an amicable reply from China probably also helped sentiment and the move higher in UST yields. Premier Li said that China wants to avoid a trade war and added that the government plans to further open the manufacturing sector and it won’t force foreign companies to transfer technology to domestic ones.

NZD underperformance started yesterday afternoon with the jump in the AUD/NZD cross from 1.0644 to 1.070, amid no news, suggesting flow was the driver. Then overnight NZD remained under the pressure with the latest GDT dairy auction printing a third consecutive price decline (-1.2%, in line with market) and early this morning Fonterra’s half year results also underwhelmed ( FY dividend seen at 25-35 NZ cents down from 40c). After trading to an intraday high of 0.7249, NZD now trades at 0.7179.

AUD is back below the 77c mark and currently trades at 0.7680. Yesterday the RBA Minutes didn’t have a lasting effect on the currency with the RBA reiterating its “gradual progress” mantra, while highlighting global growth momentum and positive signs on the outlook for wages (and the labour market). The currency traded to an overnight high of 0.7720, but then it was overwhelmed by the broad recovery in the USD. AUD now trades at 0.7681 with the uptrend line held since early 2016 now well in sight. The trend line currently suggests a break below 0.7598 opens the possibility for an easy passage towards 75c. The FOMC meeting early tomorrow will be important for the USD and both AUD and NZD look vulnerable to a big move lower if the Fed delivers a hawkish message ( see more below).

GBP has given back about half of yesterday’s gains with softer than expected inflation data easing concerns of an imminent hike by the BoE. Overnight both UK core and headline CPIs readings printed 0.1% below market expectations. That said, the wage data tonight will be more important ahead of the BoE’s Thursday night. Cable now trades just under the 1.40 mark and is one of the best G10 performers, down just 0.14% against the USD.

Looking at commodities, aside from oil, copper has had another down day (-1.36%) and iron ore is down 0.29% while the LMEX index is off 1.12%.

And in other news, the G20 meeting of finance ministers and central bankers has just ended with the communique highlighting the importance of trade as protectionism looms, adding in the comment “We are working to strengthen contribution of trade to our economies.”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.