Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

If Steven Mnuchin reaches a trade pact with China, will it create enough confidence to push the Aussie dollar out of its trading range?

https://soundcloud.com/user-291029717/mnuchin-packs-for-china-us-treasuries-shy-of-3-percent

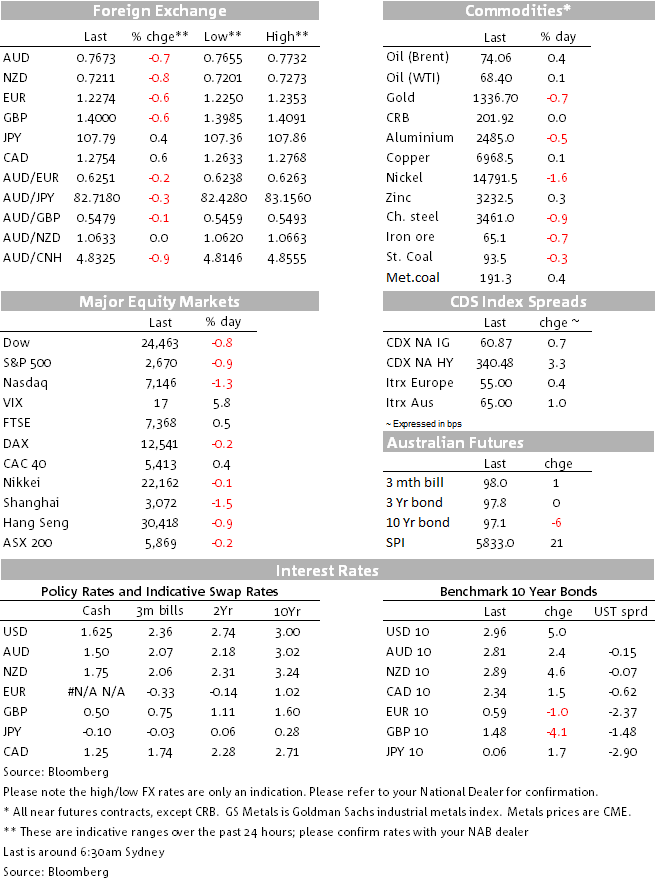

Well not quite knocking on heaven’s door, but one of the big news from Friday’s overnight session was the move higher in 10y UST yields which are now essentially knocking on the 3% mark. The 10y tenor closed at 2.96%, its highest levels since early January 2014 and the 2s10a curve closed above 50bps for the first time in two weeks. US equities closed lower on Friday, posting a second day of negative returns with losses again led by tech shares. The USD found support from the move higher in UST yields with commodity-linked currencies the big underperformers. Commodities had a mixed night.

US equities decline on Friday was led by the IT and consumer staples sectors with the S&P 500 down 0.85% and the NASDAQ -1.27% (DJ was -0.82%). Apple shares have remained under pressure (-4.1%) following Thursday’s “weak demand ”warning from TSMC, one of the iPhone maker’s biggest suppliers. Concern of a slowdown in smartphones sales weighted on the IT sector and the tech heavy NASDAQ index. Despite posting two consecutive days of decline, US equities still managed to record gains for the week. Japanese and European equities outperform and of note after a 1.47% decline on Friday, the Shanghai index was the only main index to record losses for the week, down almost 3%. Technology shares were also the big losers in China.

US yields traded sideways during our APAC session and in the first half of the European one on Friday. Meanwhile, oil prices were on a steady rise on the back of comments from an OPEC and friends gathering expressing a desire to keep tightening the oil market. The comments sparked a response from President Trump noting “Oil prices are artificially very High! No good and will not be accepted!”. The tweet triggered a sell-off in oil prices, but prices recovered with OPEC members and Russia pushing back on Trump’s claim and generally giving the impression that they had no intention of easing up on the supply cuts. Saudi Arabia’s Oil minister said “I have not seen any impact on demand with current prices” and mentioned that OPEC+ would continue its cooperation in 2019, raising the prospect the supply cuts could be kept in place beyond their scheduled end data at the end of this year.

