Trade tensions continue to mount, with critics claiming that China is exporting its industrial overcapacity

Insight

Today’s Podcast Phil Dobbie asks NAB’s Gavin Friend whether they could lift bond yields, particularly given low interest in this week’s big auctions from the Treasury. Gavin also explains why the UK’s jobless figures are not as bad as they seem, how Brexit talks are reaching the pointy end, and what will be the consequences […]

Phil Dobbie asks NAB’s Gavin Friend whether they could lift bond yields, particularly given low interest in this week’s big auctions from the Treasury. Gavin also explains why the UK’s jobless figures are not as bad as they seem, how Brexit talks are reaching the pointy end, and what will be the consequences of yesterday’s rising wages data in Australia.

https://soundcloud.com/user-291029717/whos-buying-bonds-is-britain-really-losing-jobs-are-aussie-wages-really-growing

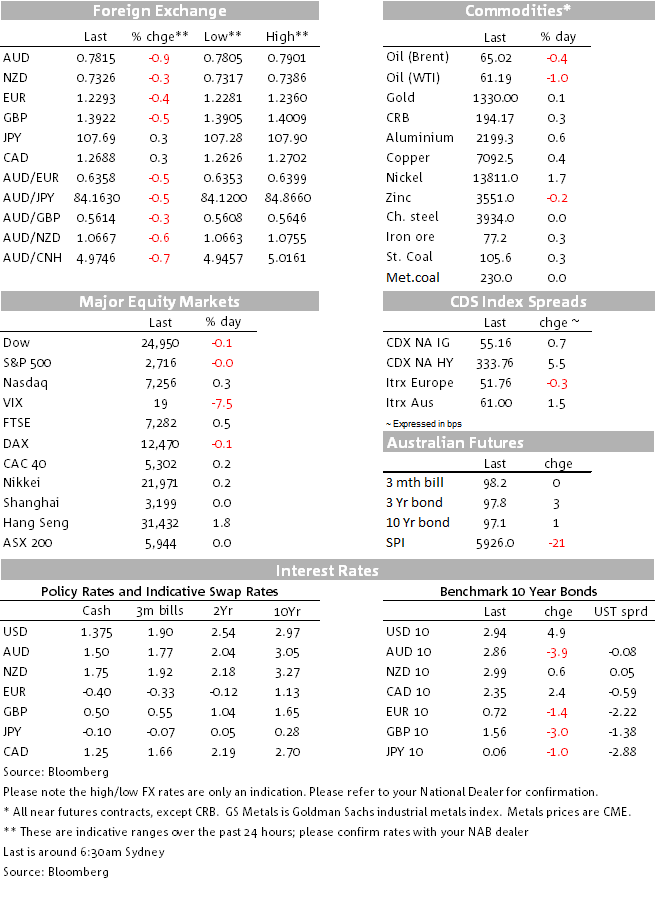

Initial reaction to the Fed minutes was on the dovish side putting the dollar under pressure amid a rally in UST yields. The dovish take also boosted US equities, but as type these initial moves look to reversing. The UST yield curve is steepening led by the back end of the curve and USD indices are stronger after dropping about 0.30% immediately after the Minutes release.

Markets were essentially marking time ahead of the Minutes and as seen in previous days, the USD was still on its slow but merry way higher. US equities were also edging a little bit higher while UST yields were essentially going sideways. All that changed post the Minutes, several officials acknowledged an upgrade to their growth and inflation forecast, but the killer line was that only “a couple” of officials were worried about the possibility that the economy would overheat. So the market initially run with the idea that even though there has been a mark up to the growth and inflation outlook, no more fruit juice will be added to the punch bowl anytime soon. In the end, however, common sense appears to have prevailed, our take is that the Minutes reflect events prior to the jump in hourly earnings seen in the January Jobs report and also prior to the extra spending bill passed by Congress early in February. This would suggest that there is a good chance that the current FOMC thinking has evolved towards a more hawkish tone since. Today we have a lot of Fed speakers and next week’s Fed Chair Powell testimony before Congress will be important in this regards.

So looking at the post Minutes market reaction in more detail, US equities are up between 0.20% and 0.67%, although immediately after the Minutes the S&P 500, DJ and the NASDAQ were all up by more than 1%. The UST curve has bear steepened, as we type the 10y rate is at 2.95% and the 2y rate is at 2.27%, a week ago the 2 year rate was 10bps lower at 2.16%.

After a sharp drop immediately post the Minutes, the USD is up across the board. In index terms DXY is up almost a full 1% over the past 24hr and now trades above the 90 mark for the first time since February 12th. In G10, AUD is the worst performer, down 0.94%. The pair currently trades at 0.7811, after briefly trading to an overnight high of 0.7879 just after the Minuets were released.

GBP is the second biggest loser, down 0.54%. The pound initially fell after the UK labour market report showed the UK unemployment rate unexpectedly ticking up and employment grew less than expected. On the positive side, UK wages data surprised on the upside. The GBP then moved higher after hawkish comments from BoE Chief Economist Haldane who said the risks around their most recent projections were to the upside while “the long-awaited – and we have been waiting for a long time – pickup in wages is starting to take root.” BoE Governor Carney, speaking in front of the Treasury Select Committee, wouldn’t be pinned down on when he expected the next BoE rate rise, but the market places around an 80% probability it will be in May. All this gains have essentially reversed post the Minutes and cable now trades at 1.3921, close to the intraday lows.

The euro was under a little bit of pressure prior to the Fed Minutes amid softer EU PMI data. The Flash February German and French PMI data revealed activity in both manufacturing and services rolled over, leaving the impression that although activity levels remain very elevated, the best has past. That said Euro Zone composite PMI eased from 58.8 to 57.5, so the reading remains comfortably in expansionary mode. The euro traded to an overnight high of 1.2359 after the Minutes, but now is down to 1.2288, a level not seen since Valentine’s day.

NZD and CAD have shown a bit more resilience, nevertheless both currencies are down around 0.3% against the USD. The kiwi now trades at 0.7324 and the Lonnie is at 1.2695.

Looking at the commodity space, oil prices have come under pressure post the Minutes on the back of a stronger USD. WTI is now -1.1% and Brent is -0.35%. Meanwhile, Copper, steam coal and iron ore are a little bit stronger at 0.20%, 0.29% and 0.27% respectively.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Trade tensions continue to mount, with critics claiming that China is exporting its industrial overcapacity

Insight

Our monthly transaction data suggest spending ticked up in April after a stagnant performance last month

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.