The oil price recovery was accompanied by a selloff in UST yields. 10y UST yields rose over 5bps from 2.915%, closing the day at 2.96%. The move higher in UST yields was led by the back end of the curve, helping the 2s10s curve close the week just above the 50bps mark for the first time in 10 days. UST yields have led the move higher in core global yields this week, the 2y UST tenor ended 10bps higher at 2.459% while the 10y and 30yields closed 13.3 and 12bps higher.

The bear steepening in the UST curve in the last two days of the week has been one of the key factors helping the USD outperform whilst for other currencies soft data releases have also played a role, such as GBP (inflation, retail sales), NZD (inflation) CAD (dovish BoC, inflation and core retail sales on Friday ) and AUD (employment). Commodity linked currencies were the underperformers on Friday (NZD -.089%, AUD -0.75% and CAD -0.70) , probably affected by the risk aversion sentiment in equities and volatility in oil prices. On the week, SEK was the only currency that managed to outperform the USD, partly retracing the soft inflation induced losses from the previous week. The greenback gains on the week has left the USD indices (DXY and BBXDY) close to the top of the ranges held since mid-January and the question now is whether the upper end of these ranges will be tested in the new week.

After flirting with a break above the 0.7825 resistance level on Thursday, the AUD ended the week at 0.7672, close to the lower end of its 0.7643-0.7813 range held since mid-March. Failure to move above the 0.7825 resistance level has left the pair more vulnerable to the downside. Meanwhile the 0.7207 weekly close for the NZD, has also left the kiwi close to the bottom of its 0.7154-0.7438 range held since mid-January.

One of the big macro questions in recent weeks has been whether the global economic slowdown in Q1 was just a weather induced blip, compounded by China’s Lunar new year, or whether the slowdown is actually more deeply rooted with US led trade tensions a contributing factor. The data will ultimately solve this riddle and Monday’s preliminary PMI’s, particularly from Germany and Europe are going to be important in this regard.

Solid PMI prints this week and or higher oil prices could pave the way for 10y UST yields to trade above 3.00%. What drives the 10y tenor above 3% will nonetheless matter. A rebound in the global growth outlook, would be good news for sentiment, but a jump in yields led by oil provoked inflationary pressure could unsettle risk assets. The last two times 10y UST yields got close to the 3% mark in 2013 (2.9937% 5 Sep and 3.02% 31 Dec), the move preceded a selloff in US equities and the pull back in risk appetite weighted on the AUD and NZD.

The EUR fell below 1.23 on Friday, a two week low with media reporting that ECB members were considering waiting until July to change their forward guidance on QE. Speaking in Washington, ECB President Draghi acknowledged that “the growth cycle may have peaked” but said “growth momentum is expected to continue” and reiterated his confidence inflation would eventually move to target. ECB Weidmann also acknowledged the Q1 economic softness, but somewhat contradicting Draghi, he said that “There’s no reason to see a turning point in growth – Germany’s economy is still booming,”. The euro has opened lower this morning and it currently trades at 1.2272.

Speaking on the sidelines of the IMF’s spring meetings, US Treasury Secretary Mnuchin said he was engaged in a “dialogue” with the Chinese government and was “cautiously optimistic” of reaching an agreement to avert trade tariffs. He also said he was considering a trip to China. Meanwhile, the Governor of the PBOC spoke about China’s intention to allow more foreign access to Chinese markets, protect intellectual property and expand imports, all of which should help placate President Trump, if followed through on.

The news could help risk assets at the start of the week, indeed this morning JPY, the preeminent safe haven currency has opened weaker with USD/JPY up about 15 pips to ¥107.80. USD/JPY is flirting with a break above the ¥108 mark and with the USD/JPY-10y UST yields positive correlation reasserting itself, a move above 3% in 10y UST yields may well lift USD/JPY into a higher trading range.

As for commodities, after some Trump tweet fuelled volatility, oil prices still managed to eke out some gains on Friday (WTI 0.13%, Brent 0.38%), copper was unchanged while gold (-0.75%) and iron ore (0.67%) lost a bit of ground. Still, on the week metal prices were the big winners, led by aluminium ( 8%, US Rusol ban), iron was flat and gold a little bit softer.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.